Constant trade deficit

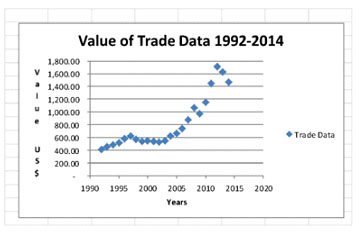

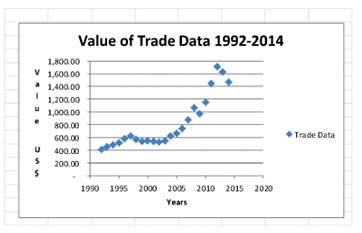

Guyana, like several other countries, runs a constant trade deficit. The simple reason is that Guyana imports more than it exports. From the Chart below, it could be seen that the value of trade has grown fourfold from 1992 to 2014. The deficit however has grown even faster tenfold during the same period. The imbalance in trade gives rise to the need for the country to make up the difference between the revenue it receives for its exports and the payments that it must make for its imports. Guyana also experiences a deficit in the services that are linked to international trade. Data on these trade and service transactions is found in the Balance-of-Payments (BOP) report of the country and is usually described as the current account balance. In addition to the current account, the BOP also has a capital and financial account section. Made up primarily of financial flows in capital and investing transactions, the BOP helps to identify and explain how the trade gap is financed. This article seeks to highlight some trends in international financial flows to Guyana that are used in financing the trade deficit.

Terms-of-Trade

![]() Invariably financial flows start with trade. The need (or greater preference in some cases) for foreign goods creates a gap in financing that has to be closed. The trade deficit has grown substantially from 1992 to 2014. It expanded tenfold from US$61 million to US$611 million. The imbalance does not come only from buying more than Guyana sells. The gap can also arise from unfavourable terms of trade. This means that the price of imports has been consistently higher than the price of exports. Looking back over the last 23 years, Guyana continued to run a trade deficit as it has done for the years for which statistics can be observed.

Invariably financial flows start with trade. The need (or greater preference in some cases) for foreign goods creates a gap in financing that has to be closed. The trade deficit has grown substantially from 1992 to 2014. It expanded tenfold from US$61 million to US$611 million. The imbalance does not come only from buying more than Guyana sells. The gap can also arise from unfavourable terms of trade. This means that the price of imports has been consistently higher than the price of exports. Looking back over the last 23 years, Guyana continued to run a trade deficit as it has done for the years for which statistics can be observed.

Without a detailed analysis, it is not easy to say which of the two factors has had a greater impact on the deficit. But in looking at the unit value of the major commodities that Guyana exports, it has behaved in typical manner as all commodities do. They fluctuated significantly during the review. Only gold and rice showed sustained increases in their prices for some periods.

Despite the perennial recurrence of the deficit, one could observe differences in its behaviour over time. One can start by looking at the gap between exports and imports. Two periods are chosen simply to avoid the contradictions that would arise from the rebasing the economy from 1988 prices to 2006 prices. From 1992 to 2004, the gap between exports and imports was relatively small. It averaged about US$55 million or G$9.2 billion per year. Trade during this period represented a high proportion of Guyana’s gross domestic product (GDP). Trade represented an average of 74 percent of GDP, reflecting the heavy dependence of Guyana on the external sector. This heavy dependence on the external sector meant that the Guyana economy could easily be disturbed by adverse events occurring in the external environment.

Despite the perennial recurrence of the deficit, one could observe differences in its behaviour over time. One can start by looking at the gap between exports and imports. Two periods are chosen simply to avoid the contradictions that would arise from the rebasing the economy from 1988 prices to 2006 prices. From 1992 to 2004, the gap between exports and imports was relatively small. It averaged about US$55 million or G$9.2 billion per year. Trade during this period represented a high proportion of Guyana’s gross domestic product (GDP). Trade represented an average of 74 percent of GDP, reflecting the heavy dependence of Guyana on the external sector. This heavy dependence on the external sector meant that the Guyana economy could easily be disturbed by adverse events occurring in the external environment.

Rate of growth

Since the rebasing of the economy, it appears as if the economy is less dependent on the external sector. Trade as a share of GDP has dropped about 33 percentage points. Looked at from that perspective, one gets the impression that the importance of trade to the Guyana economy has declined. But that is not so when one looks at the rate of growth of trade between the two periods. In the period 1992 to 2004, trade grew at an annual average of four percent per annum. However, during the years of 2006 to 2014, trade grew at an annual average of nine percent. The faster growth in trade indicates that the external sector remains a very critical factor in the economic development of Guyana. The Guyana economy is not closed and remains open for business with the rest of the world.

Heavy dependence

The heavy dependence on trade leaves Guyana perennially fetching a trade deficit. The gap between inflows and outflows tend to expand on account of the disadvantage that Guyana experiences in the areas of freight services, shipping insurance and international travel. Despite the higher dependence on the external sector in the years between 1992 and 2004, the expenditure on non-factor services was lower as compared to the period 2006 to 2014. Non-factor services represented about two percent of the total value of external trade in the earlier years. However, they grew to six percent of total external trade in the latter period of 2006 to 2014. Despite being higher, the pace at which non-factor services grew was much faster from 1992 to 2004 than it was from 2006 to 2014. Non-factor services grew at the rate of 20 percent per annum in the earlier period and at 12 percent during the latter period. This is a very interesting development considering that Guyana has increased its demand for technology licences and its dependence on franchise fees to meet the growing demand in the fast-food industry.

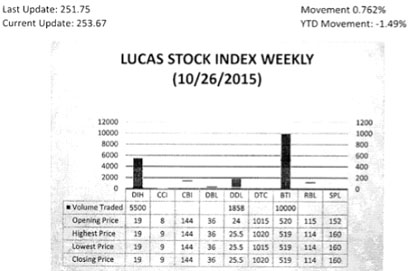

The Lucas Stock Index (LSI) rose 0.76 per cent during the final trading period of October 2015. The stocks of three companies were traded with 17,358 shares changing hands. There was one Climber and one Tumbler. The stocks of Demerara Distillers Limited (DDL) rose 6.25 per cent on the sale of 1,858 shares while the stocks of Guyana Bank for Trade and Industry fell 0.19 per cent on the sale of 10,000 shares. In the meanwhile, the stocks of Banks DIH (DIH) remained unchanged on the sale of 5,500.

Factor services which consist of migrant labour and things like interest payments and dividends have also displayed changed behaviour. In the earlier years of 1992 to 2004, factor services represented about seven percent of total trade. However that percentage has declined significantly to below one percent during the period 2006 to 2014. What is interesting too is that factor services have been making a positive contribution to the current account balance. The most significant factor service for Guyana has been remittances which have shown a steady positive contribution to the Guyana economy.

Despite the signs of encouragement coming from the factor services, the imbalance in financial flows as a result of international trade leaves Guyana depending on foreigners to do more than just buy our goods and services. For one thing, Guyana needed the help of other nations to make its trade payments. Between 1992 and 2004, a substantial amount of debt relief was required to help Guyana cope with the gaps in its financial capabilities. A major contribution came in 1996 when in excess of US$600 million of Guyana’s foreign debt was cancelled. Further substantial relief came in 2006 after the Multilateral Debt Relief Initiative (MDRI) kicked in. This initiative was developed to help poor countries to fight poverty while seeking to advance their economies. It made it possible for multilateral lenders like the International Monetary Fund, (IMF), the World Bank and subsequently the Inter-American Development Bank to provide 100 percent relief for highly indebted poor countries (HIPC). In 2006 and again in 2007, Guyana was able to shed the burden of its multilateral debts. Guyana continued to experience debt relief as recently as last year, but in much smaller amounts.

Size of flows

The financial accounts also offer some interesting developments in the effort to close the gap between exports and imports of goods and services. From 1992 to 2004, the flow of long-term investment was relatively modest. This level of flow perhaps reflected the uncertainty about the economic environment in Guyana. The highest inflow occurred in 1992 at the level of US$137 million and the lowest occurred in 2003 when US$26 million flowed into the country. In contrast, investment picked up in 2005 and began to grow at a steady pace before dipping below its peak of US$364 million in 2012. This period of private long-term financial inflows coincides with the period of substantial multilateral debt relief and perhaps a belief that the institutions that would such investments would be strengthened. The fears about corruption that were repeatedly expressed by foreign onlookers and domestic economic agents suggest that the institutional strengthening did not occur.

Other financial flows come to Guyana. These are more of a short-term nature and are not as substantial as foreign investments. Most of the short-term capital movements are attributed to the private commercial banks who are often involved in helping importers in particular to finance their purchases.

Prudent financial management

Guyanese should realize that until they can obtain better terms on which they trade, the trade gap will always be there. The information on financing the current account gap reveals also that Guyana benefitted significantly from the generosity of foreign donors who were willing to forgive a large portion of the country’s debt. Most of the debt was owed to multilateral lenders. It also shows that the country depends heavily on foreign investment as a means of covering its financial gap. Foreign donors were unlikely to come riding to Guyana’s rescue again. Hence, prudent financial management and continued foreign investment will be important to the future success of the country.