Last Thursday marked 50 years since Guyana attained its Independence from Britain. It is only fitting that we reflect on our achievements over this period of time, our collective failures (if any) and the challenges that lay ahead of us as we begin our journey into the second half century of post-Independence. This article attempts to assess how well we performed in terms of public financial management from 1966 to present date.

Position as of 1966

Like the Civil Service, there is no doubt that we inherited from the British a sound financial management system. The relevant sections of the 1966 Constitution dealing with public finance have been extracted from the Financial Administration and Audit Act 1961 which was supported by the Financial Regulations of 1955 and the Stores Regulations of 1953. These include: (a) the establishment of the Consolidated Fund into which all public revenues are to be paid and out of which all expenditures are to be met on the authority of Parliament (b) the establishment of the Contingencies Fund as an emergency fund and the criteria to be used to access and replenish the Fund; (c) the requirements for the preparation of and laying before the National Assembly annual estimates of revenues and expenditures; and (d) the auditing of the public accounts by the Director of Audit (now Auditor General) and reporting to the Legislature within nine months of the close of the fiscal year. These requirements were repeated in the 1980 Constitution.

Like the Civil Service, there is no doubt that we inherited from the British a sound financial management system. The relevant sections of the 1966 Constitution dealing with public finance have been extracted from the Financial Administration and Audit Act 1961 which was supported by the Financial Regulations of 1955 and the Stores Regulations of 1953. These include: (a) the establishment of the Consolidated Fund into which all public revenues are to be paid and out of which all expenditures are to be met on the authority of Parliament (b) the establishment of the Contingencies Fund as an emergency fund and the criteria to be used to access and replenish the Fund; (c) the requirements for the preparation of and laying before the National Assembly annual estimates of revenues and expenditures; and (d) the auditing of the public accounts by the Director of Audit (now Auditor General) and reporting to the Legislature within nine months of the close of the fiscal year. These requirements were repeated in the 1980 Constitution.

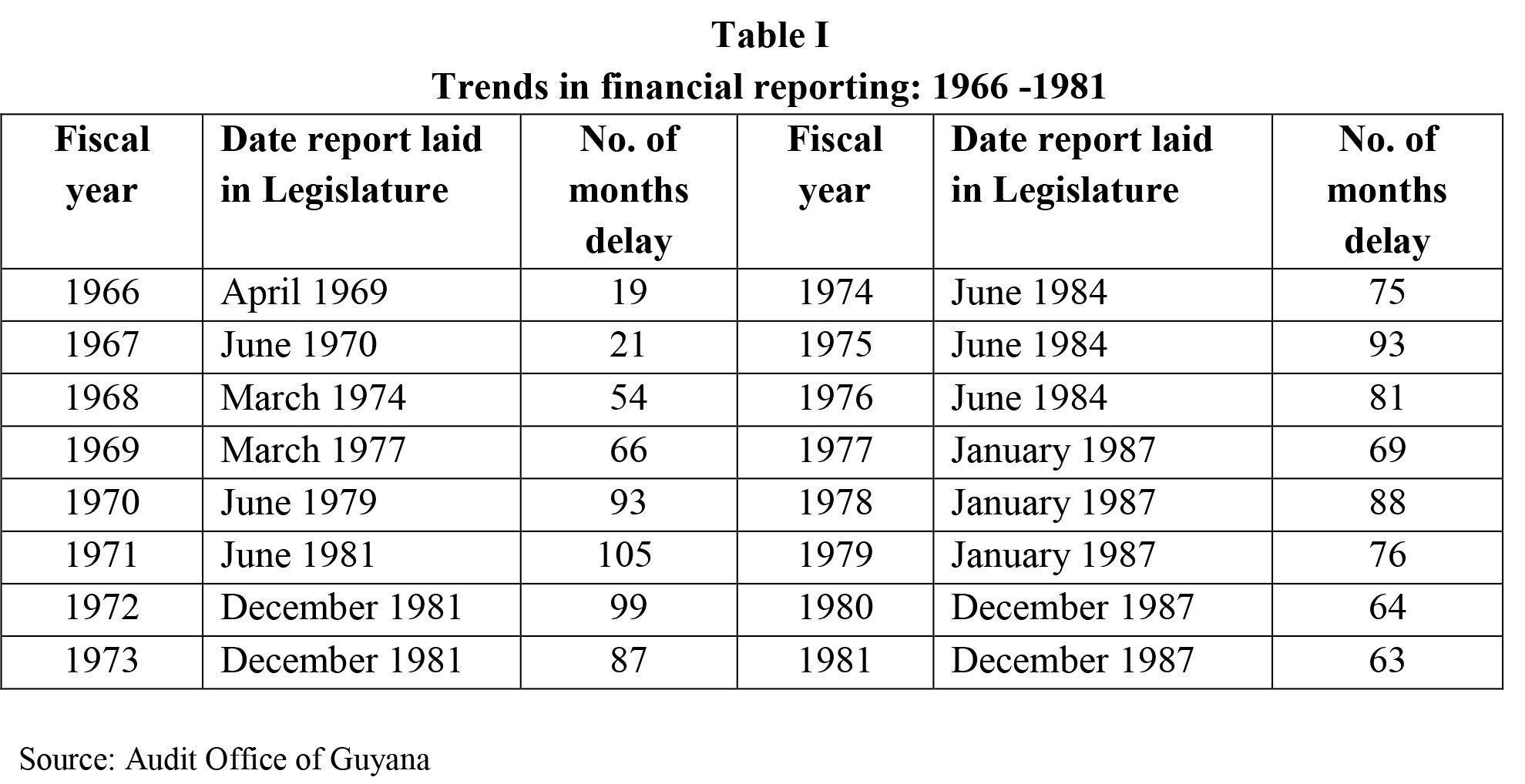

The preparation and audit of the 1965 public accounts were completed and the related report was submitted to the Legislature in May 1967, a delay of eight months. For the period 1954 to 1964, the average delay was six months. However, there were no backlogged public accounts. The only reference I found in