A column by Transparency Institute Guyana Inc

Recently, the number and prominence of foreign analysts who have corroborated the early view expressed by local analysts have increased. This is the view that the contract is heavily weighted against Guyana. Two of these foreign analysts have been OpenOil and the IMF. Yet, there is one aspect of the consideration of how bad a deal this 2016 contract has been that has escaped the discussion thus far. This article is the first of several contributions that TIGI intends to make for the purpose of highlighting gaps in our understanding of what took place and the need for accountability.

Activists are pointing out that there is no luxury of discretion provided for in the law on the part of ministers of government, or the President, with regard to the timing of the deposit of the US$18 million signing bonus into the consolidated fund. However, it appears that our leaders applied a discretion actually provided in our petroleum legislation wrongly and this is likely costing the country many times the US$18 million.

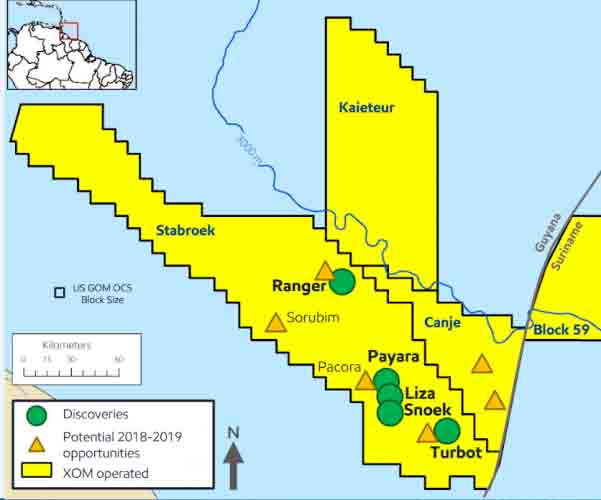

It is not that it has been completely missed in the discussion as much as that the impact of the violation of the provision regarding maximum blocks (and there is little question that there is a violation) has lain below the radar even when the aspect of the contract on which it rides, that is, the size of the Exxon Stabroek block, is discussed. That aspect is the fact that the large tract of seabed under the control of one company, has been issued under a single licence. In other words, the control of 26,800 sq km as stated by Exxon is not so much the problem as that the area is not controlled under separate licences as provided for under Guyana law.

It is difficult to appreciate the point fully without an explanation of the meaning of “blocks” according to the Guyana law. In the oil industry, the word “block” is used in two related senses: “graticular block” and “contract block.”

“Block” in the Sense of Graticular Block

The first meaning of the word “block” is “graticular block”, that is, the basic unit of area of land or seabed. Think of this as analogous to “one square foot”, the basic unit of area when specifying the amount of land in a lease. The 1986 petroleum act adds the adjective “graticular” when this is the meaning of the word “block”.

According to Part II of the Regulations dated 12th July 1986, a “graticular block” (the basic building unit of seabed) is defined in terms of 5 minute intervals of both longitude and latitude. These regulations provide for a maximum of 60 blocks – in this case, graticular blocks – to be the area available in any single licence.

Contract Block (or Licence block)

The second use of the word is in “contract block”. Think of this as analogous to the entire area of land leased in a lease agreement. So we can have, for example, a house lot of a total land area of 1500 square feet made up of individual squares 1 foot long by 1 foot wide. The Exxon “contract area” is an area of approximately 317 unit squares (according to the contract diagram); each unit square intended to represent a graticular block. According to Annex A, “The area comprises approximately 26,806 square kilometers described herein consisting of graticular blocks”.

This definition is in common use in the industry, with governments demarcating a pre-defined group of graticular blocks to make up a “contract block” as part of a petroleum exploration policy and programme. A company interested in a license would identify a listed contract block as set out on an approved diagram, and, in these days, obtain as the result of a successful bid at an auction. (See reference below to the POT-M-857 block with area of 1,215 sq.km).

However, it appears that Guyana never advanced its efforts made in 1981 to draft such a comprehensive policy and thus there were no such pre-defined blocks as late as 1986 when the current Petroleum Act was passed nor in 1999 when the licence was issued to Esso. A document published by the GGMC titled “Guyana Geology and Mines Commission Block Reference Map for Petroleum Exploration & Production Licence pursuant to Part 2 of the Petroleum Regulations of 1986” appears to be for record-keeping purposes. Nevertheless, it is a late record, as it did not appear to exist in 1986 nor in 2016 if we can be guided by its date of creation (“February 9, 2017”).

Interpretation of the Provision for Maximum Number of Blocks

The interpretation of the provision relating to the maximum number of blocks must be understood in the context that unlike in Brazil, Sao Tome, Mexico, etc., the blocks available were not pre-defined or demarcated and published as such. Therefore, the law depends upon that maximum of 60 graticular blocks to establish the “contract block”.

Kenya

Since 2006 Kenya began to reduce its block size. In that year, an area of 20,000 sq km was shared among 37 blocks (541 sq km each) instead of 25 (800 sq km each). In 2013, it was reduced further to 435 sq km each.

Trinidad

Closer to home, the Trinidad law provides that “… (b) in no case shall an area in excess of five blocks of eighty-five thousand acres each be granted under one licence; (c) every grant of such licence shall be in respect of contiguous blocks.” Five blocks of 85,000 acres each work out to be a mere 1720 sq km.

It can be shown that the area of each graticular block, as provided for by Guyana law, is 84.55 square km each. Sixty of these would be 5,073 sq km (more than 6 times the Kenya pre-2006 standard and just under 3 times the Trinidad maximum per licence). It is apparent by comparison that the Guyana maximum per licence was already very generous. The discretion in paragraph 13(3) to which this maximum is subject could not be intended to make the area awarded even more so. There is a hint of its purpose in the next clause, i.e., (4) which refers to the need to ensure that blocks awarded make sense geometrically and economically. This is in the contemplation of an active programme of exploration, partial surrender of the licence block after a number of years of unsuccessful exploration as provided for at renewal time, and best of all, the removal of discovery graticular blocks from the original area. Without the discretion to increase the size of the adjoining contract block, which may already be 60 graticular blocks, a piece of the original contract block could be left stranded, for example, being too small to be economical to another investor. In any event, the award of multiple times the maximum blocks was always legally available – under multiple licences. Seen in this light, the award of the said area under a single licence is a material breach of the regulations, unsupported by enlightened practice even prior to 1999 and has, as will be shown below, resulted in material harm to the country. It would have served no useful purpose to Guyana. Instead, it has rendered the country a wholesaler of that large tract of seabed and gifted to one oil company Guyana’s ability to conduct the retail services attendant upon the availability of multiple licenses.

Size of Signing Bonus

There was, and still is, a great outcry about the small signing bonus paid by Exxon to the Government of Guyana. Large signature bonuses are a feature of a bid system which Guyana has managed to deny itself. In fact, the largest signature bonuses are a feature of a system which relies on the interplay among the following:

Recycling of blocks (Give up half the block if you do not find anything in 7 years. Let someone else try.)

Proximity to, and better yet, contiguity with, blocks known to be rich in petroleum.

Active involvement by government professionals in the generation and provision of geological and seismic information (From seismic surveys, mappings, experience with well-digging, etc).

The competitive bidding by interested petroleum companies for the right to hold a licence for a given contract block (several graticular blocks together).

This is where the size of the ExxonMobil contract block matters most. The largest area featuring in the recently completed 15th round in Brazil’s auctions was the POT-M-857 block with an area of 1,215 sq.km. The signature bonus which was paid by Wintershall Holding, the winner of the block, was R$57,304,800 (equivalent of US$16,983,729). The total area of the blocks (all offshore) featuring in the auctions was 16,400.30 sq.km. The total signature bonus earned on this area consisting of 22 blocks was R$8,014,551,847.51 (US$2,375,315,446). Therefore, an area amounting to 60% of the ExxonMobil Stabroek block generated 130 times the signing bonus. These are for exploration rights and production rights if petroleum is found in commercial quantities.

What is behind the willingness to pay top dollar for exploration and production rights in Brazil? It is the proximity to the known petroleum reserves of the pre-salt areas. In the words of the executive of the company which along with Petrobras bid the astronomical R$ 2,24 billion signing bonus for block C-M-346 with an area of only 3,596 sq.km. in the previous round, “one of the reasons that led companies to bid (so high) … is because (the area) is close to pre-salt areas.” This executive was Pedro Parente, the CEO of Petrobras which partnered with ExxonMobil Brazil in this successful bid.

It should be clearer what successive governments of Guyana have done by issuing such a large tract of seabed under a single licence. Note well that the problem is not that it was issued entirely to one company, but all under a single licence. The Australian rules, for example, state explicitly that there is no limit to the number of licences that could be issued to one company.

Such a large expanse of seabed makes proximity and contiguity meaningless – to Guyana, that is. There is nothing to stop Exxon from privately farming out the exploration of those blocks (however many it chooses to divide them into) and benefitting from the equivalent of signing bonuses and other payments that would otherwise have been due to Guyana. In other words, there is nothing to stop Exxon from privately administering the rest; equivalent to 6 C-M-346 sized blocks (3,596 sq km) that earned Brazil US$1,124,847,802 in the 14th round auctions in February this year. Or equivalent to 40 C-M-789 sized blocks (664 sq km) that earned it R$2.84 billion (US$834 million) in the 15th round completed last month.

Had our leaders not misused the discretion provided, the more licences that would have been issued, (somewhere between 6 and 40), the more licences would have been up for auction as they are recycled by being relinquished after seven years or oil discovered under separate production sharing agreements.

Generosity

So, had not the 26,800 sq.km. of seabed been issued under a single licence, then the GOG would have been in a position to limit its generosity to Exxon and perhaps even keep it within understandable bounds. For example, all the terms to which the Stabroek Block is subject could have applied to the maximum allowable under Guyana law, that is, an area containing 60 graticular blocks or 5,073 sq.km. The remaining area of 21,729 would have been under Exxon but subject to at least 5 other licences.

The tiny country of São-Tomé and Principe (STP) appears to have managed its acreage much better than Guyana has. Over the period from 2005 to 2015, its Joint Development Zone with Nigeria yielded a total of US$274 million dollars of signing bonus. The total area involved was only 4,598 square kilometers. So an area of less than the maximum area per licence available by law in Guyana (5,073 sq km) yielded this sum in STP. Just last month a consortium of British Petroleum and Kosmos Energy signed a production sharing agreement with that country’s National Petroleum Agency involving a signature bonus of US$10 million. The area of each of the two blocks (US$5mn each) involved was less than 7,000 sq km. This interest on the part of oil companies is on the mere promise of oil discovered in neighbouring countries – none has been discovered in STP’s waters to date.

Questions

In 1999, the tiny country of 200,000 people, São-Tomé, was arranging with Schlumberger Exploration Services to collect geological and seismic data and demarcate licence blocks, many of which would be less than 1,000 sq km each, all in preparation for a system of auctions. In that very year, our leaders simply either misinterpreted or flouted our laws, handed over 26 times that size to Exxon, and waited.

Where were the trained professionals who should have guided them? Were they silent or were they not listened to?

What was the level of technical support that the nation was paying for? Did we get it?

Why 17 years after 1999 did our leaders behave as though they had never heard about petroleum auctions? Since the 1980’s petroleum bidding was becoming the preferred means of dealing with oil companies. The GGMC has held auctions for mining on land. An extract from a notice still resident on the net reads “Auction of Prospecting Licence parcels on stock maps 35SW, … 9NE and, medium scale parcels including available areas in the former Aranka and Five Star PGGS areas on Wednesday, November 24th, 2010”at 10:00 hrs at the Guyana Girl Guides Association building, Upper Brickdam, Georgetown.

Final Questions

In an article by Carole Nakhle titled “Licensing and Upstream Petroleum Fiscal Regimes: Assessing Lebanon’s Choices” the point is made that “It is also advisable that host governments not award all their territory for exploration and exploitation simultaneously. Through a gradual award of blocks, the government retains the flexibility to make some changes in the terms and conditions of future awards, following newly acquired information”.

Are the companies now knocking on Guyana’s door going to be the beneficiaries of our misguided generosity as well? Do we need to be in so much of a hurry? Surely there is time to put a legal framework in place to support the proper demarcation of remaining blocks and blocks due to be relinquished according to the renewal of licence terms (unless our governments have managed to tie our country down to similar Exxon-type agreements that have made useless the relinquishment clauses).

On a related matter, we are led to ask how Guyana will dispose of its oil? Who will sell Guyana’s oil? Will this be another closed-door deal or will the government do the responsible thing and hold auctions?