I have always been perplexed why companies in Guyana consistently ignore one of the most important considerations among their shareholders. This column has lamented, year after year and company after company, the absence of comments by companies‘ CEOs and directors in otherwise often very wordy annual reports on the performance of their companies’ shares on the stock market. Banks DIH Limited, the beverage giant has many things to be proud about with respect to its 2011-2012 performance and annual report – historic levels of profits, a strong balance sheet, good industrial relations, a stable management team and growth in share price of 37.5%.

We will get back to this shortly but let us consider first the financial statements.

Banks DIH is a company with two major institutional shareholders – Banks Holdings Limited of Barbados (20%) and Demerara Life Group of Companies (10.8%) – and one that is described as a substantial shareholder under the Securities Industry Act, Trust Company Guyana Limited (6.2%). Banks DIH is also the parent company of Citizens Bank Guyana Inc in which it has a 51% interest. Only two directors of Banks DIH (Messrs Clifford Reis and Errol Cheong) have any shareholding in Citizens Bank. The directors of the company presented their annual report and its audited financial statements last Saturday at a usually well-attended but usually uneventful meeting of its shareholders.

Banks DIH is a company with two major institutional shareholders – Banks Holdings Limited of Barbados (20%) and Demerara Life Group of Companies (10.8%) – and one that is described as a substantial shareholder under the Securities Industry Act, Trust Company Guyana Limited (6.2%). Banks DIH is also the parent company of Citizens Bank Guyana Inc in which it has a 51% interest. Only two directors of Banks DIH (Messrs Clifford Reis and Errol Cheong) have any shareholding in Citizens Bank. The directors of the company presented their annual report and its audited financial statements last Saturday at a usually well-attended but usually uneventful meeting of its shareholders.

Performance

Source: 2012 Annual Report

Source: 2012 Annual Report

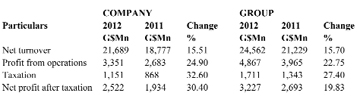

The company recorded an increase in turnover (sales) of 15.5%, the best increase in turnover over the past five years. However revenue for export sales remains minimal, 1.49% in 2012 and 1.24% in 2011. No doubt the directors of the Guyana company would reflect that one of the intents expressed in the Memorandum of Understanding of 2005 under which Banks DIH and Banks Holdings Limited did some cross-investing in each other was to market and distribute each other’s products in their respective home markets. Guyana’s domestic market will remain small for years to come and the company must sooner rather than later focus on the export market. Where the directors have reason to be very satisfied is in terms of the profits earned: a 25% increase over 2011 and a 30.4% increase in profit after taxation.

Strong balance sheet

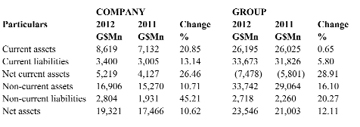

As we look at the balance sheet we see a company that by standard analytical tools is strong. Current assets have increased by 21% while the smaller figure of current liabilities increased by 13%. As a result of the combination of these two variables the net current assets position has increased by 26%.

As the company continues its capital renewal and expansion programme, the directors have opted for an increase in long-term borrowings of $750 million which are expected to increase in the current year due to planned capital expenditure of some $5,124 million on several key operating assets including equipment for the soft drink, beer, water and CO2 plants and ice cream facilities and the renewal of its distribution fleet.

Source: 2012 Annual Report

Source: 2012 Annual Report

Helped by a sale of capital assets that brought in some $461 million and borrowings of $750 million, neither of which is addressed in the CEO’s or the directors’ report, net cash inflow for the year was $101 million, compared with an outflow of $728 million in 2011. The directors would no doubt be keeping an eye on the cash and bank balances even as they recognise that the “company’s continued success will depend on its ability to respond to the needs of a rapidly emerging middle class.”

Shares and their returns

Now let us return to the matter raised in the introduction to this column. Here is why I believe that for the more discerning shareholder, a commentary on share price and performance is important. Five years ago the group had after-tax profits of $898.1 million and paid dividends amounting to $400 million. Analysts use these numbers to arrive at a pay-out ratio with a low ratio indicating a policy of retaining its earnings rather than paying out dividends. In 2012, profits had risen to $2,776 million but the directors recommended and effectively limited dividends to $560 million. The pay-out ratio for the two years is 44.5% and 20.2%. This apparent change in policy is hardly likely to operate in favour of the aging and retired shareholder who depends on dividends, bank interest and modest pensions for their life’s income.

The graph below shows three variables for the group: net profit after minority interest (ie profit available for distribution), dividends paid and dividend plus growth in shareholder value. Dividends remain low, despite significant increase in after-tax profits.

Source: Annual Reports and Guyana Stock Exchange

Source: Annual Reports and Guyana Stock Exchange

2012 provided a windfall for shareholders in terms of the movement in the share price. When examined over the period 2007 to 2012, however, a different picture emerges. Net profit after minority interest over this period was $9,902 million of which $2,810 million was paid as dividends.

The amount of available profits retained by the group was therefore $7,092,213 and which should be reflected in the market value of the company’s shares. This has however only grown by $5,600,000, a shortfall of $1,492 million. If measured against the growth in shareholders’ equity, the shortfall is $286 million.

It is to the credit of the directors of Banks DIH, with one major exception who is no longer with the company, that they have avoided any acquisitive tendency for shares in the company, either for themselves or their associates. Directors Errol Cheong, Christopher J Fernandes, Richard B Fields, George G McDonald and Michael H Pereira all still own the same number of shares they did in 2005. CEO Clifford Reis has 187,500 fewer shares now while Andrew Carto has acquired 71,312 shares since then.

It would be interesting to see whether those companies, the year-end of which is December 31 will comment on their market price performance when they issue their 2012 annual reports and financial statements over the next few months.

Barbados investment

It seems like history since in reaction to a suspected take-over bid by the Trinidadian company Ansa McAl, Banks DIH entered into a mutual investment agreement under which Barbados Holdings Limited (BHL) took a 20% shareholding in the Guyana company in exchange for Banks DIH taking a 6.7% interest in the Barbados company. BHL has two nominees on the Banks board while the Guyana company has one director on the board of BHL from which dividends received in 2012 were $39.4 million while dividends paid to Banks Holdings Ltd, Barbados were $112.1 million.

Despite what may appear to be financial returns that favour the Barbados company, consensus among observers is that the arrangement has helped Banks DIH in more than just putting the takeover threat to rest. The turnover of the company increased by approximately 75% since the investment agreement and the company continues to express satisfaction in its “dedicat[ion] to the Principles of Good Corporate Governance.”

Governance

This column can be accused of a crusade in so far as advocating better demographic representation on boards of public companies in Guyana is concerned. A look at pages 4-9 of the company’s annual report shows the youthful vitality and the gender, age and ethnic diversity which make up Guyana. The personalities in the very attractive advertisements are nine women to seven men; in higher and tertiary education women outnumber men as they do (marginally) in the population as a whole. And no doubt women also make up a large part of the company’s employees and customers, yet as shareholders turn the pages, they enter a different world, where the average age of the population is north of 50, from which women are excluded and none of whom is an Indian, even among a band of eleven. The last time this company had a woman director was in 2006 when the wife of the founder of the company died. In fact the 2005 Annual Report lists twelve directors, including Mrs D’Aguiar, so it seems possible that the company can address this limitation without the need to amend its articles or retire any director.

Conclusion

The Board of Directors Report is well laid out and contains the basic information required by law except with respect to section 168 (g) of the Companies Act which requires the directors to state the directors’ proposals as to the application of the company’s profits, including its revenue reserves. This common omission of companies in Guyana is perhaps because directors consider that it is implied.

While neither the Chairman/CEO nor the directors have much to say about the future, an expenditure of over $10 billion over a three year period is testimony to their confidence in the future of the company.