Part 1

Decline in profits

The Guyana Bank for Trade & Industry (GBTI) has reported its half-year profits for the year 2017. In a Stabroek News article on August 23rd, it was reported that the bank’s after tax half-year profits stood at $603 million, down a whopping 37 per cent ($358 million) compared to $961 million after tax profit during the same period in 2016. The  reported information is not the type of news that shareholders of the bank would want to hear. The decline in profits, while troubling to shareholders, does not put the financial soundness of the institution at risk. This is one bad year of many years of successful billion-dollar reports of profits. The half-year performance report follows an alleged fraud which consumed some $941 million and cost some staff members their jobs. Fraud is not uncommon in the financial world, but the size of the fraud is always a matter of interest. Since the affected bank is a major part of the banking system in Guyana, it is natural for people to wonder about the decline in profits and its implications for their ability to borrow. There is much in the relationship between banks and their customers. This article will look at the relationship between banks and households since the latter are the ones with the most to lose.

reported information is not the type of news that shareholders of the bank would want to hear. The decline in profits, while troubling to shareholders, does not put the financial soundness of the institution at risk. This is one bad year of many years of successful billion-dollar reports of profits. The half-year performance report follows an alleged fraud which consumed some $941 million and cost some staff members their jobs. Fraud is not uncommon in the financial world, but the size of the fraud is always a matter of interest. Since the affected bank is a major part of the banking system in Guyana, it is natural for people to wonder about the decline in profits and its implications for their ability to borrow. There is much in the relationship between banks and their customers. This article will look at the relationship between banks and households since the latter are the ones with the most to lose.

Six banks

Before doing so, it would be important to remind

readers that the banking system in Guyana consists of six commercial banks. In addition to Citizens Bank, Demerara Bank, Guyana Bank for Trade and Industry and Republic Bank which are part of the stock index that is prepared by this writer, there are two additional banks. One is the Bank of Baroda and the other is Scotiabank. According to data released by the Bank of Guyana, the commercial banks are generally in good shape. They are adequately capitalized and they are stable. In light of this observation, it is useful to get a sense of where the market stands in relation to the banks.

Market value

Around this period in August 2016, the market value of the four commercial banks that are part of the stock index prepared by this writer stood at $74.34 billion. In 2017, the market value is $73.75 billion. This change reflects a decline in value of the companies by less than one per cent. It should come as no surprise to anyone that the market value of GBTI was down 11 per cent, declining from an amount of nearly $18 billion to $16 billion. But the decline in market value is not seen in GBTI alone. Demerara Bank Limited also saw a decline by five per cent in the value of its market capitalization. This decline occurred even though DBL did not have the negative experience of GBTI. Nonetheless, the overall situation of the commercial banks can be regarded as satisfactory despite the specific problem of fraud identified above and the distortions in the foreign exchange market earlier in the year. These observations would bring no comfort to the shareholders of GBTI, whose expectations of dividend payments for 2017 might now have to be tempered.

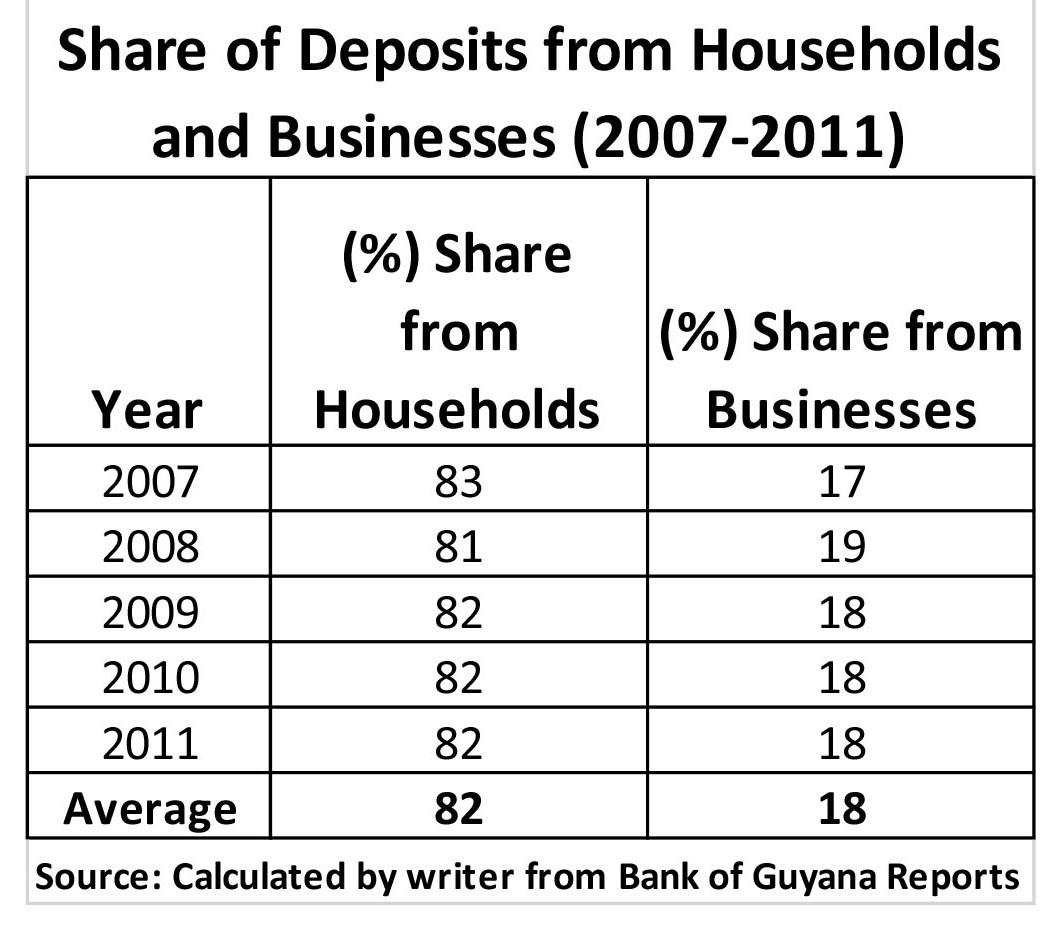

Interest in the performance of the banking system goes beyond that of shareholders of commercial banks. Households and businesses have a keen interest in what happens in the banking system. They represent the backbone of the intermediation services. In fact, it is their complementary relationship that makes the banking system tick. The banking system is one of those marketplaces where households have a large presence but seem to exert very little influence. The presence of households is reflected in the amount of money that they deposit in the banks by opening various types of savings accounts. Table 1 below shows the share of bank deposits between households and businesses in the period 2007 to 2011.

TABLE 1

The data in the Table 1 reveals that households provided 82 per cent of the money from the private sector that commercial banks had in their possession during the period in reference. At the same time, businesses contributed 18 per cent of the deposits. Banks therefore depend heavily on households to make their intermediation service work. Interest rates offered to depositors during that period were not very attractive. Starting at 3.15 per cent in 2007, the interest rate offered by commercial banks to depositors declined 37 per cent to reach 1.99 per cent in 2011.

Businesses

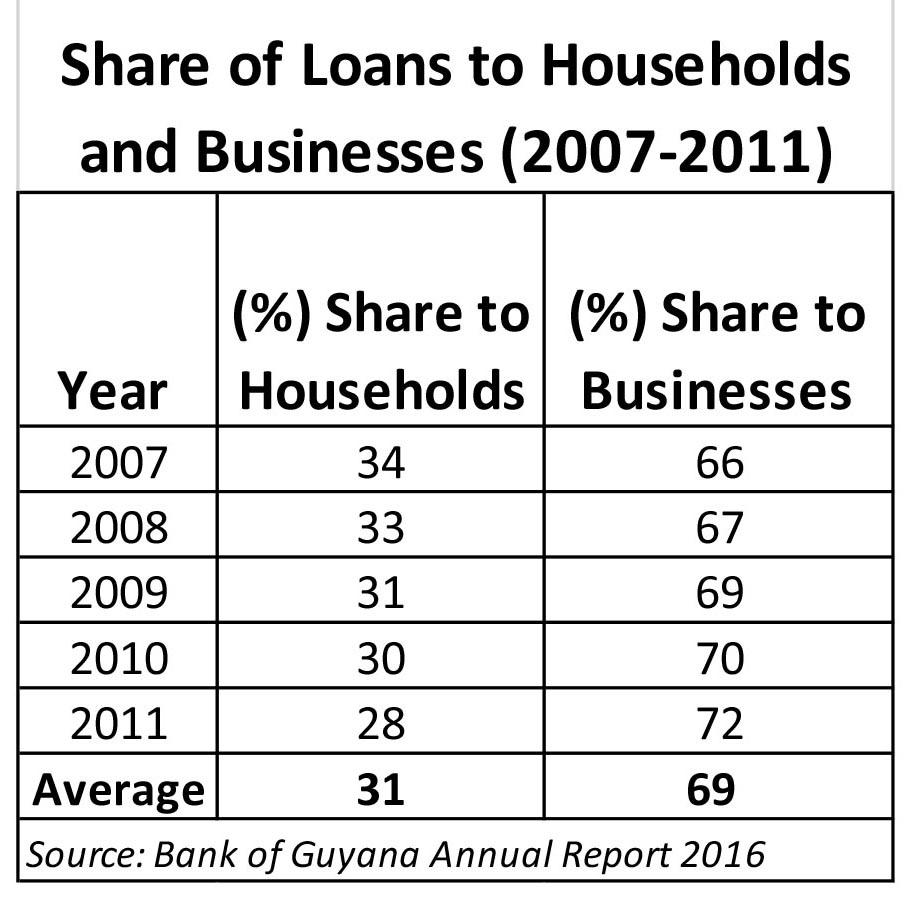

Just as they look to households to put money into the banking system, they look to businesses to take it out of the banking system and help put it into the economy. Table 2 below for the corresponding period shows that businesses borrow the bulk of the money that banks put into the economy.

TABLE 2

Second time-period

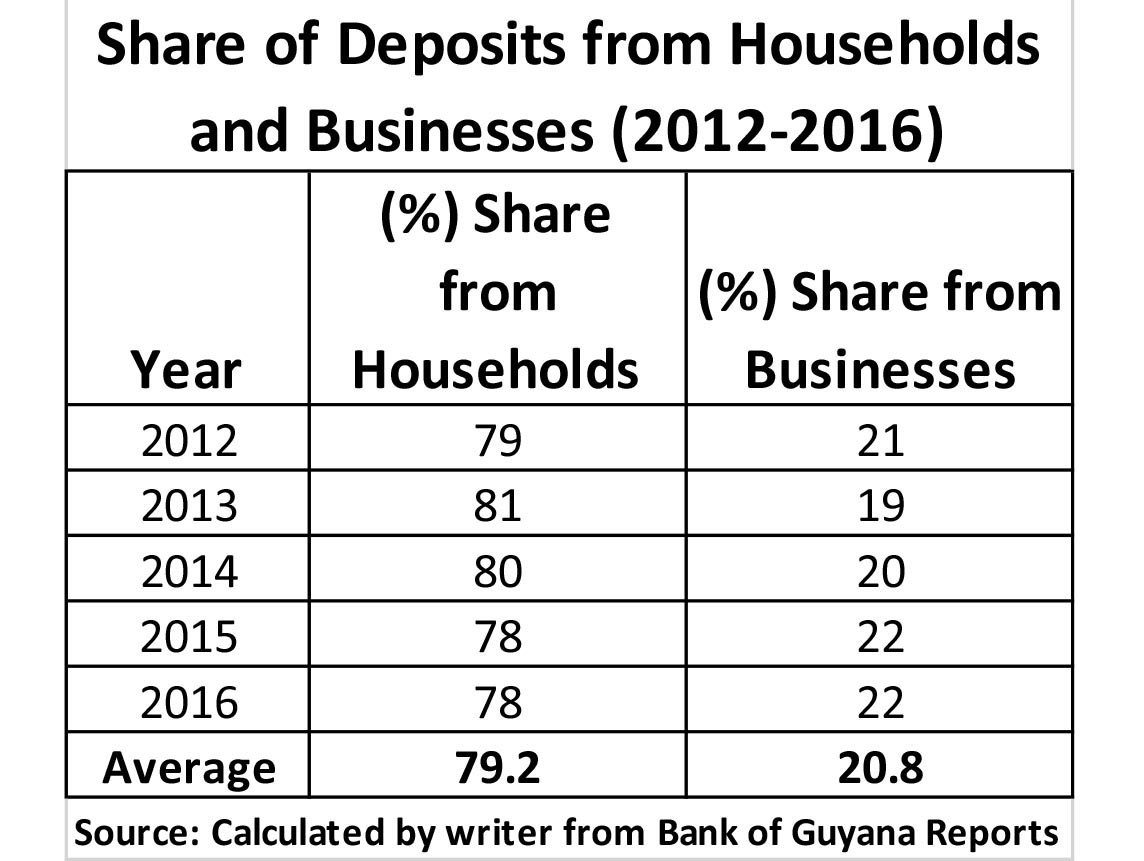

The second time-period under review displays its own set of characteristics. The share of deposits from households declined nearly three percentage points from money deposited in the prior period. Interest rates on savings accounts continued their decline too and did so by 25 per cent from 2012 to 2016. It is not surprising that households did other things with their money as against putting it into the banking system as suggested by the data in Table 3 below.

TABLE 3

The cheaper cost of borrowing by the banks largely from households often sets up the cry of foul, when it is the latter’s desire to borrow the money they put in the bank. The lamentation is often triggered by the high cost associated with accessing the money.

(To be continued)