Dear Editor,

One of the attributes of someone engaged in teaching, as I have been at various times, is the constant and necessary effort to put things over in a manner that facilitates comprehension by students. While that does not apply to Mr Ralph Ramkarran, his response of March 1 to my letter of February 29 on the two financial papers currently before the National Assembly, suggests that he missed several points which I thought would be quite obvious, particularly since he presided over the parliamentary debate on the Fiscal Management and Accountability Act 2003 which is again being hotly contested in the National Assembly. Mr Ramkarran either does not understand, or is unwilling to accept, that the Financial Administration and Audit Act Cap.73:01 is as different from the 2003 Act as chalk is from milk.

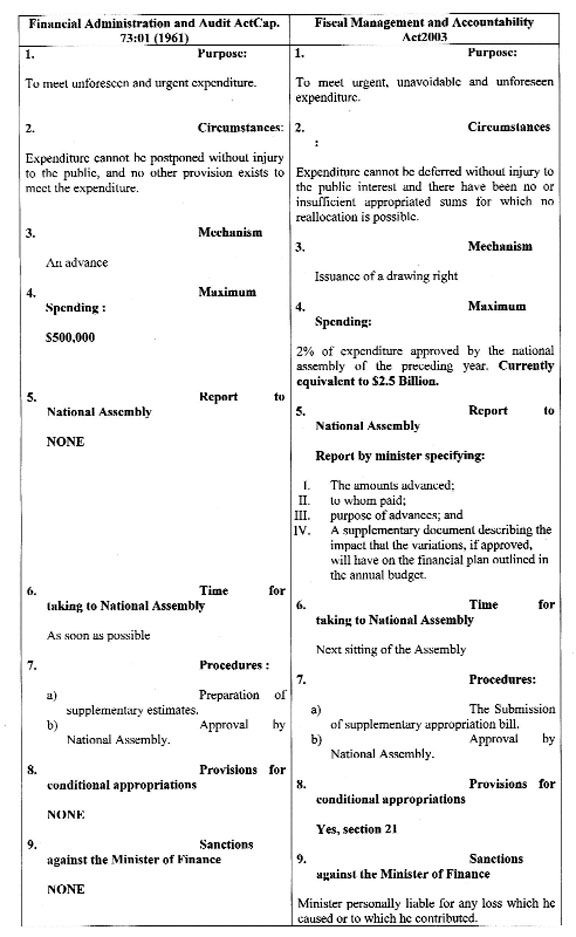

In order to make the differences between the relevant Contingencies Fund provisions of the two Acts excruciatingly clear – borrowing the words of our energetic new Attorney General – I thought it would be helpful to set those features out in tabular form. Visually, the following ought to be obvious: that the provisions are vastly different; the reasons for their being different (the sums involved, ever evolving standards of accountability and transparency); what the legislators set out to do to manage the risks associated with the huge sums involved (detailed reporting, a statement showing the impact on the annual budget); and statutory sanctions against the Minister.

In order to make the differences between the relevant Contingencies Fund provisions of the two Acts excruciatingly clear – borrowing the words of our energetic new Attorney General – I thought it would be helpful to set those features out in tabular form. Visually, the following ought to be obvious: that the provisions are vastly different; the reasons for their being different (the sums involved, ever evolving standards of accountability and transparency); what the legislators set out to do to manage the risks associated with the huge sums involved (detailed reporting, a statement showing the impact on the annual budget); and statutory sanctions against the Minister.

It may have escaped the attention, not only of the learned Senior Counsel Mr Ramkarran but also the entire National Assembly, that the limit remained at a modest dollar sum for thirty-seven years because the circumstances – even at the lower pre-2003 standards – so extreme that it would have been unimaginable that any person would be given discretion to spend such huge sums without parliamentary approval when the convening of the National Assembly is a telephone call away! Section 41 should be amended immediately to restore some discipline to the demonstrated tendency of Dr Ashni Singh to abuse his powers and to act recklessly. I recommend a figure of no more than $50 million, which is one hundred times the pre-2003 limit.

Finally, as demonstrated by letters in the press, Mr Ramkarran is not the only person who appears to have difficulties with the nature and implications of the 2003 vis-à-vis the 1961 Act. He shares company with Mr Philip Bynoe and pollster Vishnu Bisram, who can only see an “Indian hospital.” Not too long ago, Mr Bisram saw a landslide; it was a mirage.

To my disappointment, Mr Ramkarran, stung by my letter, allowed himself in his March 1 letter to degenerate into the public ‘cuss-down’ which up to recently he had opposed from his nemesis Mr Jagdeo. I would suggest that he moderate any intemperate response to this letter, since he himself is not without vulnerabilities.

Yours faithfully,

Christopher Ram