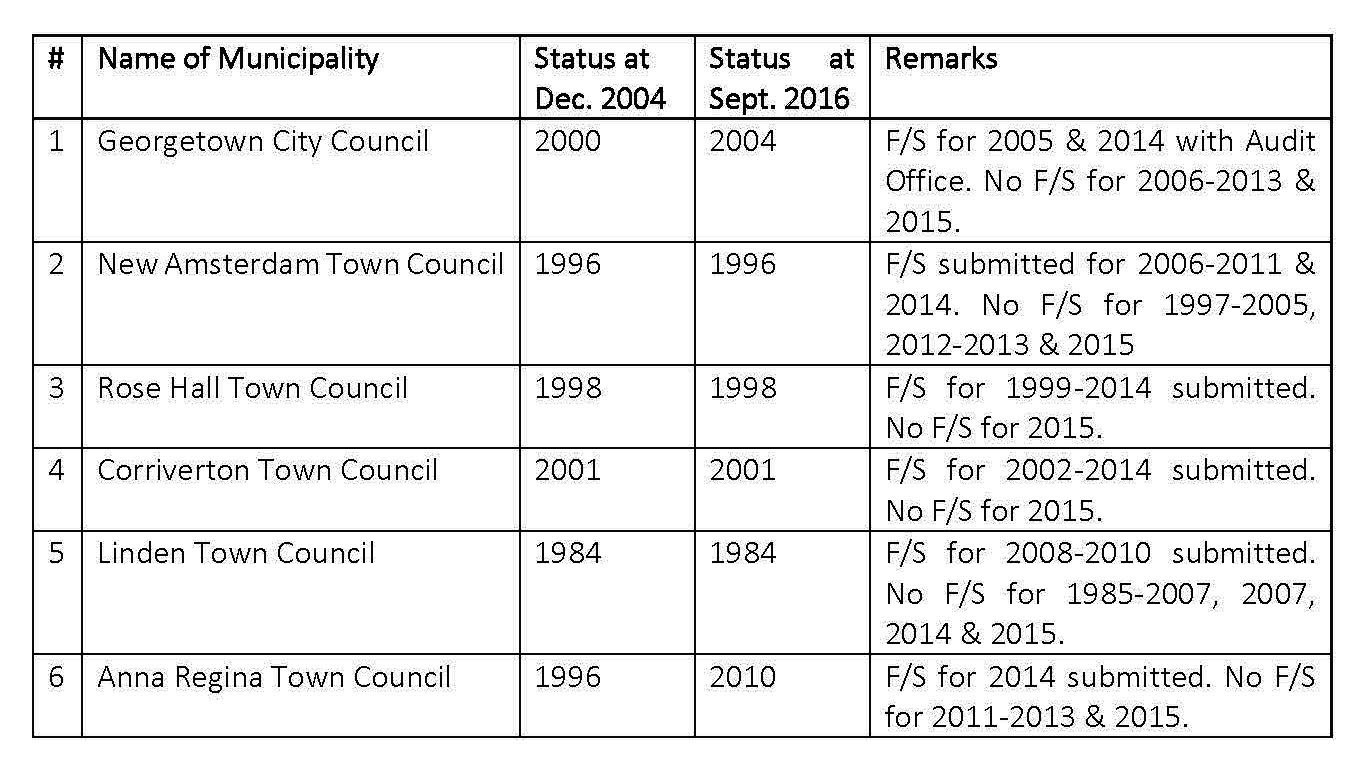

During the course of last week, we learnt that the Georgetown City Council was eleven years in arrears in having their accounts audited and reported on. This is despite the fact that Section 177 of the Municipal and District Councils Act requires all accounts of Municipal and District Councils to be prepared not later than four months after the end of each year and for those accounts to be audited as soon as practicable thereafter. The responsibility for the preparation of the annual financial statements rests with the City Treasurer who shall be guilty of an offence if he/she neglects to do so. The Auditor General is the appointed external auditor of all municipalities.

During the course of last week, we learnt that the Georgetown City Council was eleven years in arrears in having their accounts audited and reported on. This is despite the fact that Section 177 of the Municipal and District Councils Act requires all accounts of Municipal and District Councils to be prepared not later than four months after the end of each year and for those accounts to be audited as soon as practicable thereafter. The responsibility for the preparation of the annual financial statements rests with the City Treasurer who shall be guilty of an offence if he/she neglects to do so. The Auditor General is the appointed external auditor of all municipalities.

The above disclosure was made at the meeting of the Public Accounts Committee (PAC) to discuss the Auditor General’s report for 2015. That report indicated that last set of audited accounts of the City Council was in respect of 2004 and that draft financial statements were received for the years 2005 and 2014, leaving a gap covering the years 2006-2013, not to mention the almost one-year delay in the submission of the 2015 accounts. The Auditor General, however, did not indicate how long the financial statements for the years 2005 and 2014 were with his office and how soon his reports on these statements would be issued.