Recently a number of readers have asked me to offer an opinion on the prospects for the Guyana economy over the short-to-medium term. Most of the persons raising this query, I suspect, have a political interest in my response. I shall attempt a response by drawing attention to what economists describe as the downside risks facing the economy and comparing these to the upside expectations, which are there.

Performance

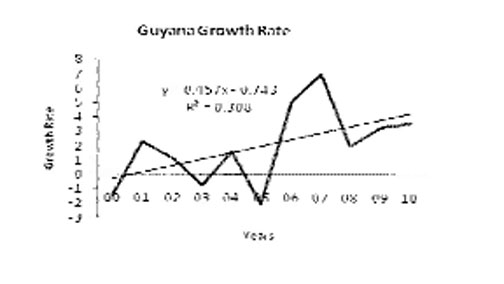

It would be useful to begin with a brief look at the recent performance of the economy. The graph below illustrates the behaviour of the growth rate of real GDP since 2000.

Given

Given  the persistent pockets of poverty, lack of productive jobs, and the pressures and strains on the livelihoods of the vast majority of Guyanese, economic growth has been most disappointing. Three of the years (2000, 2003, and 2005) have witnessed negative growth rates. In only two years (2006 and 2007) have growth rates reached 5 per cent and over. In none of the other nine years has the growth rate reached four per cent. Further, a matter of concern to me is that given the way the GDP is computed, it usually shows positive upswings after catastrophic events as economic recovery takes place. The year 2005 was the year of the country’s great flood so that the 2006-2007 performance has to be seen with a grain salt. There is also the additional consideration that after the recent GDP rebasing exercise from 1988 prices to 2006 prices, the GDP data have shown improved GDP performances. The table below presents the data shown in the graph with additional information on the growth rates for 2007-2009 (for which we have data) based on both 1988 and 2006 prices.

the persistent pockets of poverty, lack of productive jobs, and the pressures and strains on the livelihoods of the vast majority of Guyanese, economic growth has been most disappointing. Three of the years (2000, 2003, and 2005) have witnessed negative growth rates. In only two years (2006 and 2007) have growth rates reached 5 per cent and over. In none of the other nine years has the growth rate reached four per cent. Further, a matter of concern to me is that given the way the GDP is computed, it usually shows positive upswings after catastrophic events as economic recovery takes place. The year 2005 was the year of the country’s great flood so that the 2006-2007 performance has to be seen with a grain salt. There is also the additional consideration that after the recent GDP rebasing exercise from 1988 prices to 2006 prices, the GDP data have shown improved GDP performances. The table below presents the data shown in the graph with additional information on the growth rates for 2007-2009 (for which we have data) based on both 1988 and 2006 prices.

Guyana’s Growth Rate

Year Growth Rate (Real GDP by industrial origin)

2000* -1.4

2001* 2.3

2002* 1.2

2003* -0.7

2004* 1.6

2005* -2.0

2006* 5.1

2007** 7.0 (5.4 @ 1988 P’s)

2008** 2.0 (3.0 @ 1988 P’s)

2009** 3.3 (2.3 @ 1988 P’s)

2010** 3.6

Note: 1) * = 1988 prices

2) ** = 2006 prices

Source: Government of Guyana official statistics

It is useful to observe that the government has targeted growth rates in excess of four per cent for the past three years in its Budget presentation (2008-2010). The target growth rates, actual growth rates, and the variances between these are shown below:

Guyana Growth Rate (Targets vs Outcomes)

2008 2009 2010

Budget target: 2.8 4.7 4.4

Actual growth rate: 2.0 3.3 3.6

Variance (%) 58 34 18

The variances for the three years have been high. Their mean value is 37 per cent. This indicates that targeting has erred on the size of over-estimation by more than one-third of the actual outcome. However, it should be observed that there might be a downward trend in this overestimation, in that its size has fallen from 58 per cent in 2008 to 18 per cent in 2010!

Downside risks

When economists speak of downside risks they refer to the probability that events that are unfolding and which may be beyond the control of the authorities may have such adverse effects on the economy as to falsify their predictions downward. When they speak of upside expectations they are referring to the probability that positive effects on the economy, which may also be beyond the control of the authorities, could lead to the upward revision of these predictions.

It should be noted that these categorisations are not hard and fast. A downside risk could turn out to be, unexpectedly, an upside expectation and vice versa.

In the next couple of weeks, I shall present about ten downside risks and at least four major upside expectations, which I see on the short-to-medium term horizon for the Guyana economy. The upside expectations are potentially huge. I truly believe therefore that the country needs an intelligent, creative and inclusive political administration after the next election to pursue the effective management of Guyana’s development process.

Global economic recovery

The first of the downside risks stems from the fact that, in this highly globalised world economy, no country can predict its economic future without first assessing the prospects for recovery from the global economic and financial crisis and economic recession.

There are four threats that cannot be ignored, which could slow or even reverse the economic recovery we are now witnessing. These are 1) the threat of global destabilization posed by the Middle East uprisings; 2) rising oil prices, which threaten to reach pre-crisis levels or higher. The rise in oil prices is driven by the economic recovery itself as well as the instabilities mentioned at 1); 3) the nuclear crisis in Japan, which has precipitated concerns about nuclear energy that will affect both oil prices and global efforts to combat climate change and global warming; and, 4) the persistent sovereign debt crises in several European Union countries: Portugal, Ireland, Italy, Greece and Spain (the so called PIIGS economies).

We may safely conclude therefore that the global recovery is still at risk of being reversed over the short-to-medium term. If so, then the economic performance of Guyana, as indeed that of all other economies in the world, could be adversely affected.

Ed note: We regret that there is no Business Page today.