In mid-2011 there was concern about a shortage of construction lumber on the domestic market. At the beginning of a new quinquennium of government, and having the election manifesto commitments of the three largest parties, it is appropriate to extract those commitments and compare them with the latest export figures.

The PPP/C reduced its half-page on forestry in 2006 to a single paragraph in 2011– “Encourage more value-added forestry by working closely with all stakeholders on addressing constraints while continuing to support the development of our timber and non-timber resources in a sustainable way consistent with the LCDS.”

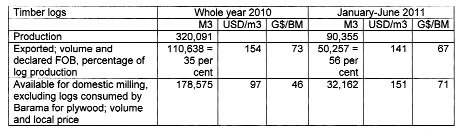

All national policies favour in-country processing and value-addition for forest products, yet the government continues to allow in effect unlimited exports, with logs at remarkably low declared FOB values. From the latest data published by the Guyana Forestry Commission (GFC) – The average log measures between 2 to 3 cubic metres. The figures above show that the declared average price of exported logs was US$54 in 2010 and US$141 in the first half of 2011. Since 2008 the GFC has suppressed almost all information on the species of logs exported.

All national policies favour in-country processing and value-addition for forest products, yet the government continues to allow in effect unlimited exports, with logs at remarkably low declared FOB values. From the latest data published by the Guyana Forestry Commission (GFC) – The average log measures between 2 to 3 cubic metres. The figures above show that the declared average price of exported logs was US$54 in 2010 and US$141 in the first half of 2011. Since 2008 the GFC has suppressed almost all information on the species of logs exported.

The trend until then, and no doubt into the present, has been for the export of the premium hard and heavy timbers of Guyana for conversion into top quality flooring and furniture in China and India. US$154 per cubic metre is a rock bottom price for these timbers. A more usual FOB price for technically equivalent timbers is three times as much, as demonstrated by the price paid for merbau logs in South East Asia, which are equivalent to purpleheart.

The rise in export commission on logs (from 2 to 7 per cent in January 2009, to 10 per cent in 2010 and 12 per cent in 2011) has evidently been far too small and ineffective in preventing rises in both absolute volumes and percentages of exports relative to national log production.

Average domestic log price has risen by more than 50 per cent in the first half of 2011 yet declared average export FOB price for logs has declined. And a further 30,000 m3 of logs were exported during July-September 2011 (Forest Products Marketing and Development Council for GFC).

Moreover, domestic log buyers have to pay VAT on the logs they process. To put it another way, domestic millers and consumers are penalized while Asian log exporters are rewarded by the GRA. This is what can be called a perverse policy measure.

Using the log-to-furniture conversion value ratios published in a letter (Mahadeo Kowlessar) by Kaieteur News on July 4, 2007, Guyana could have earned up to US$162 million from furniture in 2010 and up to US$73 million in the first half of 2011, instead of the miserable US$17 and 7 million actually recorded as the log export income. That is, Guyana could have earned up to ten times the amount from furniture than from the unprocessed logs.

According to surveys from the GFC, there is no shortage of installed capacity to process more than double the recorded total log production.

As the commercial banks are overflowing with liquidity, presumably there is no shortage of cash to invest in upgrading processing machinery?

Presumably also the government investment agency GO-Invest is keen to provide support, although its website has not been updated since 2005, so it is difficult to be sure; see http://www.goinvest.gov. gy/forestry.html.

And how do the opposition political parties propose to address this problem?

The AFC focused on policy issues and did not directly address timber processing. However, it promised to “Ensure that associations of small-scale loggers are provided with special access“ in the strategic plan for allocation of State Forest Resources.

APNU offered both diagnosis and commitment: “Contrary to all recommendations, there has been a marked increase in the export of logs, rough sawn and poorly dressed green lumber principally to China, India and the Caribbean. Added to this, value-added and downstream processing has declined significantly.

This has reduced the potential impact of the sector on employment. The MOU with Norway allows the controlled cutting of timber and downstream processing. An assessment of the reasons for the sector’s under-performance include the following:

● Under-capitalisation of entities needed for value-added production

● Inadequate marketing, facilities, training and technology

● Export of logs

● Inefficient and ineffective harvesting

“APNU in government will prioritize and facilitate through incentive a comprehensive and strategic plan to substantially increase value-adding of our forest production.“

Subsequently I propose to look at the production and export of sawn timber, and what stakeholders proposed at meetings in August and September.

Perhaps the GFC could even publish the reports of those meetings on its website, in accordance with the improved transparency in forest governance promised to the Government of Norway?

Yours faithfully,

Janette Bulkan