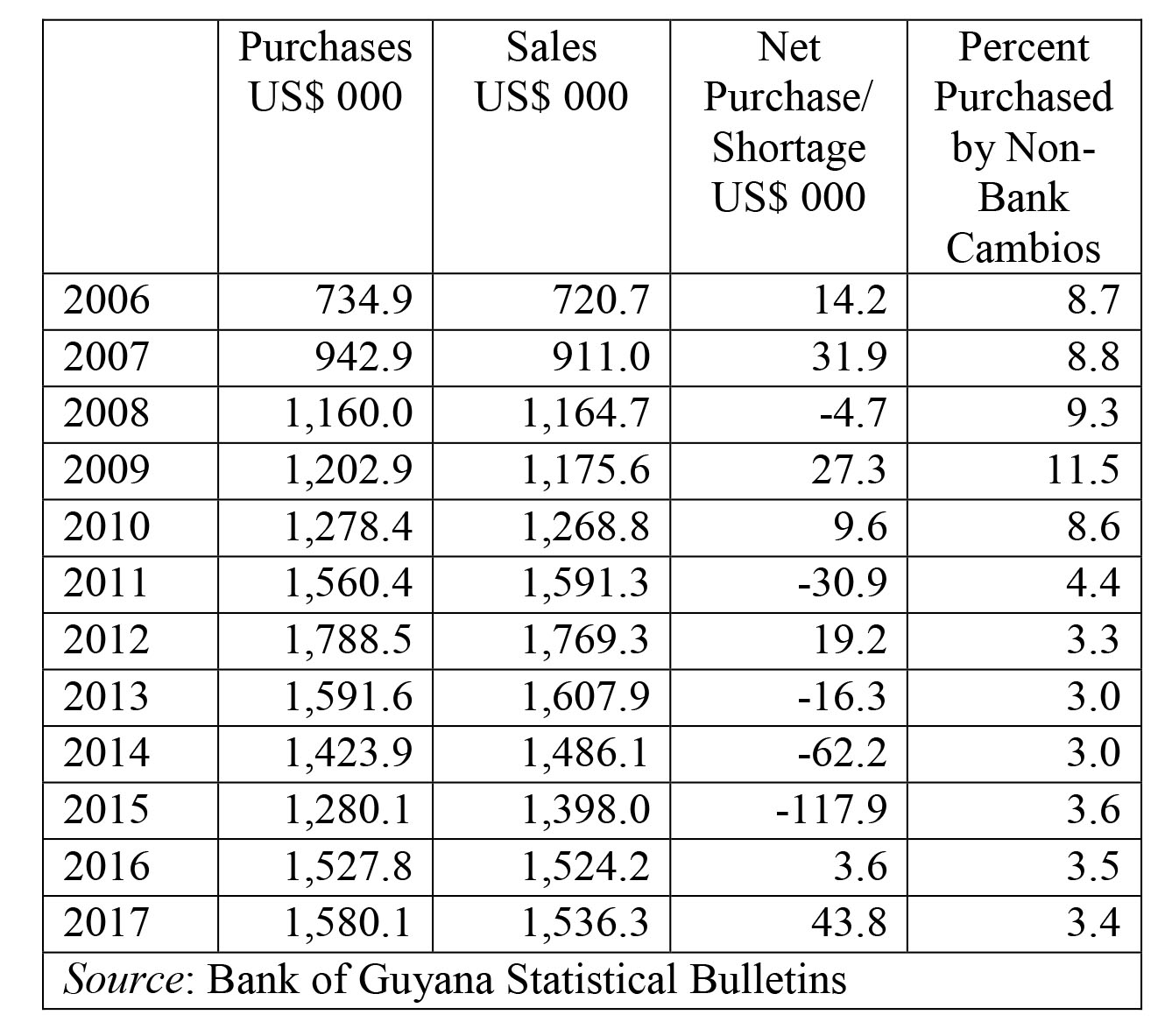

The previous column showed that both the Bank of Guyana and the commercial banks need foreign currency assets. While the central bank’s share of total foreign currency reserves is decreasing as we witness the decline of GuySuCo and other state-owned corporations, the commercial banks are gradually increasing their share. Furthermore, we observed that as the central bank’s share of foreign reserves declines, the Guyana dollar devalues (or depreciates) vis-à-vis the US$. The devaluation has been a gradual instead of the runaway type witnessed from 1988 to 1992. A creeping or gradual devaluation presents businesses the time to adjust their pricing and as a result does not engender the kind of rapid unexpected inflation, although there will be an increase in the cost of living for the vulnerable once prices adjust.

Another important adverse effect of the recent devaluations is the increase in the Guyana dollar value of the external debt. The external debt increases when there are devaluations. However, this to some extent is countered by the fact that the inflation-adjusted value of the domestic debt will decline depending on the inflationary effect of the creeping devaluation. The Guyana dollar amount of the external debt increases immediately and directly when there is a devaluation, creeping or otherwise. On the other hand, the real decline of the domestic debt is indirect since it depends on the inflationary effect of devaluation, a phenomenon known as the exchange rate pass-through to domestic inflation. The last authoritative paper on this topic by Dr Ramesh Ganpat found a strong inflationary effect of devaluation in the case of Guyana.

Another important adverse effect of the recent devaluations is the increase in the Guyana dollar value of the external debt. The external debt increases when there are devaluations. However, this to some extent is countered by the fact that the inflation-adjusted value of the domestic debt will decline depending on the inflationary effect of the creeping devaluation. The Guyana dollar amount of the external debt increases immediately and directly when there is a devaluation, creeping or otherwise. On the other hand, the real decline of the domestic debt is indirect since it depends on the inflationary effect of devaluation, a phenomenon known as the exchange rate pass-through to domestic inflation. The last authoritative paper on this topic by Dr Ramesh Ganpat found a strong inflationary effect of devaluation in the case of Guyana.