(Part 1)

By Rawle Lucas

Leadership change

The company that has the ship as its logo is about to sail into a new era. Demerara Distillers Limited (DDL) announced a major leadership change a couple weeks ago. The long-time President and Chairman of the company will step down to be replaced by a relatively younger, but reportedly equally seasoned leader. DDL, born out of the centuries-old activity of sugar in Guyana, is looking to the future with a global character and perspective.

It is making the switch in leadership at a time of political logjam at home and intense global competition and heightened due diligence abroad stemming from the concerns about money laundering and the financing of terrorist activities. One understands that the change in leadership at DDL is driven more by age progression rather than by any disappointing economic news or circumstances of the company. Yet, change of such momentous proportions cannot pass without examining the situation to be inherited by the new leader. In a way, such a review, albeit limited, would help to put in some context the expectations and responsibilities of the new leader and acknowledge the acclaimed track record of the departing one.

A precious beverage

Whether on its website or its annual reports, the story of DDL as told by the company is always fascinating. The history of the company boggles the mind. It starts with the thought that Guyana at one time had as many as 300 sugar estates with almost all of them producing rum. The size of each does not matter. It is the mere scope of the operation that thrived for a long time on slave and indentured labour. The technology of today makes one wonder what manufacturing the alcoholic beverage on each plantation was like at that time. But it is the thought that over 200 rum-making entities could be reduced to one that is the marvel of the economic adjustment of Guyana in the DDL story.

It takes some economic downsizing to reach a singular production unit that then begins to rebuild itself into a different personality; one that competes in the domestic and global market with a brand, El Dorado, that shines like the elusive city of gold that once captured the spirit of adventure and avarice of the many who sought to partake in the riches of Guyana.

It takes some economic downsizing to reach a singular production unit that then begins to rebuild itself into a different personality; one that competes in the domestic and global market with a brand, El Dorado, that shines like the elusive city of gold that once captured the spirit of adventure and avarice of the many who sought to partake in the riches of Guyana.

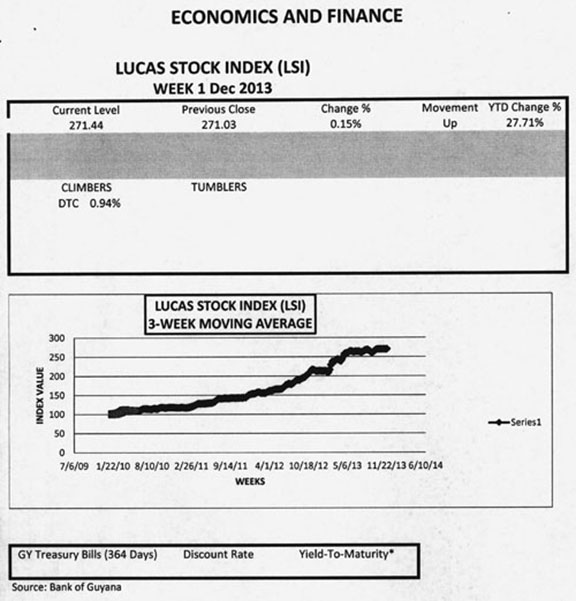

The Lucas Stock Index (LSI) rose 0.15 percent in trading during the first week of December 2013. The stocks of six companies were traded with a total of 1,104, 364 shares changing hands. There was one Climber and no Tumblers. The Climber was Demerara Tobacco Company (DTC) which rose 0.15 percent on the sale of 2,270 shares. The stocks of Banks DIH (DIH) which sold 106,776 shares, Demerara Bank Limited (DBL) which sold 956,590 shares, Demerara Distillers Limited (DDL) which sold 34,223 shares, Guyana Bank for Trade and Industry (BTI) which sold 1,000 shares and Sterling Products Limited (SPL) which sold 3,505 shares remained unchanged.

As the years passed, El Dorado became a reality that was to be enjoyed, not as a precious metal, but as a precious beverage that titillated the palette of the rum drinkers and stimulated conversation into the wee hours of the morning. It acquired the status through the dedication of its workers, its management and the astute and acclaimed leadership of its retiring President.

Diversified entity

While we must wait for the numbers of 2013, there is plenty in the history of the company which allows one to ponder the influence and impact of the outgoing President. DDL moved from being a single-product company to a diversified entity offering many products and services to Guyanese and foreigners. In addition to its many varieties of El Dorado rum, DDL produces and sells softer beverages and food products in the domestic market. The products that it produces include carbonated beverages like Pepsi, Seven-Up, Slice and Mountain Dew.

Along with the sodas, DDL produces fruit juices, jams and jellies, carbon dioxide and dry ice. The range of activities of the company includes distributing Nestle and Johnson and Johnson products, both of which are household brands at home and abroad. DDL also provides shipping and warehousing services. Within the last 10 years, the company also had a fish and shrimp processing operation and was involved in the information technology business, providing software support and operating as an internet service provider. It has since given up these latter two businesses.

Special attention

As a result of its many activities, DDL operates in more than one sector of the Guyana economy. While the majority of its activities could be described as manufacturing, DDL by virtue of its commercial trade, supply chain and insurance activities could be identified with the services sector of the Guyana economy as well. Its output is noticeable since it contributes at least one per cent of the value-added output of the nation from among the many participants in the economy.

It therefore gets special attention from policy-makers and competitors. Not only are the activities of DDL spread over multiple sectors, they are also spread over several continents. The operations of DDL could be found in Asia, Europe, Latin America and the Caribbean, and North America. The bulk of its business operations, 91 per cent, is done in Guyana. Smaller amounts of manufacturing take place in Canada, Europe, India, Jamaica, St Kitts and Nevis and Trinidad and Tobago. In addition to Guyana, the service operations of DDL could be found in Canada, Europe, India, Trinidad and Tobago and the United States of America, indicating that the operations in Jamaica and St Kitts and Nevis do not contribute to this part of the company’s revenue stream. The array of business activities and locations of operation make DDL a conglomerate.

Tighter

The new leader will be taking over the company from the beginning of the new year and would be inheriting a somewhat healthy enterprise. There is many a slip between cup and lip and the 2013  numbers are unavailable to the public. Being an insider, the situation of the company would be no surprise to him, even if the numbers differ significantly from those of 2012 for those of us on the outside. Based on the 2012 data, however, the new leader would be taking over a company with a current ratio that shows it has more than enough current assets to cover its obligations.

numbers are unavailable to the public. Being an insider, the situation of the company would be no surprise to him, even if the numbers differ significantly from those of 2012 for those of us on the outside. Based on the 2012 data, however, the new leader would be taking over a company with a current ratio that shows it has more than enough current assets to cover its obligations.

Things become tighter when the current obligations are set off against the resources that are readily convertible into cash. That ratio drops considerably and indicates that the company has only about 10 cents in liquidity to cover every dollar of current liability. Business transactions are usually done in an orderly fashion and the company would be able to buy time. Such a financial posture heightens the risk of the company in an emergency and reveals that it lacks much financial flexibility at this point in time. In a more defensive posture, DDL actually has 203 days in which to raise cash to meet critical production, administrative and selling costs.

A good position

As regards the long-term strategy of the company, some evidence exists as well. The new leader would be picking up at a point where the company invests 55 per cent of its current assets in its long-term future. He would also find a company that invests an average of 25 per cent of its working capital in the long-term financing of the business.

The long-term investment strategy of keeping 66 per cent of the productive assets of the company in the long-term financing of the business is also a scenario that the new head of DDL will inherit. The new president of DDL would be inheriting a long-term financing strategy that is typical of major manufacturing companies in Guyana. He would be inheriting a situation in which 86 per cent of the long-term financing of the company would come from internal resources. This is a very good position in which to be because it leaves management firmly in control of the operations of the enterprise. But it increases the need for good customer care in order for that long-term financing strategy to continue. These are known variables to him since he is a long-serving member of the leadership of the company. Being an insider, the transition should be easy, yet these numbers have implications for the company and the new leader and deserve further inquiry, at least for the sake of the shareholders of the company. These and other issues would be looked at in the second part of this article.

Challenges

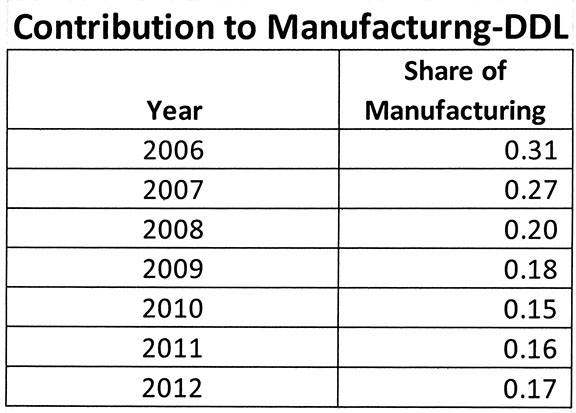

Despite familiarity with, and knowledge of, the company, the new leader will encounter challenges that are not so obvious. One interesting development is the position of DDL in the manufacturing sector. The table below provides a sense of the challenge awaiting the new head honcho of the company. As could be noted from the table, DDL contributed 31 per cent of the output of the manufacturing sector in 2006. However, by the end of 2012, it was contributing nearly half of that amount.

It raises the issue as to how much of this downward movement could be ascribed to the business strategy of the company and how much is the result of exogenous forces. There is no doubt that the rebasing of the Guyana economy has had an impact on the numbers. The downward trend also suggests that more manufacturers might be joining the sector. However, that should also be reflected in higher employment numbers and that remains an open question. Part of the impact could be coming from rice which has done well for itself in the period under review. Further analysis is required, but the movement in the numbers regarding DDL’s share of the manufacturing sector is something that the new head of the company would have to think about. Remaining a visible and significant part of the manufacturing sector will give him a chance to stamp his own impression on the company.

(To be continued)