The Transparency Institute (Guyana) Inc. wishes to express its gratitude for being afforded an opportunity to meet with the OAS team on the implementation of the Inter-American Convention Against Corruption. TIGI had submitted in June 2013 its response to the Fourth Round Questionnaire. This presentation draws largely from the response and covers the topic “Civil society perspectives on government oversight bodies that prevent, detect, punish and eradicate corrupt acts.

The Audit Office of Guyana

The Auditor General is required to audit annually the public accounts of Guyana and to submit his reports to the National Assembly. The Constitution defines the public accounts to include: (a) all central and local government bodies and entities; (b) all bodies and entities in which the State has controlling interest; and (c) all projects funded by way of loans or grants by a foreign State or organization. The Auditor General’s mandate is therefore very wide and the task is highly complex technically, professionally and otherwise, requiring the services of a highly trained, skilled, competent and respected person with a proven track record to serve as Auditor General. This is why the Auditor General’s salary, superannuation, benefits and other conditions of service are commensurate with those of the Chief Justice, recently upgraded to those of the Chancellor of the Judiciary. In addition, the Auditor General needs to be supported by a well-resourced, competent, efficient and effective Audit Office.

The Auditor General is required to audit annually the public accounts of Guyana and to submit his reports to the National Assembly. The Constitution defines the public accounts to include: (a) all central and local government bodies and entities; (b) all bodies and entities in which the State has controlling interest; and (c) all projects funded by way of loans or grants by a foreign State or organization. The Auditor General’s mandate is therefore very wide and the task is highly complex technically, professionally and otherwise, requiring the services of a highly trained, skilled, competent and respected person with a proven track record to serve as Auditor General. This is why the Auditor General’s salary, superannuation, benefits and other conditions of service are commensurate with those of the Chief Justice, recently upgraded to those of the Chancellor of the Judiciary. In addition, the Auditor General needs to be supported by a well-resourced, competent, efficient and effective Audit Office.

While the current Auditor General has been making some efforts to discharge his responsibilities, he has his own shortcomings. He is not a professionally qualified accountant although he is required to supervise the work of Chartered Accountants in public practice contracted by him. In addition, unlike several other countries, there are many State-owned/controlled companies, statutory bodies and public corporations for which the Auditor General has audit responsibility. However, the Companies Act requires the auditors of companies to be issued with practising certificates from the Institute of Chartered Accountants of Guyana before undertaking the audits of companies. Since he is not a professionally qualified accountant, the Auditor General is not is possession of such a certificate. Regrettably, neither the Constitution nor the Audit Act 2004 specifies qualification requirements for appointment as Auditor General.

The effect of not having a suitably qualified person to serve as Auditor General is the inability to attract and retain suitably qualified and trained persons to serve under him or her. This would therefore have an adverse effect on the quality of the work undertaken and the reports issued. To a large extent, this is true of the Guyana Audit Office, as many of the findings are routine findings resembling those of internal audit. Several significant issues of national importance are given superficial treatment or are avoided in their entirety.

TIGI recommends that the Audit Act be amended to include qualification requirements for appointment as Auditor General. The person to be appointed should possess at least a professional accounting qualification such as the ACCA (UK), CPA (USA), CGA (Canada). He or she must also have appropriate experience in an external audit environment at a very senior level, preferably at the level of a partner of a reputable chartered accounting firm. Alternatively, in addition to having an advanced degree in one of the related disciplines – accounting, finance, economic and public management – the person should be an expert in public finance and administration. In both situations, it would be imperative for the Audit Office to be staffed with professionally qualified accountants at the senior management level.

The Constitution states that there shall be an Auditor General for Guyana. We interpret this requirement to mean that the holder of this office must be a substantive appointee, and that any acting arrangement should be for a short period not exceeding six months usually to allow time for the proper selection as a replacement to the previous holder. This requirement is to preserve the independence of the Auditor General which is one of the fundamental concepts in auditing. Any prolonged acting arrangement is likely to put pressure on the Auditor General to be as critical as he/she would like to be of the operations of the Government since he/she is dependent on the Government for a continuation of the acting arrangement and possibly to be appointed substantively at some future point in time. Prior to his substantive appointment last year, the Auditor General acted in the position for eight years. It was only when it was pointed out publicly that he was about to attain retirement age in his substantive position and would therefore have to demit office that he was substantively appointed, thereby extending his tenure by another ten years. We view this as an unfortunate occurrence.

TIGI recommends that the Audit Act 2004 be amended to make it a requirement that in the event of the position of Auditor General being vacant, any acting arrangement should not exceed six months.

The Audit Act provides for the appointment of the Auditor General by the President based on a recommendation by the Public Service Commission (PSC). This is an anomaly since the PSC no longer has jurisdiction over the Audit Office in terms of appointment of staff members of the Audit Office. Since the Auditor General serves the Legislature, the latter should have a say in the appointment of an Auditor General. This is necessary to ensure that the person so appointed enjoys the confidence of the Legislature.

TIGI recommends that all future appointments of the Auditor General be based on a recommendation from the Public Accounts Committee (PAC). In this regard, the Committee could propose three candidates from which the President makes a selection, subject to ratification by two-thirds of the membership of the National Assembly.

There is only one professionally qualified accountant among the staff members of the Audit Office and there is no evidence that efforts were made over the years to recruit qualified accountants for the Office. Persons are promoted based on years of service and completion of internal training and external training at the technician level, and to a certain extent participation in fellowship programmes through the generosity of mainly the Canadian and Indian National Audit Offices. But these are no substitute from formal academic and professional qualifications, as provided for in the job specifications.

There was an unfortunate incident recently where the Auditor General sought to have the PAC ratify the appointments of 11 senior officers, most of whom did not meet the job specifications. The PAC was divided on the matter, with the members of the Opposition not in favour of the appointment of

persons who did not satisfy the job requirements. On the day the PAC was in session, the Government side, observing that a member from the Opposition was absent, called for a vote on the matter. The vote was carried since the Government side had the majority.

TIGI recommends that whenever a vacancy arises in the Audit Office, appointments should be based on public advertisement, short-listing of candidates, and assessments based on interviews and other means before the selection is made.

The Minister of Finance is responsible for preparing, certifying and submitting the public accounts of Guyana to the Auditor General for audit. His wife is, however, the only professionally qualified accountant in the Audit Office and holds the position of Audit Director which is the next level position below the Auditor General. Given that the Auditor General is not a professionally qualified accountant, the general view is that wife of the Minister is the de facto head of the Audit Office. In addition, she has overall responsibility for the audit of public enterprises of which the National Industrial and Commercial Industries Ltd (NICIL) is one such entity. The Minister of Finance is the Chairman of NICIL. The operations of NICIL are shrouded in controversy involving the vesting of State properties and other assets, their disposal and the retention of the proceeds to meet expenditure in complete violation of Articles 216 and 217 of the Constitution. We view this situation as a serious conflict of interest.

TIGI recommends that the Auditor General, in collaboration with the Government, take appropriate measures to remove the conflict of interest that has been existing in the Audit Office since the appointment of the Minister of Finance in 2006. This could be done by re-assigning the Minister to another ministerial portfolio, or if this is not considered desirable, having the concerned officer relocated to another State-owned/controlled entity.

Once appointed, the Auditor General serves until the age of retirement, which is 65. The first local Auditor General served for 21 years while the second served for 15 years. The current Auditor General, upon attaining retirement age would have served for 17 years. Many countries have considered it necessary to introduce fixed term appointments. For example, South African Auditor General serves for seven years while in Canada, the Auditor General demits office after ten years. India has a five-year term limit while for the United Nations Board of Auditors the term limit is six years. This practice enhances the independence of the Office and allows for the incumbent to give of his/her best and possibly to leave a lasting legacy for someone else to continue. Experience has shown that lengthy appointments only serve to stagnate the Office.

TIGI recommends that the relevant legislation be amended to limit the term of office of the Auditor General to ten years with the proviso that current Auditor General be given the option to retire on completion of this period of service, given that he is not a professionally qualified accountant.

The Public Accounts Committee

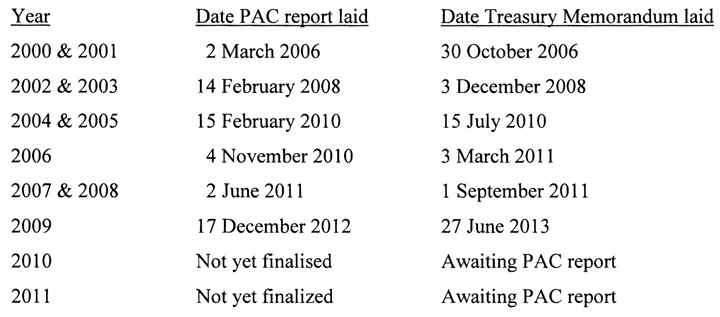

The PAC’s main function is “to examine the accounts showing the appropriations of sums granted by the Assembly to meet Public Expenditure and such other accounts laid before the Assembly as the Assembly may refer to the Committee together with the Auditor General’s report thereon”. In conducting its examination, the PAC invites accounting officers and other officials to provide the necessary explanations and clarifications. At the end of its examination, the PAC issues a report to the National Assembly which usually adopts it. The report is then referred to the Government for a response in the form of a Treasury Memorandum setting out what actions have been taken or proposed to be taken in relation to the findings and recommendations of the PAC. In the past, the PAC has been slothful is discharging this responsibility, though the situation has somewhat improved with its reconstitution following the 28 November 2011 National Elections. The following table shows the trend in finalizing and presenting of the PAC’s reports in the National Assembly as well as the Government’s response:

Ideally, the accountability cycle, culminating in the issuance of the Treasury Memorandum, should be completed in a manner to facilitate the budget process. In reviewing the budget for a particular fiscal year, and for a more meaningful process to take place, legislators should benefit from the results of the audit of the previous fiscal year, including the completion of the PAC examination and the issuance of the Treasury Memorandum. For this to happen, the accountability cycle needs to be revised. For example, given the rapid advances in information technology, there is no valid reason why financial statements cannot be submitted earlier to enable the Auditor General to issue its report within six months of the close of the financial year. This will facilitate the PAC’s examination of the public accounts in early July, its reporting by September, and the issuance of the Treasury memorandum by October. The budget process for the next fiscal year could then begin in November, and by 31 December the budget is approved.

Ideally, the accountability cycle, culminating in the issuance of the Treasury Memorandum, should be completed in a manner to facilitate the budget process. In reviewing the budget for a particular fiscal year, and for a more meaningful process to take place, legislators should benefit from the results of the audit of the previous fiscal year, including the completion of the PAC examination and the issuance of the Treasury Memorandum. For this to happen, the accountability cycle needs to be revised. For example, given the rapid advances in information technology, there is no valid reason why financial statements cannot be submitted earlier to enable the Auditor General to issue its report within six months of the close of the financial year. This will facilitate the PAC’s examination of the public accounts in early July, its reporting by September, and the issuance of the Treasury memorandum by October. The budget process for the next fiscal year could then begin in November, and by 31 December the budget is approved.

TIGI recommends that consideration be given to revising the timetable for the various activities, from budget preparation and approval to the issuance of the Treasury Memorandum, to facilitate the National Assembly’s more informed consideration of the National Estimates and approval before the fiscal year begins.

The PAC has been focusing on the Auditor General’s report as the basis for its examination, almost to the exclusion of the public accounts. As indicated above, given the staffing situation in the Audit Office, many significant issues of national importance are not reflected in the Auditor General’s report, or are treated superficially without any detailed analysis and review.

Mention was also made of what constitutes the public accounts but the PAC examination is restricted to the results of the audit of central government activities. There is no evidence that the audited accounts of statutory bodies, public enterprises and other entities in which controlling interest vests with the State are referred to the PAC after they have been tabled in the National Assembly.

TIGI recommends that that the PAC’s examination of the public accounts be extended to include all statutory bodies, public enterprises and other bodies in which controlling interest vests with the State.

(See tomorrow’s edition for another instalment of the presentation.)