By Janette Bulkan and John Palmer

This article seeks answers to two questions. Firstly, which Government Ministry or agency deals with persistent underpricing of public assets? Secondly, will the draft State Assets Recovery Bill 2016 address the persistent failure of Government to deal with Customs fraud?

Here is one example from log exports: Over 100,000 cubic metres (m3) of wamara logs were exported to China in 2014 alone. The FOB price for wamara logs declared in Georgetown was in the range US$200-220/m3 in 2014. Containerized log freight and insurance Georgetown to China is in the range US$ 25-36/m3 according to the Guyana Manufacturing and Services Association. CIF reported by China Customs (not ITTO) was in the range US$700-1000/m3. The equation FOB+freight+insurance=CIF clearly does not work with these values, and the obvious explanation for the US$500/m3 discrepancy is transfer pricing. 100,000 m3 X US$ 500/m3 = US$ 50 million. No part of that sum was returned to Guyana’s Consolidated Fund.

The GFC denies that there is transfer pricing but provides no contrary evidence. Under-pricing leads to lower export commissions on the logs than the law provides, and on this massive scale the loss of revenue is considerable.

Our question is: Is this the equivalent of stealing State Assets?

Another source of corroboration about Customs fraud is in the report on ‘Illicit financial flows (IFF) from developing countries: 2003-2012’ from the Washington-based Global Financial Integrity (December 2014). IFF are estimated for Guyana at US$84 million in 2003 rising almost continuously to US$440 million in 2012. Around half of the illicit flows (US$1,464 million for 2003-2012) are attributed to export under-invoicing (http://www.gfintegrity.org/report/2014-global-report-illicit-financial-flows-from-developing-countries-2003-2012/ )

The objective of the Guyana Forestry Commission (GFC) is given in section 4 of the Guyana Forestry Commission Act (cap. 67:02 revised 2007) – to encourage the development and growth of forestry in Guyana on a sustainable basis. Ten functions of the Commission are given in section 5 of that Act, including (a) to develop, advise the Minister on, and carry out forestry policy; and (i) to administer the Forests Act 2007 [actually the Forests Act 2009], including – (i) carrying out the Commission’s functions under that Act; and (ii) collecting and recovering all fees, charges, levies, premiums, fines, penalties, costs, expenses and other monies payable under that Act. Section 73 (1) of the Forests Act 2009 states that ‘All forest produce on, or originating from, public land is the property of the State until the rights to the forest produce have been specifically disposed of in accordance with this Act or other written law’. Section 80 (1) of the Forests Act 2009 empowers the Minister to make regulations to impose …fees, charges and levies. The charges include royalties, which is the only kind of forest tax to be paid automatically into the Consolidated Fund under section 80 (3), all other monies to be retained by and paid into the general revenues of the GFC. Note that this contradicts section 15 (3) of the Timber Marketing Act (cap. 67:04 of 1973) which requires fees associated with timber exports to be paid into the Consolidated Fund, and the regulations under that Act (including payment of fees) carry over through section 85 (1) of the Forests Act 2009. Note also the contradictions with policy and plans (below) about which agency retains which fees.

No regulations have yet been proposed or gazetted under the Forests Act 2009 but the Forest Regulations 1954/1982 and the Timber Marketing Regulations 1973 have continued validity because of control passed through section 85 (1) for the Forests Act 2009.

Royalty charges are authorised by Regulation 2 of the Forest Regulations, and area rental fees by Regulation 7 (2) for State Forest Permissions and Wood Cutting Leases (WCLs) and by Regulation 7A (2) for Timber Sales Agreements. Area rental fees for State Forest Exploratory Permits are mentioned in section 4, page 6, of the GFC Manual of Procedures for Exploratory Permits (revised April 1999) and are charged in practice by the GFC but apparently the drafters forgot to include legal provision in the technically weak legal drafting of the Forests Act 2009 (compared with the infinitely better draft of 2004).

Export commission on unprocessed logs has been charged by the GFC since before 1991. Until 2009, all log exports were charged a nominal commission of 2 per cent of the reported FOB value. Since 2009, rates vary by timber species. We have been unable to locate the basis for the GFC charging the export commission.

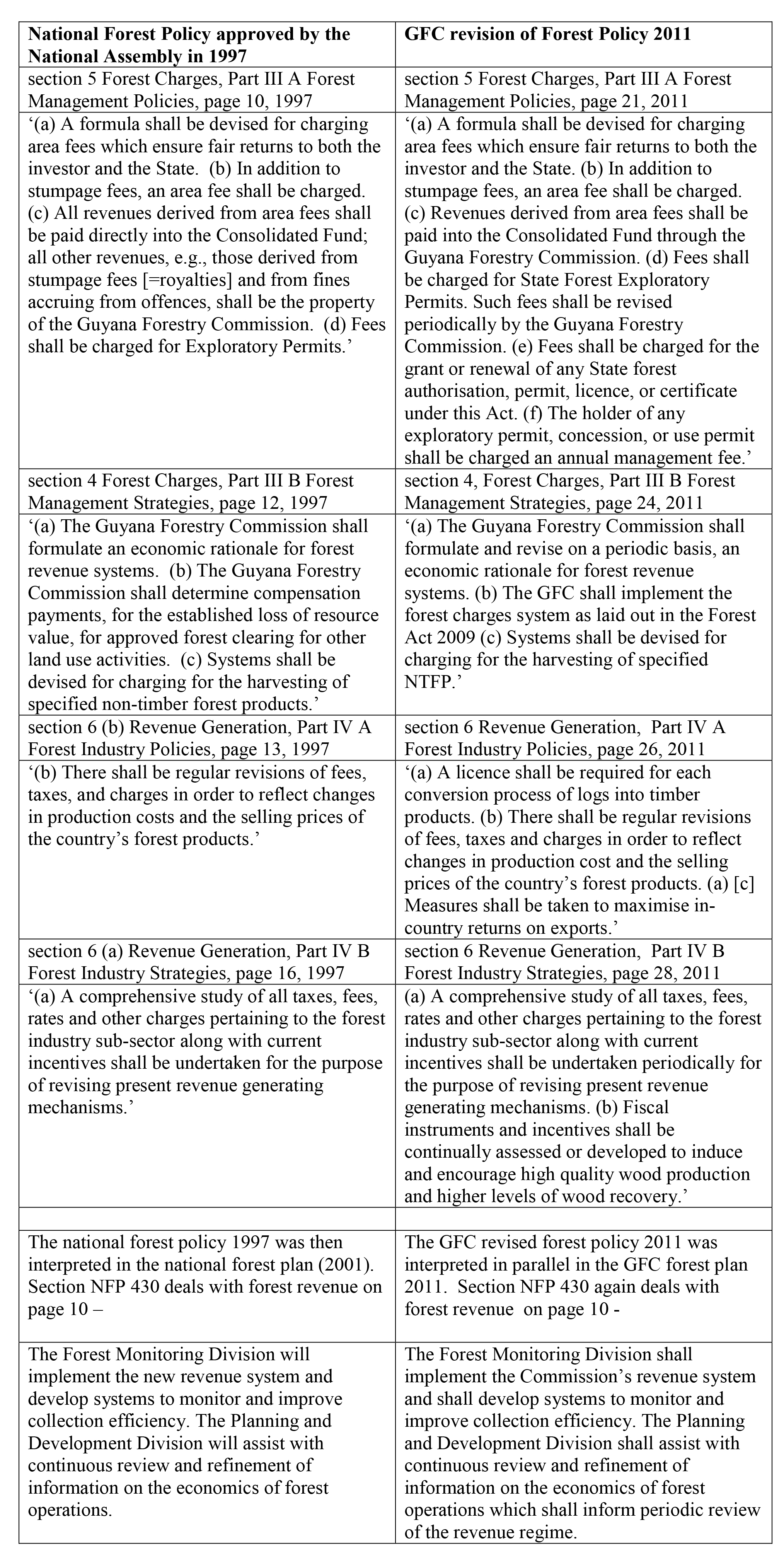

There was almost no implementation of either the approved national forest policy (1997) or the national forest plan (2001). Both policy and plan were revised in 2011 but without discussion in or approval by the National Assembly. Likewise, negligible progress has been made on implementing the 2011 revisions of the forest policy and forest plan, as shown by the similarities between the two sets of documents in the table below.

During the 19 years since the 1997 national forest policy, the royalty and area rental fees for logging concessions have been unchanged, the provisions in law for performance deposits and bid premia for concessions have been applied we think only once, and massive Customs fraud has been perpetrated with GFC connivance through under-valued and mis-declared log exports.

During only 2014, Bai Shan Lin through log exports under its own name and through fraudulent use of rented concession documents earned around US$8 million through under-declaration and transfer pricing. Yet this group of companies protests that it cannot pay US$0.5 million in long outstanding debts of forest taxes and penalties to the GFC and somewhat more to the Guyana Revenue Authority.

The failure to implement national policy on forest revenue generation had even by the mid-1990s left the forest taxes of Guyana among the lowest in the world; the extreme case being Barama’s area rental of just over US$2,000 per year for 1.61 million hectares (Mha) of forestland. The commitments for improvements to forest revenue in the policy from 1997 have not been implemented, so government revenue income has been consistently and deliberately deprived; Guyana is not obtaining proper value from the public assets in the State Forests.

Is this the equivalent of stealing State Assets?

If these two situations – deliberate and continued under-collection of forest-based revenue and Customs fraud over many years – are not SARU cases, who should be prosecuting and under what laws? Of course the logs harvested from State Forests and shipped to China cannot be retrieved and restored to be living trees again, so to that extent these State Assets cannot be recovered. But the lost revenue can be recovered. And the private property and other assets acquired through the contraventions of the civil service code of conduct (Integrity Commission Act) would surely come under the purview of SARU.

If they are SARU cases, let us hope to see them high up in the list for early prosecution. And be sure to inform the Chinese Ambassador about the roles played in Guyana by enterprises partly owned by the Government of China and which have been failing to comply with codes of conduct for transnational Chinese companies issued by the Ministry of Commerce and State Forestry Administration in Beijing; as previously pointed out in the independent Press in Guyana (see Guyana – Stabroek News Letter to the Editor, Monday 27 April 2015 – http://www.stabroeknews.com/2015/opinion/letters/04/27/super-profits-by-asian-transnationals-generated-partly-from-excessively-favourable-investment-arrangements-provided-by-govt/ – Super-profits by Asian transnationals generated partly from excessively favourable investment arrangements provided by gov’t).