Introduction

It was emphasized in the previous column that Guyana’s foreign exchange (FX) market is comprised of twenty-one licensed FX traders (buyers and sellers). There are six commercial bank traders and fifteen non-bank traders. It was noted that the quantity of foreign currencies traded in the market increased almost monotonically since 2000. The latter resulted in spite of the continued lukewarm export performance of the official production sectors over this period. Since 2000 the commercial banks have continued their dominance of this market accounting for at least 90 percent of all trades (or purchases).

It should be remembered that the quantity of foreign currencies available for purchase by the traders comes from export revenues, remittances, foreign capital inflows and through the underground economy route. The foreign currencies purchased are then sold to importers, those who wish to travel abroad, and those who want to remit funds abroad. To make a profit, the traders maintain a spread between the buying and selling rates. Last column underscored the tendency for this spread to be persistent and has even increased slightly since 1991.

It should be remembered that the quantity of foreign currencies available for purchase by the traders comes from export revenues, remittances, foreign capital inflows and through the underground economy route. The foreign currencies purchased are then sold to importers, those who wish to travel abroad, and those who want to remit funds abroad. To make a profit, the traders maintain a spread between the buying and selling rates. Last column underscored the tendency for this spread to be persistent and has even increased slightly since 1991.

Price leadership and the

exchange rate

Given that commercial banks account for 90 percent of foreign currency trades, is it possible that one or two commercial banks account for the bulk of the 90 percent trades? In that case the market would tend to be dominated by a price leader. The data are not publicly available to establish the break down of foreign currency trades by trader. But I hope an enterprising economic researcher from UG could tackle this question as it is important for understanding exchange rate determination in economies like Guyana. None of the textbook exchange rate theories emphasize a price leader setting the rate. Textbook exchange rate theories are often derived from the efficient market hypothesis.

The thesis of a price leader is also important because it adds a political economy dimension to exchange rate determination. For example, in a society where the post-Jagan elites can use insider information advantage to ferret funds from a collapsing financial institution to another (yet to collapse), it should be no surprise the elite could use some form of moral suasion to persuade the price leader to maintain a stable exchange rate. Of course, politically, this class has an incentive to maintain a stable exchange rate, which affects the inflation rate and thus the cost of living.

I am not saying it is wrong to maintain a stable exchange rate using moral suasion instead of the market framework of indirect monetary policy. As an aside, in the case of Guyana indirect monetary policy means using Treasury bills to manage excess reserves in the banking system. The basic idea is that if commercial banks have high levels of excess reserves, then they could change portfolio allocations in a manner which could be detrimental to the exchange rate. Therefore, the Bank of Guyana uses a market-based strategy, within the context of an IMF financial programming model, to maintain excess reserves consistent with stable prices and economic growth forecasts.

Moreover, the price leadership (or oligopoly FX market) question should be answered – especially for the purpose of pushing outwards the frontier of academic literature. It is an important question because the IMF continues to shower praise on the government for stable macroeconomic fundamentals. However, as I had argued last year, stable macro fundamentals can only come from transforming the production structure. You can have stable prices and exchange rates but a backward production structure. At the end of the day, it is the transformation of the production base which lifts the welfare of the masses. Guyana is poor because it specializes in the production of commodities at the low end of global hierarchy of products. Hence, the country specializes in being poor. In other words, the IMF’s concept of stabilization is necessary but insufficient for the purpose of economic development.

In the next column, I would give my take on whether the de facto fixed exchange rate is helpful for the purpose of economic development.

The exchange rate

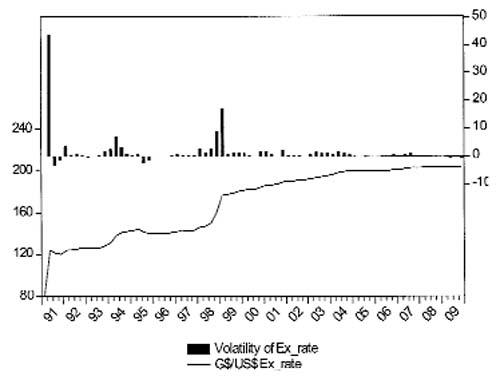

I would only analyze the G$/US$ exchange rate. As was noted in the last column, the US$ is the most traded currency in the Guyana FX market – accounting for approximately 90 percent of all trades. Thus it is this rate which is fundamental to cost of imports, exports and the process of inflation. Hypothetically assume the rate is G$ 204 for one US$. If that number falls it means the Guyana currency has appreciated against the US$. On the other hand, if the number increases it means the G$ has depreciated against the US$.

Figure 1 shows the exchange rate from first quarter 1991 to last quarter 2009. On the left- axis is the G$/US$ rate. It is obvious the rate depreciated substantially in the early period of the formation of the cambio market system; as at end 2009 the exchange rate stood at G$ 204 for one US$. However, by fourth quarter 2004 there commenced a remarkable stabilization of the rate relative to previous periods. It is easier to spot the stability by looking at the bars (right-axis), which shows the change in the exchange rate from one period to the next. Thus a large spike shows a large and volatile change in the exchange rate from period to period. On the other hand, stability is indicated by a less volatile oscillation of the bar spikes. Moreover, when the spike is above zero it signals depreciation, while a spike below zero shows an appreciation of the Guyana dollar.

Figure 1. The G$/US$ exchange rate (left-axis) and volatility (right-axis) – 1991:Q1 to 2009:Q4

Why the stability?

The conventional story emerging from IMF reports is the stability is derived from the prudent macroeconomic policies of the government. The latter largely means lower fiscal deficits and sound monetary policy. I am sympathetic to the sound monetary policy view. However, the fiscal deficit improved substantially from the VAT windfall starting in 2007. As noted above, the stabilization of the rate started in fourth quarter 2004.

The previous column showed that the quantity of foreign currencies (mainly US dollar) available in the economy continue to increase in spite of the weak economic performance of the official economy. FDI inflows have also been tepid but there was resurgence in 2008 as the data from Bank of Guyana indicate. More recently gold export value increased owing to the high world market price. But overall the official economy continues to muddle through. In spite of the latter, the quantity of foreign currencies available for purchase by traders increased almost monotonically. Therefore, are remittances playing an important role in maintaining a stable rate?

My hunch is the most important explanation has to do with moral suasion acting on one or two FX market price leader (s). In technical terms, a price leader would be an oligopoly trader with market power. The market power stems from lock-in effects (perhaps through the largest business loan portfolio), better physical security when making an over-the-counter trade, and superior branch networking reach to mobilize foreign exchange more than all other traders. Thus the smaller traders face a greater foreign exchange constraint (or shortage) even if they would like to offer the public more attractive rates.

A further consolidation of market power occurred in March 2003 when the former National Bank of Industry and Commerce (NBIC) acquired the state-owned Guyana National Cooperative Bank (GNCB). The FX trading arm of GNCB and national branch network were acquired in that process.

One might ask what motivation the price leaders would have to cooperate with the policy makers. If banks could hoard US$ and the rate depreciates then they would realize a profit. However, we must remember that banks which trade foreign currencies are more importantly lenders with large loan portfolios in Guyana dollars. Therefore, it is not in their interest to have the Guyana dollar depreciate rapidly given that importers will pass on the higher import prices to consumers. Thus with rising exchange rate driven inflation, the banks would actually realize a loss in loan value and those who borrowed will gain.

In closing, the stability of the exchange rate, in the short-term, is beneficial for the masses (given the predictability of cost of living) in spite of the political motives of the post-Jagan class. However, we would need to discuss the concept of the real exchange rate in the next column and examine the extent to which this grip of the elites is actually retarding the structural production upgrade of the economy.

Please send comments to tarronkhemraj@gmail.com