Leadership

The Guyana Bank for Trade and Industry (GBTI) is the second largest bank in Guyana with about 25 percent of the deposits, a market capitalization of $25 billion and assets to the tune of $95 billion or 28 percent of the assets under the control of the commercial banks. Based on the nominal changes, GBTI has been growing from strength to strength. Over the past three years, assets have grown at the rate of 16.3 percent per annum. Deposits have grown at the rate of 18.3 percent per annum and loans and advances, the largest income-generating assets, have advanced at the rate of nearly 32 percent per annum. This positive growth reflects favourably on the leadership and staff of the entity and a commitment to remain a leader in the banking sector. But even amidst the favourable figures, it is possible to spot some trends that draw attention to the business strategy of the bank and prompt one to ask if its assets are working as efficiently as they could. For example, current assets as a share of long-term investment have been declining within the past three years. One cannot help noticing too the variable nature of the investment in long-term assets. The behavior of these variables has implications for the profitability of the company.

Profile

![]() The operational profile of GBTI is an interesting one. Like the other commercial banks, GBTI accepts deposits from customers and in turn uses the money to generate income. Customers continue to place confidence in the bank, even though deposits grew at its slowest pace, 12 percent, in the last four years. A review of its exposure profile reveals that the dominant focus of GBTI is the service sector which in 2013 held almost half of the outstanding loans to the bank. Interestingly though the bank has begun to shift emphasis in its income-generating portfolio. Four years ago, household loans were ranked third behind services and manufacturing in the distribution of outstanding loan value. By 2013, loans to households were the second most important part of GBTI’s portfolio and accounted for about 20 percent of outstanding loan balances.

The operational profile of GBTI is an interesting one. Like the other commercial banks, GBTI accepts deposits from customers and in turn uses the money to generate income. Customers continue to place confidence in the bank, even though deposits grew at its slowest pace, 12 percent, in the last four years. A review of its exposure profile reveals that the dominant focus of GBTI is the service sector which in 2013 held almost half of the outstanding loans to the bank. Interestingly though the bank has begun to shift emphasis in its income-generating portfolio. Four years ago, household loans were ranked third behind services and manufacturing in the distribution of outstanding loan value. By 2013, loans to households were the second most important part of GBTI’s portfolio and accounted for about 20 percent of outstanding loan balances.

While making loans from deposits remains its core business, GBTI is one of those companies that engages also in an array of activities with special features which brings it special benefits. It is involved in the Women-of-Worth project in which collateral is waived on loans funded by the government. It participates in the scheme that enables Guyanese with comparatively low-income to obtain a mortgage to buy or build a home. GBTI also is involved in administering a US$1.7 million IDB-funded financing facility for the Ministry of Agriculture. The thrust of that programme is to facilitate an expansion in the export of certain clusters of agricultural produce. In the last quarter of 2013, the government launched the small and micro enterprise initiative. The GBTI is also one of the partner financial institutions that has agreed to lend money to entrepreneurs under the arrangement.

Reporting

The preceding special activities are in addition to its core business of making loans from the deposits of customers. GBTI does not report separately the income from these special facilities in its financial reports, even though it acknowledges the tax savings from the special activities that it enjoys when determining its annual tax liabilities. However, GBTI does acknowledge in its “Notes” to the financial statements that the financial statements do not include balances that present any risk to it or for which it has no financial responsibility. Given the way the special initiatives with the government are structured, they present little or no risk at all to GBTI and open up access to the micro and small business market, one that it might not be most suited to service under normal conditions. The government either guarantees the loans or grants tax exemptions to the participating entities in what looks like a win-win situation for each. It would appear however that GBTI bears some risk or responsibility for the special financing facility since the value of the money held is included in its reported liabilities to third parties.

The preceding special activities are in addition to its core business of making loans from the deposits of customers. GBTI does not report separately the income from these special facilities in its financial reports, even though it acknowledges the tax savings from the special activities that it enjoys when determining its annual tax liabilities. However, GBTI does acknowledge in its “Notes” to the financial statements that the financial statements do not include balances that present any risk to it or for which it has no financial responsibility. Given the way the special initiatives with the government are structured, they present little or no risk at all to GBTI and open up access to the micro and small business market, one that it might not be most suited to service under normal conditions. The government either guarantees the loans or grants tax exemptions to the participating entities in what looks like a win-win situation for each. It would appear however that GBTI bears some risk or responsibility for the special financing facility since the value of the money held is included in its reported liabilities to third parties.

Conservative

One thing that stands out about GBTI is that it is a very conservative entity. It is not shy to shift the deposits of customers into safe investments when necessary. For example, in 2011, an election year, GBTI willingly put the bulk of its deposits into Treasury Bills and other securities that were guaranteed by government. This disposition is not surprising or unusual since self-preservation is nature’s first law, and the survival of any bank depends heavily on the confidence of depositors and their willingness to trust the judgment of the management of the enterprise. As a consequence, investments in short-term securities not only exceeded the creation of short-term loans and advances, it also exceeded the creation of loans and advances with longer maturities. This latter situation stems from the liquidity risk of the bank. Overall, total investment in securities and similar instruments were greater than the amount of loans and advances held by the bank in that particular year.

Assets are the things that help a business to bring in income and notwithstanding the upward movement in the gearing ratio of GBTI, in the case of a bank, the maturities of income-generating assets say much about the short and long-term investment strategies of a business. The short-term income-generating assets of GBTI have grown as a share of total short-term assets. In 2011, income-generating assets with maturities of one year or less made up 58 percent of current assets. That figure declined to 54 percent in 2012 but rose sharply to 66 percent in 2013. Notwithstanding the behavior of current assets as a whole, the bank has been careful to ensure that it grew its capacity to generate income even within the short-term class of assets. Loans and advances with short-term maturities grew by about 40 percent over the last few years and are far more distinguishable today as a source of revenue than they were three years ago. For example, in 2011, loans and advances with short-term maturities made up 23 percent of the current assets while investments made up 35 percent of the short-term portfolio. By the end of last year, the figure for loans and advances had grown to over 38 percent of current assets while that of investments declined to 28 percent.

Recalibration of Portfolio

The recalibration of the asset portfolio suggests that GBTI has set its sights on staking out a long-term future for itself in the banking sector. Important shifts have been observed in the composition of its outstanding loans with household loans emerging as a significant component of the portfolio. The realignment of its asset portfolio has been accompanied too by a reduction of current assets and an increase in long-term assets as part of the long-term investment strategy of the Bank. Applying a modified gearing ratio to the strategic financing model, current assets made up more than four hundred percent of the assets invested in the long-term future of the business in 2011. That figure fell to 389 percent in 2012 and further still to 359 in 2013. The change is driven by an expansion in the income-generating assets with long-term maturities.

At first blush, there appears to be some merit in this shift in business strategy for during this period, GBTI was able to expand its profits and increase the returns on asset. After tax profits grew by an annual average of 22 percent in the last three years and the returns on assets rose 13 percent from $2.01 in 2011 to $2.28 in 2013. The positive returns do not appear to be driven by the income-generating asset of loans and advances when marginal revenue is taken into account. Changes in total assets during the period 2009 to 2013 have produced average increases in income by six cents annually. The bank’s most important income-generating asset is loans and advances. Marginal revenues produced by this category of the portfolio averaged two cents during the same period, suggesting that marginal revenue from loans and advances has not exhibited convincing positive growth.

In 2010 and 2011, marginal revenue remained unchanged at two cents for every additional dollar spent on loans and advances. It increased to three cents in 2012 but fell to one cent in 2013. This calls into question the efficiency with which loans and advances are working, and might be evidence of the challenges arising from the continued efforts to make its new Core Banking Application fully operational as noted by the Chief Executive Officer in his annual report for 2013. Otherwise, one could ask if the composition of the loans and advances is structured and diversified appropriately.

Tightened Control

As with all major companies in this country, the management of GBTI exerts firm control over the resources of the organization and that was unlikely to change anytime soon. Over the last three years, management has tightened its control over the future of the organization. Resources under its control moved from 89 percent of long-term financing capacity in 2011 to 92 percent in 2013. Except for customers’ deposits, there is no threat to the management of the company from external sources. This is primarily because external financing makes up less than seven percent of the bank’s long-term financing. As a result, the future of GBTI will continue to depend on the quality of leadership of the company.

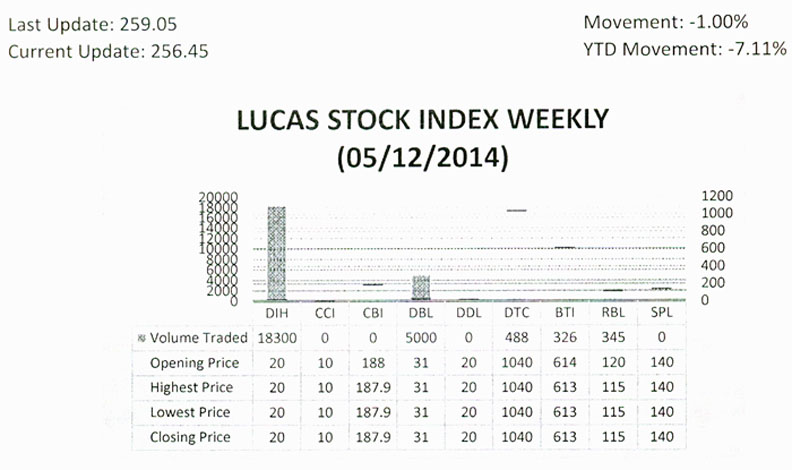

LUCAS STOCK INDEX

The Lucas Stock Index (LSI) declined 1 percent during the second period of trading in May 2014. The stocks of five companies were traded with a total of 29,414 shares changing hands. There were no Climbers and two Tumblers. The value of the stocks of Guyana Bank for Trade and Industry (BTI) declined 0.16 percent on the sale of 326 shares while the value of the stocks of Republic Bank Limited (RBL) fell 4.17 percent on the sale of 5,300 shares. In the meanwhile, the value of the stocks of Banks DIH (DIH), Demerara Bank Limited (DBL), and Demerara Tobacco Company (DTC) remained unchanged on the sale of 18,300; 5,000; and 488 shares respectively.