In our last three columns, we discussed the contents of the audit report on Exxon’s post contract costs for 2018-2020. We had stated that we were unsure whether the 55-page document constitutes the full report, and that in the absence of any information to this effect we based our analysis on the document that we have in our possession.

In our last three columns, we discussed the contents of the audit report on Exxon’s post contract costs for 2018-2020. We had stated that we were unsure whether the 55-page document constitutes the full report, and that in the absence of any information to this effect we based our analysis on the document that we have in our possession.

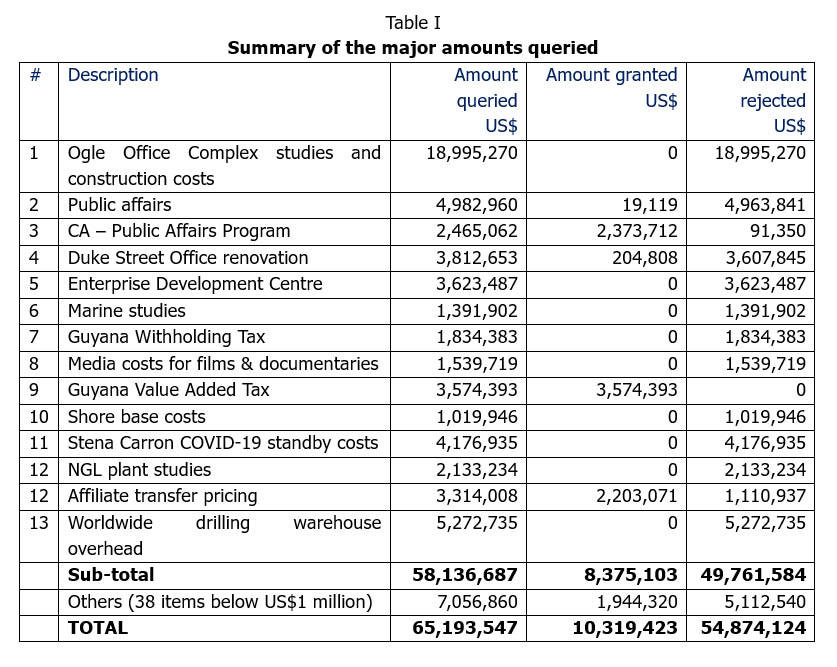

The report is in fact a five-page letter addressed to the Permanent Secretary of the Ministry of Natural Resources, with two appendices covering the rest of the 55 pages. Appendix A, comprising 29 pages, contains eleven items, namely: accounting overview of Exxon’s main subsidiary Esso Exploration and Production (Guyana) Ltd.; drilling and rig overview; labour; allocation methodologies; COVID-19 costs; benchmarking and contracts; capital expenditures (shared costs); taxes; coding; inventory and materials; and Liza FPSO. Also, included in this appendix is an eight-page report on “Stock Verification and Inventory Site Visit”. Appendix B, containing 13 pages, sets out the auditors’ response to 30 sets of questions posed by the Government.