If corruption is a disease, transparency is an essential part of its treatment.

If corruption is a disease, transparency is an essential part of its treatment.

Kofi Annan, Former Secretary-General of the UN

As the world mourns the death of Kofi Annan, let us pause to remember that it was during his tenure that the United Nations Convention against Corruption (UNAC) came into being. Kofi Annan wrote the Foreword, and his thoughts on the effects of corruption will always be remembered as one of the best, if not the best, that have ever been articulated on the subject:

Corruption is an insidious plague that has a wide range of corrosive effects on society. It undermines democracy and the rule of law, leads to violations in human rights, distorts markets, erodes the quality of life and allows organized crime to flourish.

… Corruption hurts the poor disproportionately by diverting funds intended for development, undermining a Government’s ability to provide basic services, feeding equality and injustice and discouraging foreign aid and investment. Corruption is a key element in economic under performance and a major obstacle to poverty alleviation and development.

… The adoption of the United Nations Convention against Corruption will send a clear message that the international community is determined to prevent and control corruption. It will warn the corrupt that betrayal of the public trust will no longer be tolerated. And it will reaffirm the importance of core values such as honesty, respect for the rule of law, accountability and transparency in promoting development and making the world a better place for all.

… If fully enforced, this new instrument can make a real difference to the quality of life of millions of people around the world. And by removing one of the biggest obstacles to development it can help us achieve the Millennium Development Goals.

… Be assured that the United Nations Secretariat, and in particular the United Nations Office on Drugs and Crime, will do whatever it can to support the efforts of States to eliminate the scourge of corruption from the face of the Earth. It is a big challenge, but I think that, together, we can make a difference.

The question of how the oil revenue is to be used when it starts to flow into the Government’s coffers in 2020, has been a source of intense debate in recent weeks. This follows the thought-provoking suggestion of Prof. Clive Thomas that a portion of such revenues should be set aside and given as cash transfers to each household, with appropriate conditionalities so that the money could be used wisely to improve standards of living and lower poverty. Prof. Thomas’s suggestion might have been influenced by the results of the latest Labour Force Survey which showed that: (i) 35 percent of the population live below the poverty line; (ii) the level of unemployment is 12 percent; and youth unemployment is 17.3 percent for men, and 28 percent for women.

Today’s article examines the issue and considers that whatever the decision of policy makers in relation to cash transfers to households, and more generally how oil revenue is to be used, several factors need to be considered.

Sovereignty of Natural Resources

The natural resources of a country belong to all of its citizens. Not only its present generation should benefit from their exploitation but also future generations as well. Enough funds should therefore set aside for future generations. It is also appropriate to consider that funds surplus to our day to day requirements should be set aside and saved for when a ‘rainy day’ steps in. It is mainly for these reasons, and others, that the notion of a Sovereign Wealth Fund has been developed.

Natural Resources as Capital Assets

Natural resources are capital assets of a country. When such resources are exploited, they are converted into financial assets. In principle, the capital portion ought not to be used to meet operating expenses without eroding the country’s capital base. It should be set aside, and only the interest portion should be utilized for government programmes and activities.

In its report entitled, “Guyana: A Reform Agenda for Petroleum Taxation and Revenue Management”, dated November 2017, the International Monetary Fund (IMF) identified several specific challenges relating to revenue management in extractive industries. These include:

(a) Revenue can be potentially large but temporary, given the exhaustibility of the

natural resources;

(b) Revenue can be volatile and uncertain;

(c) Government spending is often procyclical, that is, it increases in lock-step with the extractive industry revenue;

(d) There is often the pressure to increase government spending upfront, sometimes by borrowing against future expected revenue; and

(e) These spending pressures often arise from elevated expectations from citizens as to the benefits from extractive industries projects.

The report suggested that these challenges can be addressed by designing a fiscal policy framework that reflects a balance between increasing investments in development projects on the one hand, and the need to set aside funds for stabilization and future generations, on the other. The first step is to calculate the total government wealth derived from oil. Given the uncertainties involved in terms of future oil prices, production volumes and costs, it would be prudent to come up with a range of government wealth estimates under different scenarios.

The second step is to calculate the sustainable income generated from the oil wealth. This is a notional measure of the return that should reflect the actual long run average return on financial savings. The report estimates the sustainable income from the initial oil wealth at US$137 million annually in real terms using also the discount rate of three percent. This is the amount of oil revenue that can be spent annually, while preserving the total government wealth from oil indefinitely. The third step is to repeat the calculation for each year throughout the planning horizon. Oil revenue produced in any given year above the estimated sustainable income will be saved in the form of financial assets.

Fossil fuels as Non-Renewable Natural Resources

Fossil fuels are an exhaustible resource and not a renewable one. It follows that extreme caution has to be exercised in dealing with revenue that flows from their extraction. One does not wish to create a vacuum in terms of expectations, after the resource is fully exploited and completely exhausted. This notion reinforces the need to remain focused on the various sectors that contribute to the economy and, to the extent possible, take appropriate measures to diversify the economy. As the saying goes, do not put all your eggs in one basket. We must also learn from the experience of other oil producing countries that have been afflicted by the Dutch disease and the ‘resource curse’.

No ‘big bang’ approach

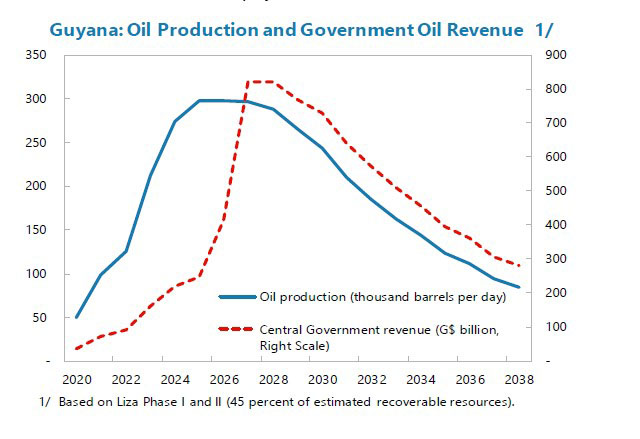

Based on ExxonMobil’s production schedule, extraction will commence in 2020 not in a ‘big bang’ way but rather at modest levels in the earlier years, progressively increasing and peaking perhaps six or seven years later, depending on market conditions. Thereafter, production will decline progressively until the resource is completely exhausted at around 2038, as shown below in the graph below.

The above graph was extracted from the 2018 IMF Article IV Report dated 31 May 2018, prepared by the IMF Staff and endorsed by the IMF Board of Directors on 15 June 2018. The report stated that the extent of oil discovery is conservatively estimated at 3.2 billion barrels. Based on Lisa Phases 1 and 2, production is expected to commence in 2020 with an estimated 50,000 barrels per day, progressive scaling up to its peak of 325,000 bpd at around 2026. The footnote indicated that some recent estimates have production as high as 120,000 bpd in 2020 (Liza I) and 340,000 bpd in 2025 (Liza I and Liza II combined).

An interesting aspect of the graph is the Government’s share of oil revenue which, for 2020 is estimated at around G$100 billion, equivalent to US$500 million. Production will scale up gradually during the next 7-8 years, peaking at around 350,000 bpd in 2028 when the anticipated Government revenue will be about G$800 billion, equivalent to US$4 billion. As production declines progressively during the next ten years, so will be the Government share of revenue. In 2038, production will come to an end as the oil resources will be completely exhausted.

Recovery of Capital Costs

In the early years of production, oil companies will seek to recover the cost of their investment. Therefore, using the profit-sharing model, the availability of profits for distribution between the oil company and the Government will not be as significant in the first five years or so. As the IMF report points out, “[t]he Government’s share will increase substantially once cost recovery on the initial investment is met (in the late 2020s), and most of production consists of ‘profit oil’.” We therefore need to temper our expectations as to the extent of oil revenue that is likely to flow in the first six or seven years, and plan accordingly.

The Production Sharing Agreement with ExxonMobil provides for the Government to reimburse Exxon the sum of US$460 billion representing pre-contract costs incurred during the period 1999 and December 2015 as well as “such costs as are incurred under the 1999 Agreement between January 1, 2016 and the effective date which shall be provided to the Minister or on before 31 October 2016 and such number agreed on or before 30 April 2017”. The total pre-contract costs could be as high as US$900 million, as suggested by some experts.

The IMF has also estimated the total capital costs incurred on Lisa Phases I and II to be around US$4.4 billion. It this is to be recovered during the first five years of production, there will be an annual charge against revenue of US$880 million, and the extent of profits to be shared between Exxon and the Government will be affected accordingly.

When the Government’s liability in respect of pre-contract costs is taken into account, one must not discount its adverse impact on oil revenue in the early years, unless an agreement is reached with Exxon to delay the settlement of this liability until the peak period of production.

Volatility of oil prices

Over the last year or so, the price of WTI crude oil has climbed from around US$50 to US$68 per barrel. However, there is no guarantee that oil prices will continue to rise. If the reverse were to happen, profitability will correspondingly decrease, and it is possible that there may come a time when it may no longer be economically feasible to extract the oil. One also needs to consider the role of OPEC in setting production levels for crude oil, which will have implications on the world market price.

The Paris Accord on Climate Change

There is no doubt that climate change is a man-made phenomenon. The Paris Accord, signed by 195 countries, has committed countries to take appropriate measures to limit the use of fossil fuels and to switch to renewable sources of energy. The European Union countries have pledged to reduce emissions by 40 percent by 2030. France announced plans to ban all petrol and diesel vehicles by the year 2040. It will also no longer use coal to produce electricity by 2022 and is committed to investing four billion euros to boost energy efficiency. Germany has published a 30-year climate change strategy, including the cutting of greenhouse gases by 80-95% by 2050; and significantly lowering car emissions with e-cars contributing to this goal. As of 2015, Germany increased the power production of renewable energy by 30%. Sweden has also decided that it would go carbon-neutral by 2045.

Given the above, there is likely to be a decline in the production and use of fossil fuels in the not too distant future. The effect of this is a likely drop in the price of crude oil which in turn will have implications for oil revenue for Guyana.

Conclusion

The Government needs to be extremely cautious in terms of the use of oil revenue that will flow with effect from 2020. Perhaps the most important area is the need to establish the Sovereign Wealth Fund along the lines recommended by the IMF in order to set aside adequate for future generations and to provide for situations of grave national emergencies or disasters, such as an act of war, an earthquake, a tsunami or a prolonged and severe drought.

Other areas that need to be given priority are:

(a) Enhancing fiscal discipline by having a balanced budget, instead of a deficit one.

For too long, the economy has been burdened by deficit budgeting which has to

be financed by borrowings. For example, the budget deficit for 2018 is G$33.412

billion;

(b) Reducing, if not eliminating, the public debt which stands at over 50 per cent of

the gross domestic product since there will be significant savings on interest

charges; and

(c) Eliminating the massive overdraft on the Consolidated Fund which currently

stands at around G$150 billion.

Only when the above measures are achieved, should there be a consideration for cash transfers to households as suggested by Prof. Thomas. In any event, the National Budget could include specific measures to address the issue of employment and poverty-alleviation measures.