In our last two columns, we discussed three aspects of the 2017 Auditor General’s report, namely: overall opinion given on the country’s accounts which we felt was not supported by adequate audit evidence; the Executive Summary which did not appear to capture the essence of the report; and the Consolidated Financial Statements of the Government. One statement – Loans and Advances granted by the Government – appeared incomplete since, for example, loans to the Guyana Sugar Corporation and Guyana Power and Light were not included. The report is also badly in need of editing to ensure that findings are presented in concise manner; the report is free of grammatical errors; and technical terms such as “cheque orders” and “inter-departmental warrants” are properly explained or avoided altogether.

In our last two columns, we discussed three aspects of the 2017 Auditor General’s report, namely: overall opinion given on the country’s accounts which we felt was not supported by adequate audit evidence; the Executive Summary which did not appear to capture the essence of the report; and the Consolidated Financial Statements of the Government. One statement – Loans and Advances granted by the Government – appeared incomplete since, for example, loans to the Guyana Sugar Corporation and Guyana Power and Light were not included. The report is also badly in need of editing to ensure that findings are presented in concise manner; the report is free of grammatical errors; and technical terms such as “cheque orders” and “inter-departmental warrants” are properly explained or avoided altogether.

In the Executive Summary, it was stated that there were overpayments totalling $79.738 million to 79 contractors against measured works. However, it is not clear whether any mobilisation advances were deducted before arriving at the overpayments. A mobilisation advance is usually given for large contracts to enable contractors to acquire the necessary machinery and equipment and to mobilise them to the project work sites. The advance is recoverable over the life of the contract by way of deductions from each valuation certificate. Therefore, any attempt to match the value of physical works before they are completed, against payments made, will not give a true reflection of the extent of any overpayment, if any.

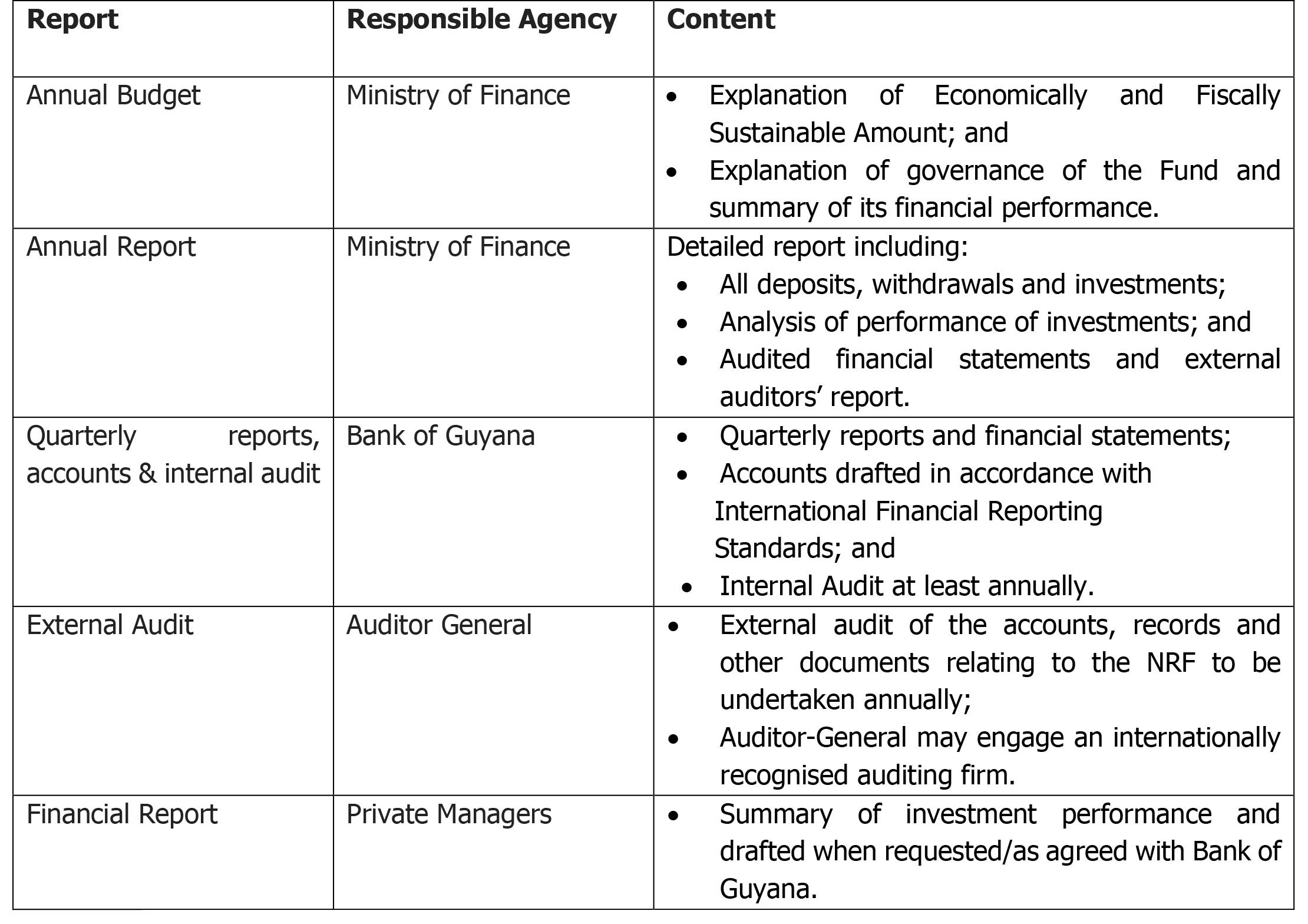

Today’s article discusses the oil revenues expected to flow in 2020; the feature address by the former Prime Minister of Trinidad and Tobago at the recent Guyana Manufacturing and Services Association’s annual presentation award dinner; and the Green Paper on the proposed Natural Resource Fund (NRF). At the time of writing, the Bill for the NRF has been published in the Official Gazette. This will be the subject of our next column.