Last Thursday marked 50 years since Guyana attained its Independence from Britain. It is only fitting that we reflect on our achievements over this period of time, our collective failures (if any) and the challenges that lay ahead of us as we begin our journey into the second half century of post-Independence. This article attempts to assess how well we performed in terms of public financial management from 1966 to present date.

Position as of 1966

Like the Civil Service, there is no doubt that we inherited from the British a sound financial management system. The relevant sections of the 1966 Constitution dealing with public finance have been extracted from the Financial Administration and Audit Act 1961 which was supported by the Financial Regulations of 1955 and the Stores Regulations of 1953. These include: (a) the establishment of the Consolidated Fund into which all public revenues are to be paid and out of which all expenditures are to be met on the authority of Parliament (b) the establishment of the Contingencies Fund as an emergency fund and the criteria to be used to access and replenish the Fund; (c) the requirements for the preparation of and laying before the National Assembly annual estimates of revenues and expenditures; and (d) the auditing of the public accounts by the Director of Audit (now Auditor General) and reporting to the Legislature within nine months of the close of the fiscal year. These requirements were repeated in the 1980 Constitution.

Like the Civil Service, there is no doubt that we inherited from the British a sound financial management system. The relevant sections of the 1966 Constitution dealing with public finance have been extracted from the Financial Administration and Audit Act 1961 which was supported by the Financial Regulations of 1955 and the Stores Regulations of 1953. These include: (a) the establishment of the Consolidated Fund into which all public revenues are to be paid and out of which all expenditures are to be met on the authority of Parliament (b) the establishment of the Contingencies Fund as an emergency fund and the criteria to be used to access and replenish the Fund; (c) the requirements for the preparation of and laying before the National Assembly annual estimates of revenues and expenditures; and (d) the auditing of the public accounts by the Director of Audit (now Auditor General) and reporting to the Legislature within nine months of the close of the fiscal year. These requirements were repeated in the 1980 Constitution.

The preparation and audit of the 1965 public accounts were completed and the related report was submitted to the Legislature in May 1967, a delay of eight months. For the period 1954 to 1964, the average delay was six months. However, there were no backlogged public accounts. The only reference I found in relation to the audit of these accounts around this time was from Ambassador Odeen Ishmael’s publication entitled “From Autocracy to Democracy in Guyana. Aspects of Post-Independence Guyanese History 1966-1992” in which the following statement was made:

In 1966, Peter D’Aguiar, the UF leader and Minister of Finance, charged that he was not being adequately consulted by PNC leader and Prime Minister Forbes Burnham, particularly on government expenditures. Early in 1967, he accused the PNC section of the government with spending $1.5 million

illegally on building the East Coast Demerara road, declaring that the Director of Audit had questioned the expenditure.

The Director of Audit at the time was one Mr. Dunlop, a British national. In 1969, he was replaced by our first local Auditor General, the late Patrick Farnum, who relinquished his position of Accountant General to take up the new offer.

Trends in financial reporting and audit: 1966-1981

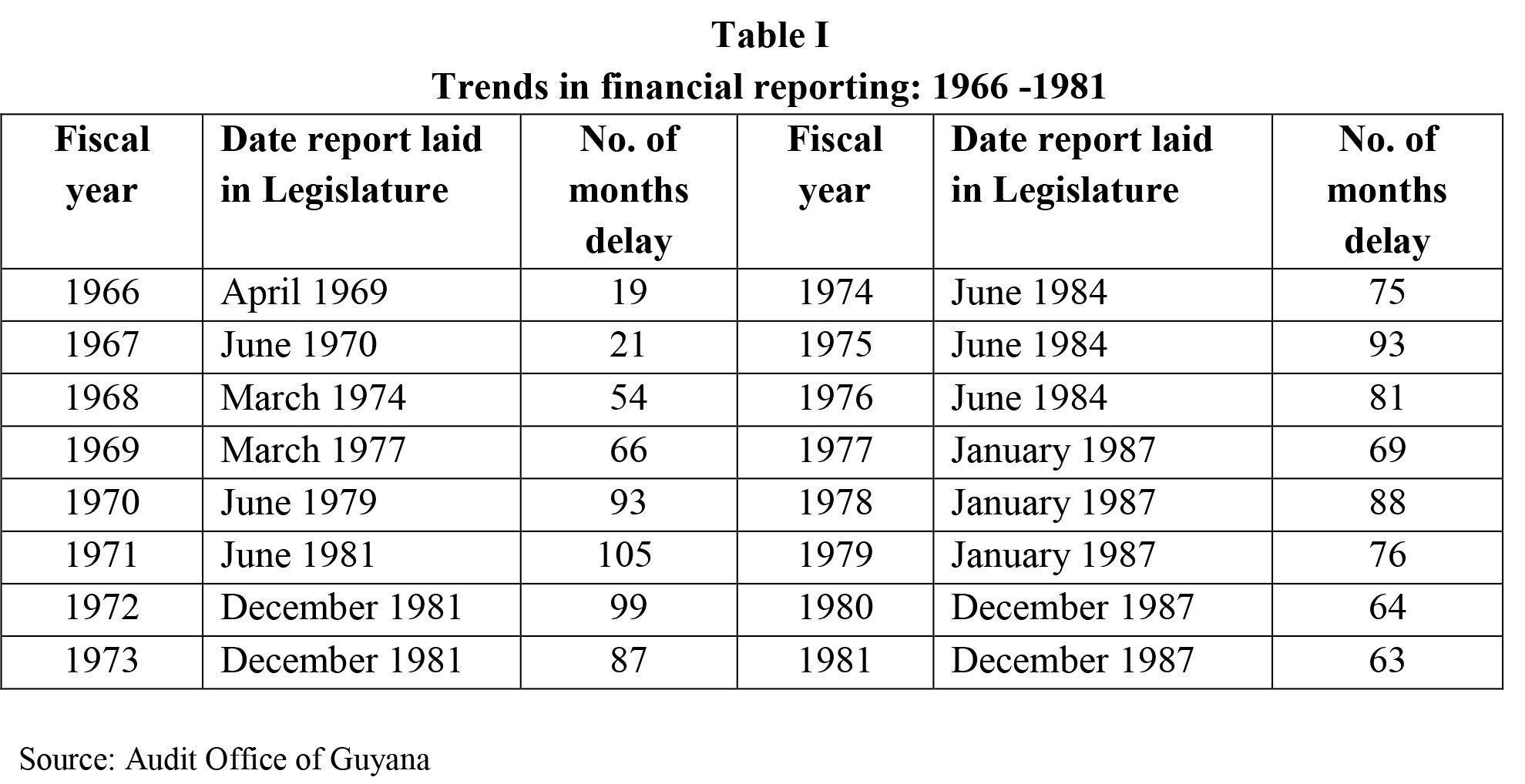

Experience has shown that undue delays in having audited accounts of an organization are an indicator that all is not well with its financial management practices and, more importantly, are symptomatic of a more fundamental problem. In relation to the public accounts, the average delay was six months during the pre-Independence period 1953 to 1965. However, for the years 1966 to 1981, such delays were in the order of on average six years, as shown at Table I:

As can be noted, the greatest delay was in respect of the year 1971 when the accounts were not finalized and presented to the National Assembly until June 1981, almost nine years later. To compound matters, a number years were reported together: 1972 to 1973; 1974 to 1976; 1977 to 1979 and 1980 to 1981. It soon became clear that the inevitable was likely to happen. Public accountability was brought to a standstill with effect from in 1981. Explanations obtained indicated that the main frame IBM System 3/15 mainframe computer at the Ministry of Finance had “crashed”, resulting in the Government’s inability to produce the public accounts for subsequent years.

The Hoyte Administration had inherited seven years of the backlogged accounts covering the period 1977 to 1983. To its credit, it was able to produce audited public accounts for first five of these years in 1987, albeit in combined form.

Restoration of public accountability

In late 1990, the newly appointed Auditor General, yours truly, drew the attention of the Minister of Finance, the Accountant General and the concerned senior officials about the requirements of the law relating to financial reporting of the Government and the fact that the said law was honoured in the breach for eight years. The Accountant General was adamant that computer problems prevented him from finalizing the public accounts for not only the backlogged years 1982 to 1989 but also the year in question – 1990. On the other hand, Accounting Officers contended that it was the responsibility of the Ministry of Finance to process transactions relating to their Ministries and Departments and to submit periodic print-outs for reconciliation with their records. Because of the absence of such print-outs, these officials claimed that they could not effect the necessary reconciliations and therefore could not prepare their appropriation accounts and submit them for audit! It soon became clear that political intervention was needed to redress the situation and to break the impasse. However, any such intervention had to await the outcome of the 1992 elections.

The Audit Office had conducted preliminary audits of Ministries and Departments and had held its findings in abeyance pending the submission of financial statements. The Auditor General took the view that in the absence of financial statements, the results of the preliminary audits should be presented to the Legislature. The Government vigorously opposed this view, prompting the Auditor General to seek a legal opinion from the Attorney General on the matter, which opinion supported his view. As a result, the Auditor General issued preliminary reports to the National Assembly for the years 1982-1985. He also wrote to the Minister in late 1991 outlining the problems associated with the Government’s financial management and making a number of recommendations, including a proposal for a two-pronged approach to restart financial reporting, with 1991 as the cut-off year. The key recommendations were:

- The closure of all government bank accounts and the opening of new ones with effect from 1992 to avoid any contamination from the backlogged years;

- Instituting proper systems and procedures to ensure accurate recordkeeping and reconciliation, and to facilitate timely, reliable, and accurate financial reporting for the future, commencing 1992; and

- The setting up of a task force to deal with the backlogged accounts covering the period 1982 to 1991. The Accountant General had estimated it would take approximately six months for each of the backlogged years to be finalized. In other words, it would have taken until 1997 to bring the backlogged accounts up-to-date, by which time the current year’s accounts would have gone backlogged by five years, hence the recommendation of a two-pronged approach.

Although the Minister accepted these recommendations, they were not implemented despite strenuous efforts by the Audit Office to influence the Ministry of Finance to do so.

In late 1992, the Auditor General renewed his representations to the new Minister and met with the Head of the Presidential Secretariat (HPS) and the Accountant General to present his arguments in favour of a resumption of annual financial reporting based on the two-pronged approach he had advocated. The Accountant General contended that it was unprecedented to have a gap in financial reporting and that any attempt to do so would result in inaccurate reporting. The HPS enquired about the level of accuracy that could be achieved if the recommendations of the Auditor General were to be followed. The Accountant General indicated that such accuracy would be in the vicinity of 60 to 70 percent to which the HPS responded: Would a 60-70 per cent level of accuracy not be better than no financial reporting?

In February 1993, the Government issued instructions to the Accountant General and accounting officers to comply with the requirements of the law relating to annual financial reporting of the public accounts. As a result, financial statements for the fiscal year 1992 were submitted for audit examination. However, such submissions were not without their fair share of resistance and lack of cooperation from those responsible for preparing the accounts. As was expected, the accounts were somewhat incomplete in that of the 12 consolidated statements comprising the public accounts, two were not submitted. However, individual statements of revenues and expenditures of all Ministries and Departments, which numbered approximately 200, were submitted. The Audit Office completed the audit of these statements and accounts, and the Auditor General presented his report to the Minister on 14 September 1993 for laying in the Assembly, thereby bringing to an end ten years of absence in financial reporting at the national level. It was a hard-fought victory for the restoration of public accountability. Since then, there has been annual financial reporting and audit, and laying of the related reports in the Assembly.

In relation to the backlogged accounts for the years 1982-1991, a task force was set up to compile the financial statements. However, little progress was made and the effort had to be abandoned, resulting in a significant blemish in the history of public accountability in Guyana.