The Budget 2012 reveals that despite the statistical benefit which is derived from using the rebased 2006 GDP series as the denominator (because this has led to an approximately two-thirds increase in its size) the debt stock to GDP ratio for Guyana has increased from its low of 60 per cent in both 2007 and 2008 to 70 per cent in 2011. It took decades of real economic stress and distress to bring the debt to GDP ratio down from its peak levels of 2-3 times the value of GDP about 2-3 decades ago, to the low of 60 per cent in 2007 and 2008. I had cautioned readers last week about this recent increase, as the last thing Guyana can afford at this juncture is to return to the distress of the notorious ‘valley of debt.’ With a debt to GDP ratio of 70 per cent in 2011, both investors and financial markets are likely to react adversely, as they will see Guyana approaching the shadow of the valley of debt. This behaviour on their part would be typical for them, as it has occurred on myriad of other occasions around the world.

The data which I presented last week also showed most of the rise in the debt stock coming from domestic debt increases; total domestic debt has doubled in value since 2007. However, it had only increased by 50 per cent in the earlier years 2000 and 2007. The data further revealed that, during the 2000s, the external debt had declined from about US$1.2 billion in 2000 to a low of US$0.7 billion by 2007. Unfortunately, last year it was back at US$1.2 billion! For readers convenience Table 1 below briefly summarizes the debt/GDP ratios for 2007-20011.

As can be observed in the table during 2007-2011 the external debt/GDP ratio had a narrow range (from 40 to 44 per cent) and an average of 42 per cent. However, the range for the domestic debt/GDP ratio was larger (from 19 to 28 per cent) for an average of 22 per cent.

As can be observed in the table during 2007-2011 the external debt/GDP ratio had a narrow range (from 40 to 44 per cent) and an average of 42 per cent. However, the range for the domestic debt/GDP ratio was larger (from 19 to 28 per cent) for an average of 22 per cent.

Money supply expansion

Growth in the money supply is a useful indicator of how supportive in practice the monetary authorities are to a rise in sovereign indebtedness. The question which should therefore be asked is: what do the Guyana monetary data reveal? As Table 2 below indicates, first, over the 2000s the total money supply has more than trebled. Second, when this total is disaggregated into its two main components, narrow money supply and quasi money supply, we observe the following: narrow money supply (or what economists term as M1) is constituted of currency supply and demand deposits held by commercial banks. This has expanded by nearly four-fold over the 2000s. Quasi money supply (or what economists term as M2) is constituted of time

Growth in the money supply is a useful indicator of how supportive in practice the monetary authorities are to a rise in sovereign indebtedness. The question which should therefore be asked is: what do the Guyana monetary data reveal? As Table 2 below indicates, first, over the 2000s the total money supply has more than trebled. Second, when this total is disaggregated into its two main components, narrow money supply and quasi money supply, we observe the following: narrow money supply (or what economists term as M1) is constituted of currency supply and demand deposits held by commercial banks. This has expanded by nearly four-fold over the 2000s. Quasi money supply (or what economists term as M2) is constituted of time  and savings deposits held in the commercial banks. This category nearly trebled in value during the 2000s. Graph 1 below illustrates these behaviours.

and savings deposits held in the commercial banks. This category nearly trebled in value during the 2000s. Graph 1 below illustrates these behaviours.

On closer examination readers would note these data reveal that, like the trend in sovereign indebtedness observed before, the increases in money supply were larger for the most recent years (that is, after 2006/2007) than in earlier years of the 2000s. (Data on annual changes in total money supply are shown in the extreme right columns of Table 2).

Price inflation

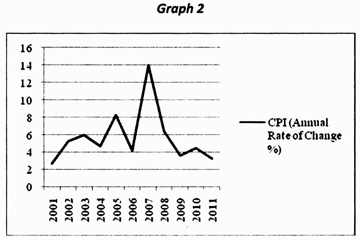

Most readers would associate significant rates of increase in money supply (and indeed liquidity more generally) with price inflation. It would be useful therefore if we looked at the annual rate of change of the consumer price index (CPI) over the last decade. These are shown in Table 3 at left and illustrated in Graph 2.

Most readers would associate significant rates of increase in money supply (and indeed liquidity more generally) with price inflation. It would be useful therefore if we looked at the annual rate of change of the consumer price index (CPI) over the last decade. These are shown in Table 3 at left and illustrated in Graph 2.

Readers should note that over the last decade the CPI information was constructed from two different base periods, namely January 1994 (the older  series) and December 2009 (the new series).

series) and December 2009 (the new series).

Next week I shall continue this discussion of the threat of debt stress and distress embedded in the National Budget 2012 from this observation on the behaviour of price inflation.