Introduction

Introduction

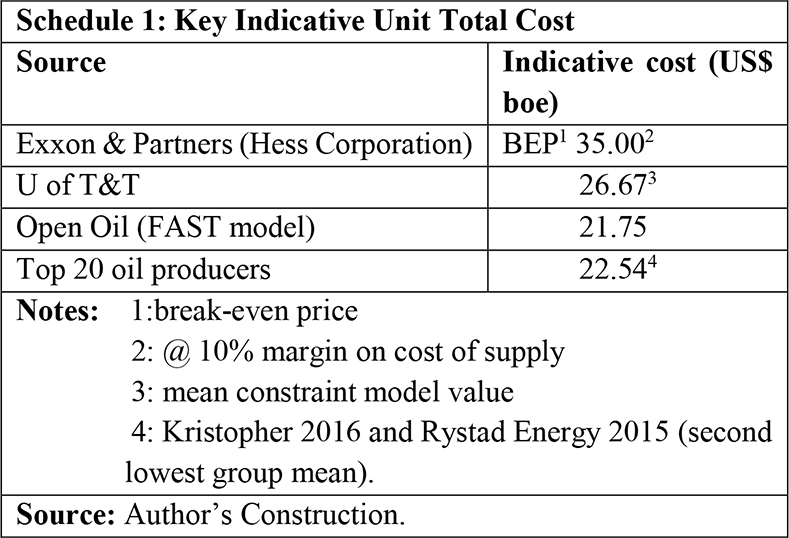

Last week’s column wrapped-up my discussion of break-even prices, both from a business (commercial) perspective and a fiscal and their relation to the unit total cost of Guyana’s crude oil exports. Both break-even prices are determined, bearing unit total cost in mind. However, for the private business calculation of the break-even price, which is market based, this relation is of utmost stringency. For the fiscal break-even price, stringency is there, but far less This is the case because normative considerations dominate because this price is based on what the National Budget determined price the Government thinks “ought to” prevail.

Indeed, it is also for such reasons why, as a rule, the fiscal break-even price substantially exceeds its business (commercial) counterpart.

This week’s column focusses however, on wrapping-up the discussion of Guidepost 6 in Guyana’s Road Petroleum Road Map for its first dimension of “getting petroleum revenues.” Moreover, the column also provides the “indicative unit cost range per barrel of oil equivalent, boe,” that will be used in my projections of Guyana’s likely petroleum revenues, after cost. Next week, in the final column of this dimension, I shall provide a broad summing-up of the major indicators of this dimension before I turn to address the second dimension of the Road Map, namely “spending the petroleum revenues.”