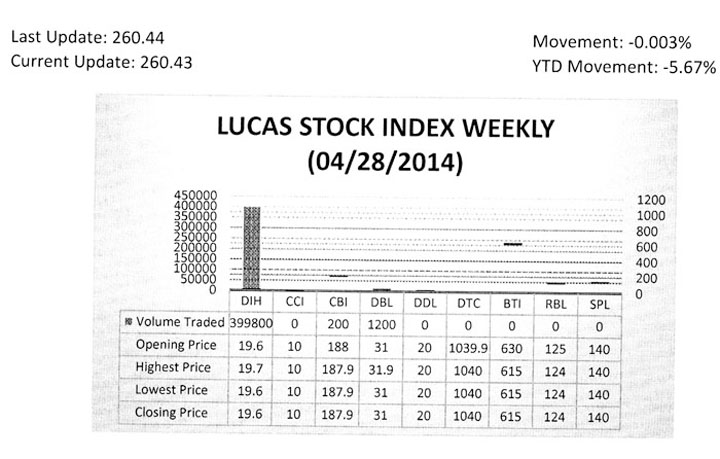

Largest Companies

Republic Bank (Guyana) is by far one of the largest companies in Guyana by any measure. It holds assets in excess of $117 billion. It has annual sales in excess of $6 billion and it has a market value of about $36 billion, 45 percent more than its closest rival. In the world of Guyanese business, Republic Bank is a behemoth. Republic Bank (Guyana) is a subsidiary of Republic Bank which is based in Trinidad and Tobago. Republic Bank went through several incarnations. At one point, it was known as Royal Bank of Canada. The name was changed to the National Bank of Industry and Commerce after it was acquired by the Government of Guyana. Upon conversion to a privately owned bank, the name remained NBIC until it was purchased by Republic Bank. Interest in the performance of this entity and in the other financial institutions that are listed on the Guyana Stock Exchange stems from the seemingly unending growth which they have experienced in the Guyana economy. It ought to be of interest to Guyanese to understand how each individual bank has been able to sustain a run of increasing yields for so long.

Combination of Factors

In this instance, the focus is on Republic Bank (Guyana) with an effort to understand how, with the lowest return on assets, it was still able to generate a 24.5 percent return on the investment of its owners as reported by the Bank of Guyana. The assumption made here is that it used its financial leverage, that is, the ability to use the money of others to operate the business. For a bank, the opportunity comes from the deposits made by customers. Republic Bank holds 35 percent of the total deposits as at September 2013. This means that all the other banks had to share 65 percent of the pie, which works out to be an average of 13 percent each. Having all that money means nothing unless it is used effectively. It would appear that there is a combination of factors contributing to the handsome return on equity earned by RBL. Yet, the poor performance of its assets hangs like a cloud over the bank’s head.

it was still able to generate a 24.5 percent return on the investment of its owners as reported by the Bank of Guyana. The assumption made here is that it used its financial leverage, that is, the ability to use the money of others to operate the business. For a bank, the opportunity comes from the deposits made by customers. Republic Bank holds 35 percent of the total deposits as at September 2013. This means that all the other banks had to share 65 percent of the pie, which works out to be an average of 13 percent each. Having all that money means nothing unless it is used effectively. It would appear that there is a combination of factors contributing to the handsome return on equity earned by RBL. Yet, the poor performance of its assets hangs like a cloud over the bank’s head.

Getting to ROE

Getting to the return on equity (ROE) all starts with generating increased income. One of the best ways to do so is through customer demand, which is often reflected in the money earned. Everyone knows that a company depends on its assets to generate its income. These assets are put in the service of customers who, if satisfied, readily pay for the services. On the face of it, customers seem to be responding to the overtures of the bank. Indeed, RBL makes a big issue out of customer service. Its Managing Director places much emphasis on this vital aspect of the bank’s operation as could be seen from his remarks taken from the 2013 Annual Report of the company. “Ensuring that our customers experience continuous improvement in service delivery continues to be the cornerstone of our Bank, with emphasis being placed on training and development of staff, enhancing our products and services, and expanding our delivery channels to meet our customers’ needs”. The attention being given to its customers appears to be paying off because the bank was able to expand its revenue by 10.73 percent over 2012. Even more pronounced was the increase in gross profit margin which grew by 28.46 percent.

Getting to the return on equity (ROE) all starts with generating increased income. One of the best ways to do so is through customer demand, which is often reflected in the money earned. Everyone knows that a company depends on its assets to generate its income. These assets are put in the service of customers who, if satisfied, readily pay for the services. On the face of it, customers seem to be responding to the overtures of the bank. Indeed, RBL makes a big issue out of customer service. Its Managing Director places much emphasis on this vital aspect of the bank’s operation as could be seen from his remarks taken from the 2013 Annual Report of the company. “Ensuring that our customers experience continuous improvement in service delivery continues to be the cornerstone of our Bank, with emphasis being placed on training and development of staff, enhancing our products and services, and expanding our delivery channels to meet our customers’ needs”. The attention being given to its customers appears to be paying off because the bank was able to expand its revenue by 10.73 percent over 2012. Even more pronounced was the increase in gross profit margin which grew by 28.46 percent.

The substantial change in profits increases the prospects that the assets under the control of the management are performing well and are meeting the expectations of customers. For a financial institution like RBL, the aim is to increase the efficiency of its productive assets. Typically, those include the loans and advances that are made to customers as well as the physical assets of the bank such as its ATM machines and computers that are supposed to help get customers in and out of the bank quickly. For RBL, the physical assets are an integral part of the service delivered to customers and it sees them as critical to the success of the bank as it does its loans and advances. RBL pays much attention to its technological infrastructure which it uses to enhance the electronic banking services to its customers.

To emphasize this point, the Managing Director states further in the Management Discussion and Analysis which is found in the 2013 Annual Report “[our] focus in this area remains that of providing innovative and advanced service alternatives that are convenient, timely and cost effective”. There is little doubt about this emphasis since the bank increased its long-term investment in its productive assets by 15 percent. The observed long lines in and out of the bank might suggest that attaining the goal of faster service might is still a work in progress.

Slipped

But yet as the bank itself observes, the return on its assets has slipped further. Clearly this event raises a question not so much about the commitment of RBL to its declared statements about delivering the best service to customers, but to how effectively the bank is actually accomplishing this task. The bulk of the bank’s productive assets is in the form of loans and advances.

This category makes up about 82 percent of the productive assets of the bank. Consequently, any attempt to understand how efficiently the bank is utilizing its assets to meet its customers’ needs would benefit from a focus on loans and advances. To do so, one would have to consider the gross performance of the loans. In that way, none of the other factors interfere with the performance of the most important element of the asset portfolio.

A review of the notes to the accounts helps us to link the amount of loans and advances with the interest revenue that it produces. The loans and advances portfolio of RBL grew by nearly 21 percent from 2012. Not only did the asset base expand, the cost of borrowing by the bank actually declined by 13.5 percent. The note to the accounts reveals also that loans and advances are responsible for 93 percent of the interest earned by the bank. Compared to last year, revenues associated with the loans and advances grew by 20.16 percent. The real focus here though is on how efficiently the critical assets of loans and advances are working for the bank. This outcome is depicted by the relationship between interest revenue and loans and advances. This relationship is similar to the asset turnover, but with a limited focus. Based on the data reported in the annual report, the turnover was recorded at 12.16 percent for 2013 and 12.07 for 2012. Despite the smallness of the change, it enabled RBL to increase the efficiency of its loan portfolio by $466 million, thereby enabling it to add that much money to its bottom line in 2013.

Behaviour of Current Assets

With loans and advances acquitting themselves, the challenge for the bank must lie in the way the other productive assets are being used or in the behaviour of the current assets. Two events appear significant here. The decline in the cash and equivalents and the increase in the statutory reserves are important. The bank can do little about the movement in statutory reserves. However, it might want to reexamine the behaviour of its cash and equivalents and the impact that that is having on its total asset turnover.

Further, given that the long-term investment of the firm is linked to its long-term financing disposition, an examination of this condition would be useful. Based on current circumstances, the long-term financing of RBL is primarily based on its long-term internal equity position. Current data reveal that 98 percent of RBL’s long-term investment is generated from the internal equity of the firm. Long-term debt and equity therefore do not play a significant part in the bank’s long-term investment strategy. This means that management has it within its power to confront the challenge that it is facing with respect to the performance of its assets. The growth in the return in equity which was reported by the bank could not come from external debt or equity. Therefore, financial leverage has no impact on the long-term strategy of RBL.

The Challenge

The challenge therefore must be in how the bank is handling its deposits. As was noted last week, RBL has a diversified portfolio and is the leader in household lending. The distribution of its loans between businesses and households plays an important part in the revenues generated. RBL may need to reexamine its profit maximization strategy and rebalance the distribution of its portfolio. It may also need to take a look within the two portfolios to see which of the business activities is constraining the performance of its assets.