When an individual wants to buy or sell a stock, they must communicate certain information to a broker. The broker must be given the following information:-

● What issue the customer would like to buy or sell;

● The number of shares the customer would like to buy or sell; and

● The price at which the customer would like to buy or sell.

There are a number of ways of expressing how an order is to be regarded and also the amount of time the broker has to execute the order. Here are the major types of orders.

Market order: A market order is the simplest of all orders, which is basically an instruction to purchase or sell stock at the market price. For example, let us assume that the market price of EEB1S stock is GY$26.51 and you place a market order for the purchase of 1,000 shares of EEBIS stock. This means that you would have to pay GY$26,510 (plus commission to your broker) for the shares. Market orders are easiest to be filled because the broker just buys the stock when they are available regardless of the price. Here the broker executes the order immediately at the best possible price.

Limit order: means that you would buy or sell shares up to a certain limit or price. For example, given the same current market price, you would instruct your broker to sell your 1,000 shares of EEBIS stock at $27.00. Notice that a limit sell order would be higher than the market price, and, conversely, a limit buy order would be lower than the market price. This means that when the price of EEBIS reaches GY$27.00, then your broker would sell your shares.

If the price does not reach GY$27.00, then your transaction will not be executed. What it does is specify the minimum price at which to sell or the maximum price to buy. That is, it says to the broker, buy only if you can buy for no more than $X, or sell, but only if you can sell for at least $Y.

Good for the day. Good for the day means that if you placed an order with your broker, if the order is not filled up to the end of the trading day, your order is cancelled.

A good until cancelled order means that if your order is not filled today, you will keep that order open to the next trading day and every succeeding trading day until it is filled or until you instruct the broker to cancel the order.

TYPES OF FIXED-INCOME SECURITIES AND THEIR CHARACTERISTICS

Fixed-income securities are usually debt instruments. However, not all debt instruments are fixed-income. We will first start off by a brief discussion of the various features of fixed-income securities and the provisions for paying off bonds.

The market for corporate debt instruments in the Caribbean is not well developed, except for the market in Trinidad and Tobago. Because of this, we will have to rely on the examples from elsewhere.

First of all, corporate debt instruments are financial obligations of a corporation that have a priority over the claims of preferred and common stockholders in the case of bankruptcy. Corporate securities can be either publicly or privately placed. The advantage of debt is that it has seniority of claims over all other claimants to the firm’s assets. Even among debt holders, there are those that have priority of claims over other debt holders (i.e. those holding senior debt over junior debt holders).

BONDS

Sample bonds issued in Trinidad and Tobago

Debt is not an ownership interest in the firm and creditors usually do not have voting power.

Interest on bonds is deductible for tax purposes. The written agreement between the corporation (borrower) and its creditors is called an indenture. The indenture contains basic terms of the bond (coupon, principal amount, repayment times, etc.), a description of any property used as collateral, any call -provisions and protective covenants.

A Bond Certificate

MATURITY

The term to maturity of a bond is the number of years over which the issuer has promised to meet the conditions of the obligations. The maturity date of a bond refers to the date that the debt will cease to exist, at which time the issuer will redeem the bond by paying the amount borrowed. The maturity or term of the bond can be divided into different terms such as; short-term is 1 to 5 years, intermediate-term is 5 to 12 years, and long-term more than 12 years. There are three key reasons why the term to maturity of a bond is important:

Term to maturity indicates the time period over which the bondholder can expect

to receive interest payments and the number of years before the principal will be

paid in full.

The yield offered on a bond depends on the term to maturity,

The price of a bond will fluctuate over its life as interest rates in the market

change.

PAR VALUE

The par value of a bond has many other names, such as; principal, face value, redemption value and maturity value. All these terms connote the amount that the issuer agrees to repay the bondholder by the maturity date. There is no law that says that par values need to be identical. As such, you can have different par values, e.g. GY$1,000, GY$5,000, GY$100,000. This is why there is the practice to quote the price as a percentage of its par value. For example, a bond with par value of GY$1,000 selling for GYS900 would be a bond that is said to be selling at 90. In order to compute the price of a bond given the quote of selling at 90, one should first compute the price of the bond per dollar value of par value. In this case, it is GY$0.90, then we multiply this number to the par value, say GY$5,000, we have the price of the bond as GY$4,500. When the price of the bond trades below its par value, it is said to be trading at a discount. Conversely, if the bond is trading above its par value, it is said to be trading at a premium.

In the most basic sense, the coupon rate is the rate of interest that the issuer agrees to pay each year. The annual amount of the interest payment made to bondholders during the term of the bond is called the coupon. The coupon is computed by multiplying the coupon rate by the par value of the bond. For example, if we have a 10% coupon rate and a par value of GY$1,000, the annual interest is $100. However, not all bonds pay coupons. There are bonds that do not pay any coupons during its entire life, and these are called zero coupon bonds. The interest that is paid by the borrower is the difference between the par value and the price paid.

Some bonds do not pay coupons for a certain number of periods but start paying coupons after a specific date. These bonds are called deferred coupon bonds. They initially behave like zero coupon bonds for a certain number of years and up to a specific term, they then become a normal coupon-paying bond until maturity.

In a volatile interest rate environment, offering fixed interest rates may not seem attractive to bondholders. Thus, bonds are commonly issued as variable rates and these instruments are called floating-rate securities. The interest rate that will be paid is based on a typical formula that is reset periodically according to some reference rate.

DENOMINATION

Typically, bonds are denominated in the local currency but can also be issued in a foreign currency .Some bonds carry conversion privileges. A convertible bond allows the bondholder to exchange the bond for common shares of the firm. An exchangeable bond allows the bondholder to exchange the bond for shares of a different firm from the issuer.

Some bonds also carry what are called put provisions. Basically, a put provision gives the bondholder the right to sell the issue back to the borrower at a specified price on designated dates. The price that will be paid by the issuer is called the put price. Thus, when the market rates increase above the issue’s coupon rate, the bondholder can sell the bond at the put price and reinvest the proceeds at the prevailing higher rate.

RISKS ASSOCIATED WITH INVESTING IN BONDS

In a general sense, investing in bonds is less risky than investing in stocks because interest as principal payments are contractual obligations of the borrower and there is seniority of claims on the assets of the firm. However, there are still risks that are assoc-iated with investing in bonds that cannot be overlooked Some of these risks result from the different features of the bonds in question. 1) Interest Rate Risk.

The biggest risk that a bondholder faces is interest rate risk. Interest rate risk is the risk that the price of the bond will decline due to an increase in interest rates. There is an inverse relationship between the price of the bond and the yield that is required by the market. When the coupon rate is equal to the market yield, the bond trades at par. If the yield required on the bond increases, the price of that bond would decline. For example, if you bought a 10% coupon bond at par (i.e. its yield is 10%) and the yield increases to 12% in six months, the price of that bond in the market would be selling at a discount. This is because, no one would take in a 10% coupon at par if he/she would be

able to get 12% elsewhere for the same risk. As such, since the coupon rate of 10% cannot be changed, the price of the bond would have to be adjusted to reflect this increase in yield.

The different features of a bond affect interest rate risk in different ways. For example, the longer the maturity of a bond, the greater the bond’s sensitivity to changes in interest rates.

The lower the coupon rate on a bond, the higher its sensitivity to interest rate changes. This is because you receive a lower present value today and the higher the interest rate in the future the lower the present value of the cash flows that you would expect to receive.

2) Exchange Rate or Currency Risk

When you hold a bond denominated in a different currency, you are exposed to exchange rate risk. This is because there is a possibility that due to exchange rate fluctuations, the value of the coupon and maturity value that you will receive is less than what you initially planned.

For example, if you hold a US dollar bond and the Guyana dollar continuously appreciates, then the value of the dollar coupons and face value that you will receive would be less than what you expected.

3) Event Risk

There are certain scenarios that make it difficult for firms to repay their debt obligations. Some of these are:

● Corporate Takeover

● Natural disasters

● Political Risk

● Regulatory Risk

● Restructurings

● Technological advances

4)Default Risk

Default risk is the risk that borrowers fail to make all the promised payments. Technical default can occur if the issuer violates any of the debt covenants (contractual agreements) of the bond. Rating agencies (CariCris, Standard & Poor’s (S&P), Moody’s) rate the default risk of bonds. The highest rated bonds are called investment grade. Bonds rated below investment grade are called junk bonds.

When a corporation issues corporate debt, it can either be secured or unsecured. In the case of secured debt, that is an instrument which is collateralized with real or personal property. When the borrower defaults on his obligations, the property is foreclosed in favour of the lender. A form of secured debt is a mortgage on a house, where the default of the borrower would result in the foreclosure on the house that is pledged under the agreement. Typically, lenders only accept first mortgages, which are properties that have not been mortgaged elsewhere. This is because it is possible to borrow even a small amount and use a big property as collateral. For unsecured debt or what is called a debenture, there is no collateral that is pledged. These types of loans are usually done based on the character of the individual. Sometimes, this becomes very costly for the lender.

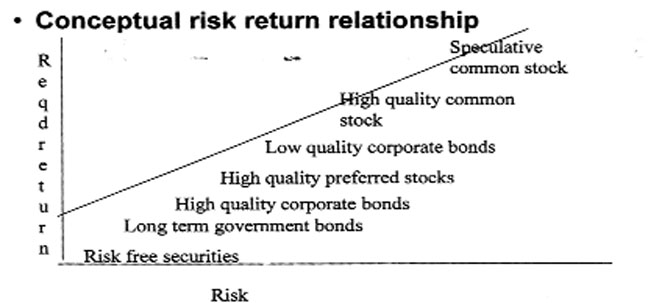

Risks and required returns for various types of \securities

EQUITY STYLES

There are four types of equity styles: 1) value, 2) growth, 3) market-oriented, and 4) small capitalization. Consider this scenario where you have two investors who are evaluating the same P/E ratio from two opposing perspectives. The “growth” investor is primarily concerned with the earnings component of the ratio, and is concerned with if that future growth does not occur as expected. On the other hand, the “value” investor is concerned primarily with the price component of the ratio and cares much less about future earnings growth of the company. These two investors look at the same stock and at the same indicator, but from different perspectives. Thus, they purchase the stock at different points along the P/E curve, both of which has potential for earnings as long as the stock follows their desired pattern.