In this section we consider the measures announced by the Minister, analyse them, evaluate their impact and discuss the extent to which they meet the economic benefits of the stakeholders

Section 6 of the 2017 Budget Speech contains a staggering fifty seven paragraphs of Budget measures, some of which are regulatory rather than fiscal. This follows a substantial number in 2016 and a possible impact would drive parts of the economy underground.

Only some of these carry an estimated cost and a number of them have not inconsequential compensating savings. We now look at those measures and offer our comments.

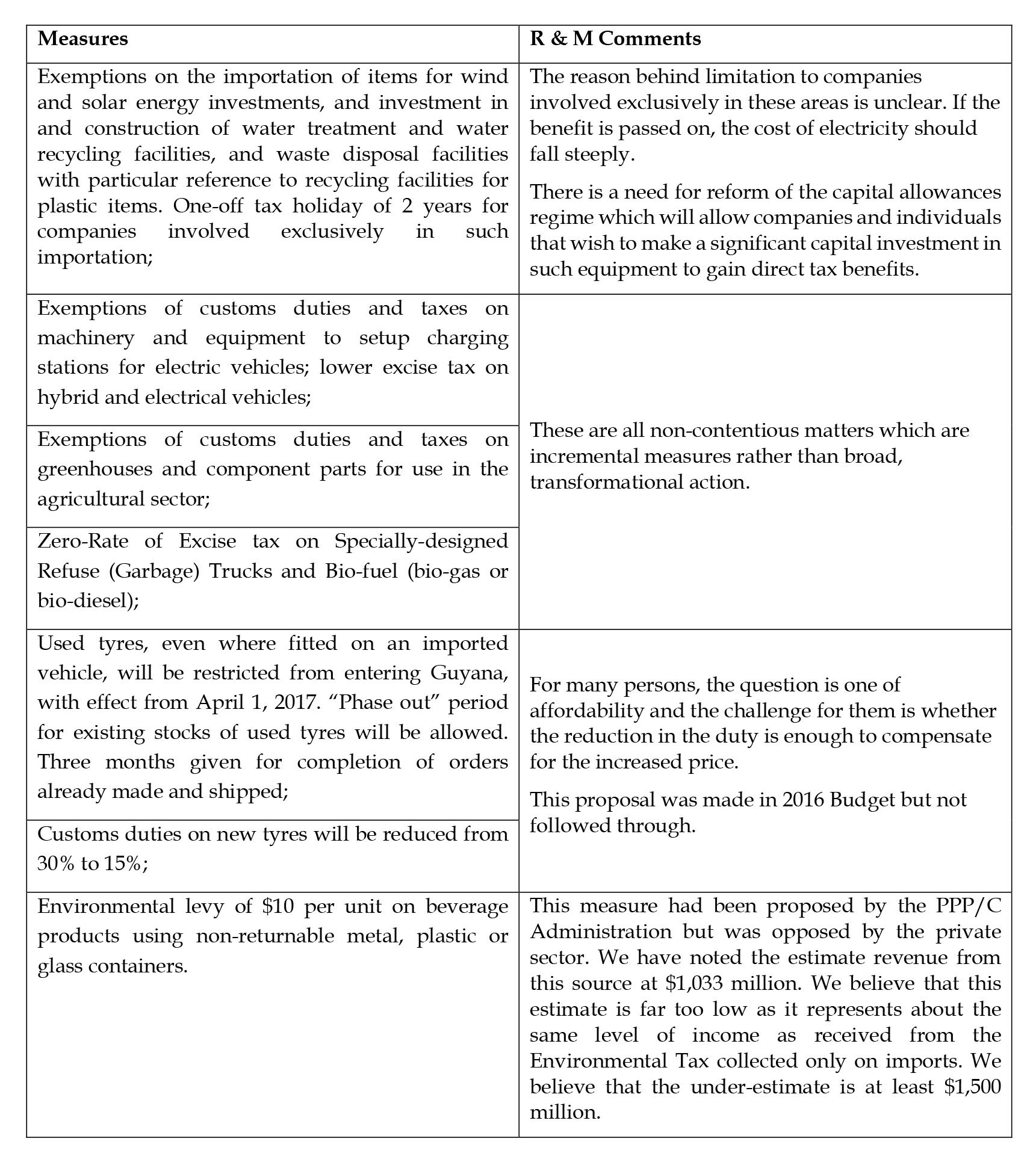

Measures in Support of Our Green Agenda and Protecting the Environment

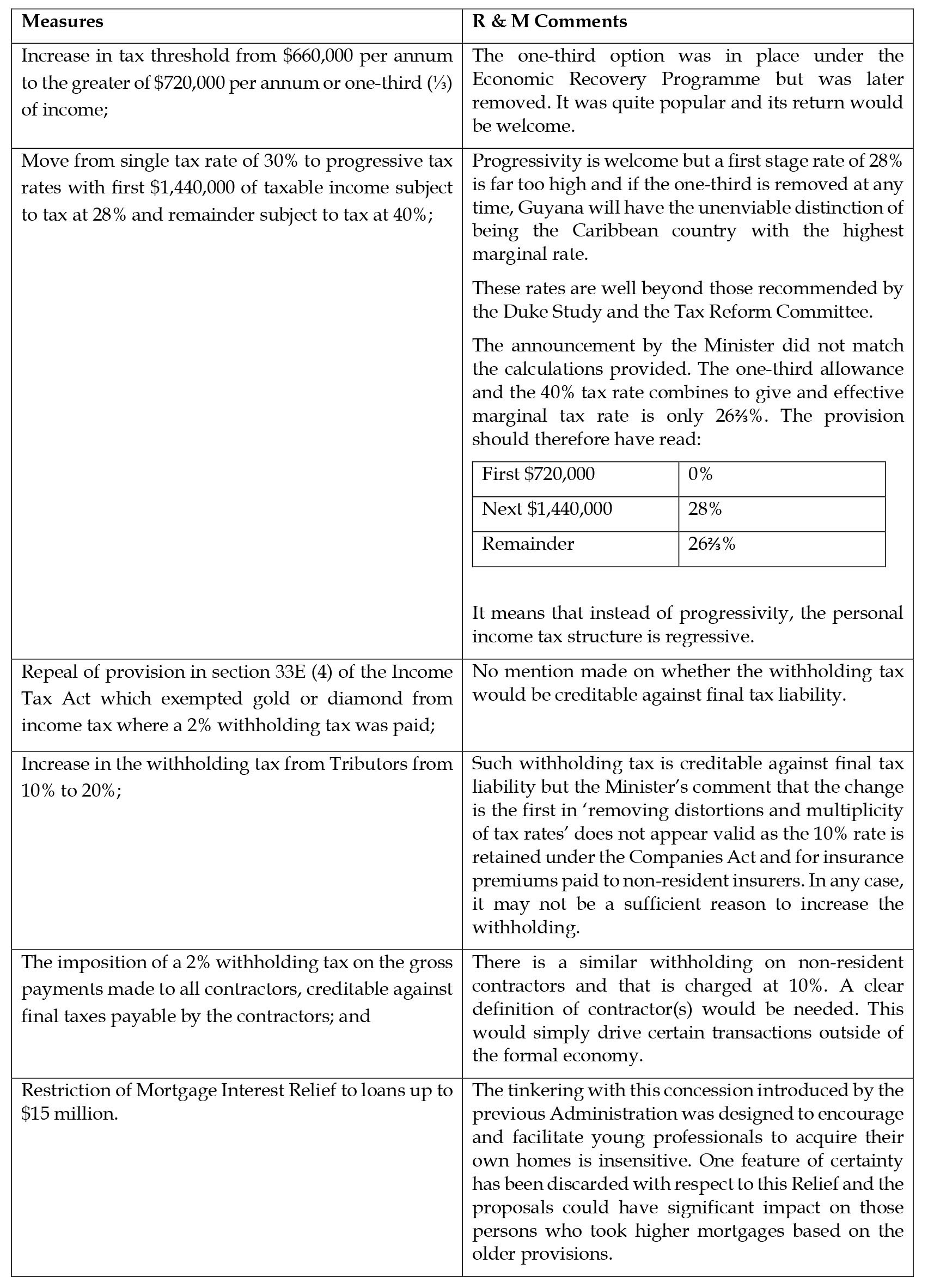

Measures to Reduce Inequality and Increase Disposable Income

Measures to Reduce Inequality and Increase Disposable Income

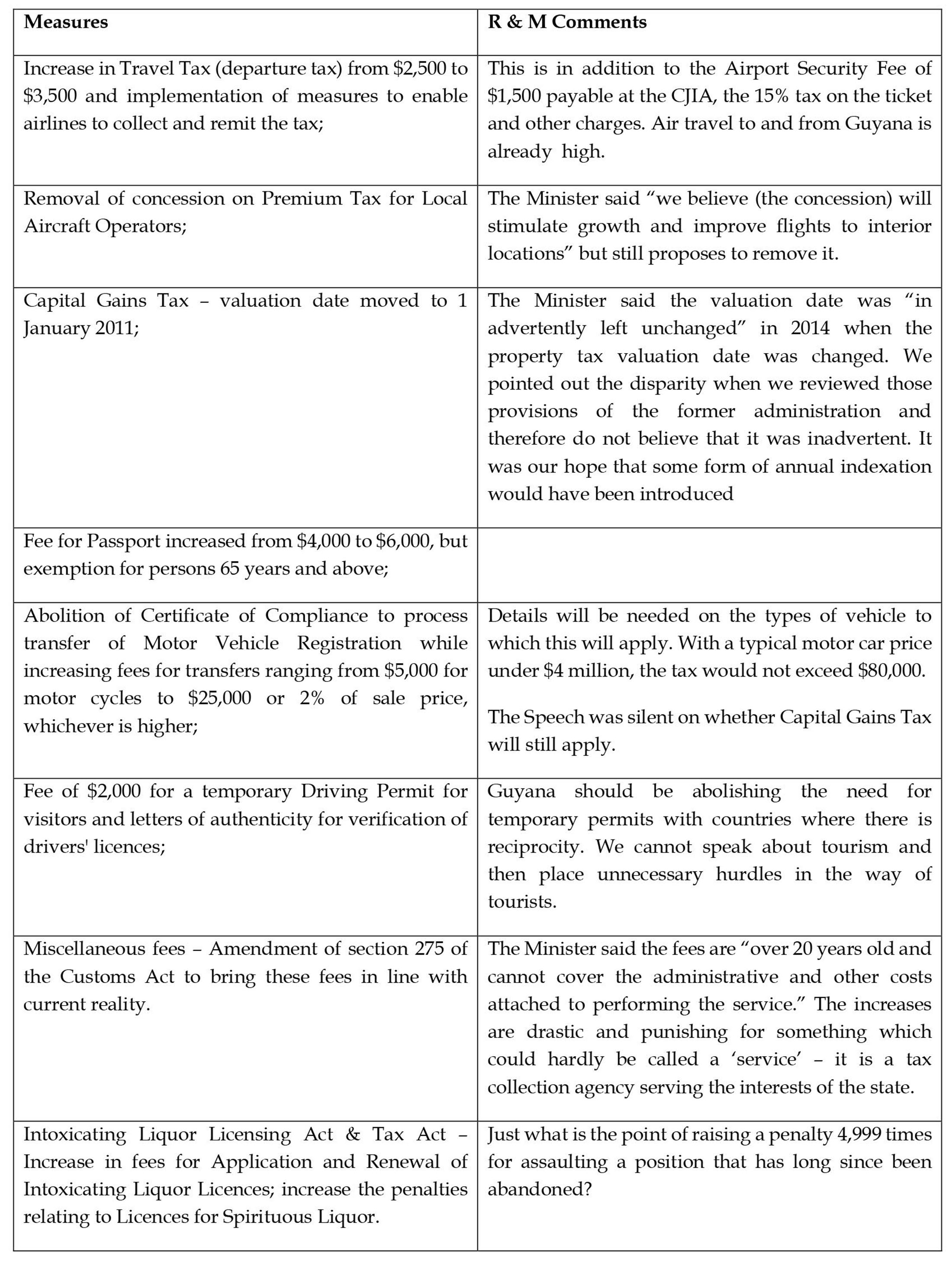

Measures to Spur Economic Growth

Measures to Spur Economic Growth

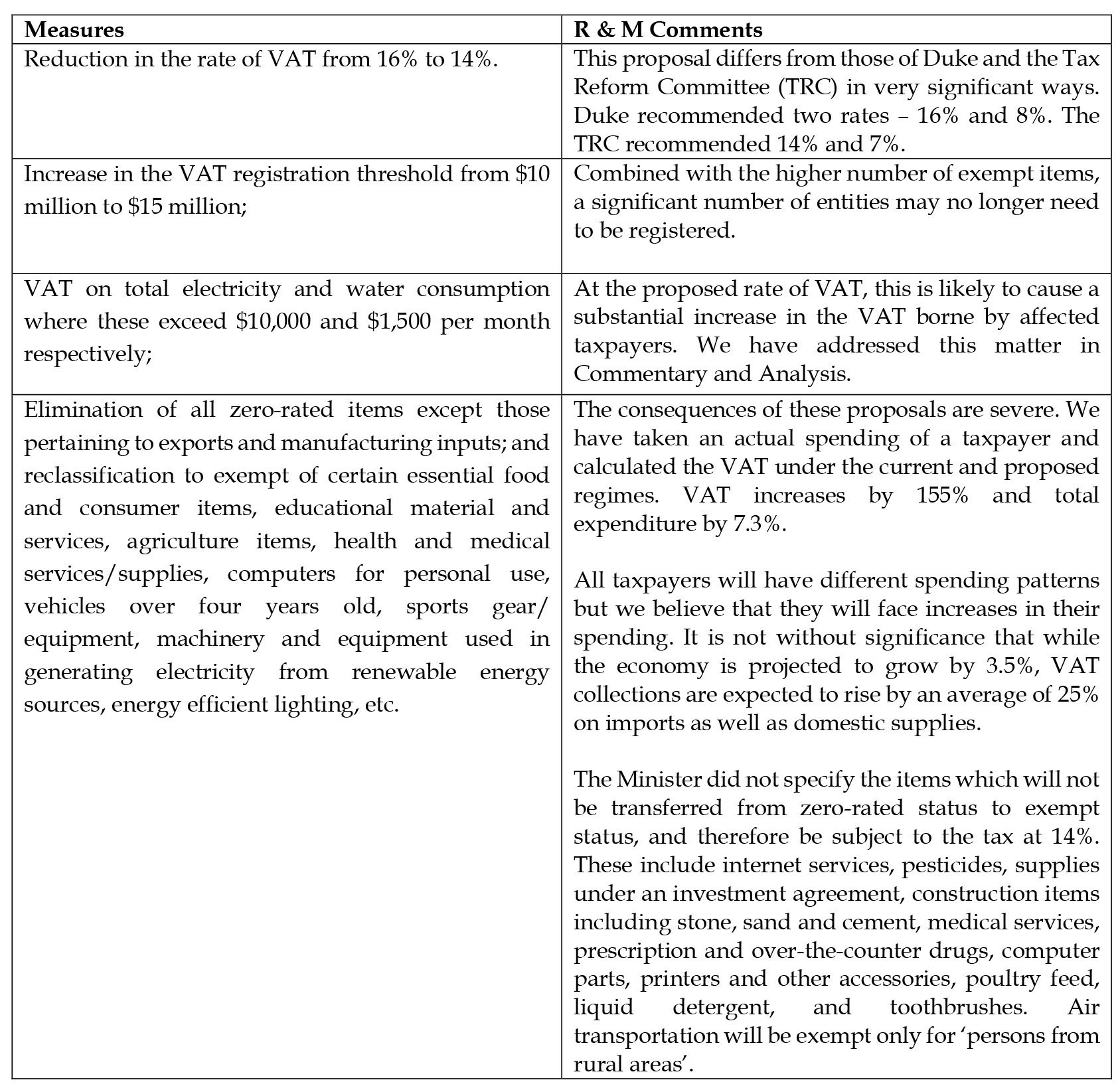

Value-Added Tax (VAT)

Value-Added Tax (VAT)

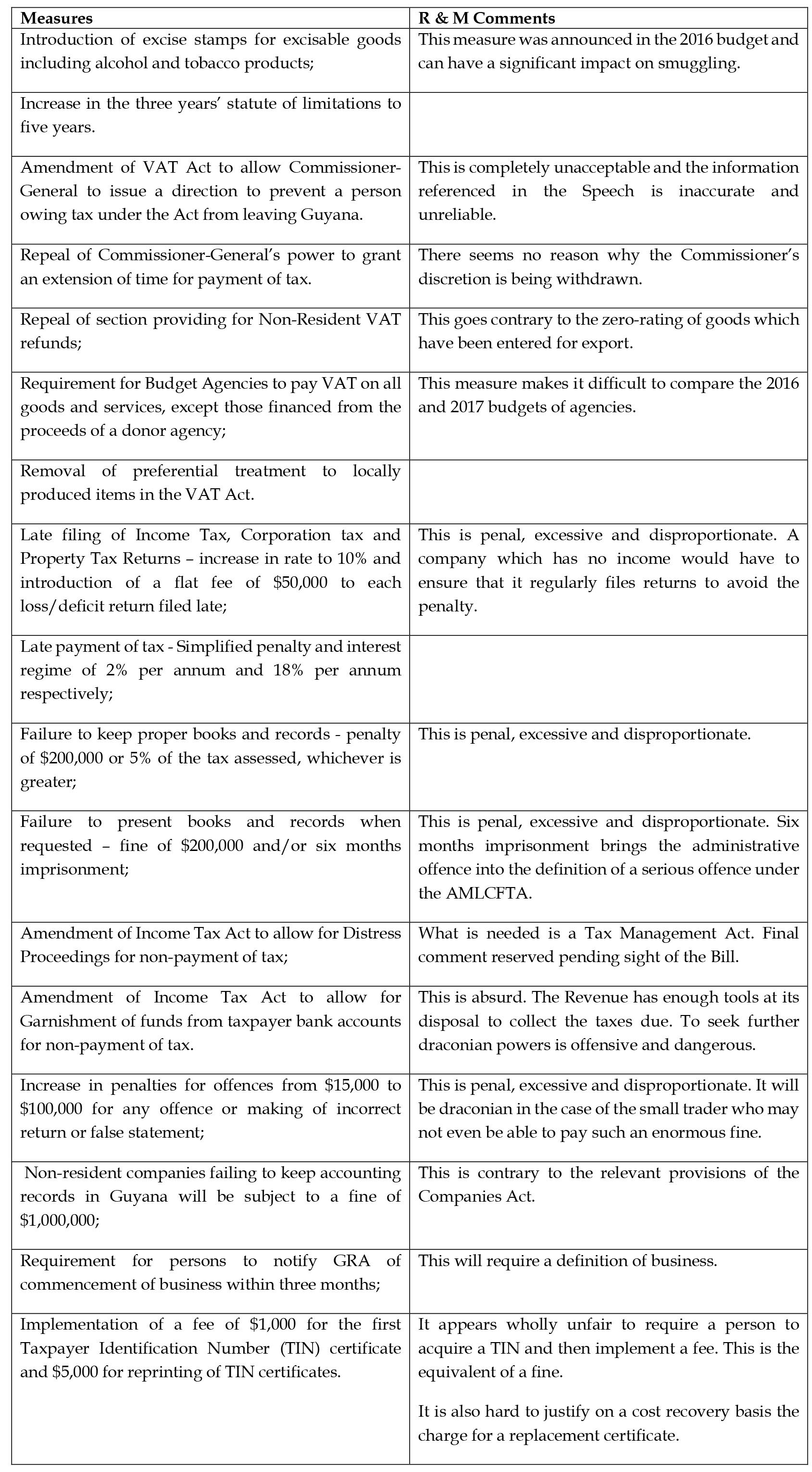

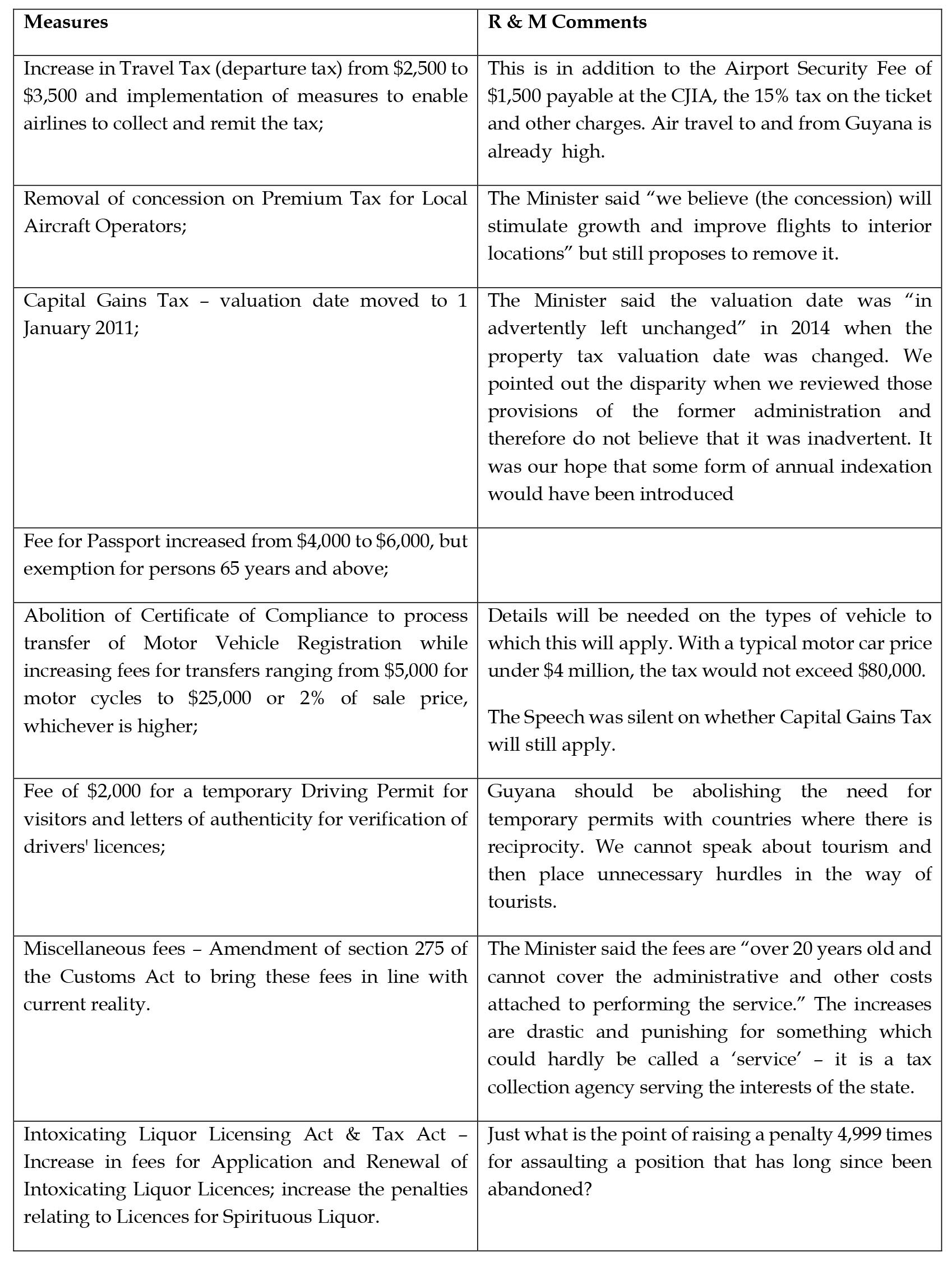

Measures to Improve Tax Administration

Measures to Enhance Revenue

Measures in Support of the Elderly

Measures to Improve Workers’ Disposable Income

Overall comments

Overall comments

We are disappointed that the Minister once again has not provided the cost of each of the proposed measures. In those instances where values are indicated, we believe some of them are way out. While we cannot conclude on whether the Minister’s speech matches the proposed legislation, we believe that at least one of the proposals is misguided and would cost the state a substantial sum. That particular proposal needs to be revisited.

The commitment to client friendly and business friendly tax environment may escape the taxpayers faced with charges for tax services and heavy penalties for administrative breaches. If the tax authorities wish some equity, the law must provide for the payment of equivalent interest on amounts owed by the GRA as it does on amounts owed to the GRA.

The Tax Measures proposed did not follow the recommendation of the Tax Reform Committee to abolish and slash concessions and exemptions on key political and other players.