Government operations should be transparent such that citizens and the media can provide oversight and hold officials accountable. In addition, procurement processes that comply with international anti-corruption standards will ensure a level playing field for investors. Private sector actors must also answer for any role that they play in corrupt practices, and when choosing private sector partners it is advisable to choose the reputable over the most convenient. Most importantly, a robust civil society and free press are critical to holding leaders responsible for their actions.

We continue to look forward to the government’s initiatives to combat corruption, including Natural Resource Fund legislation that offers both transparency and clear oversight, and to a meaningful and inclusive process of stakeholder engagement. A strong anti-corruption stance now will show Guyanese citizens, and the rest of the world, that the government is committed to transparent institutions that utilize the country’s resources to the long-term benefit for all Guyanese.

Extract of statement from the U.S. Embassy on

International Anti-Corruption Day

After a three months’ break, we resume our Accountability Watch column today. During this period, some important developments took place which under normal circumstances would have attracted our attention since they impact adversely on good governance, transparency and accountability. These include: the controversy over the frequency of meetings of the Public Accounts Committee (PAC); status of the audit of the US$460 million ExxonMobil’s pre-contract costs; failure to audit some US$9.5 billion in expenditure incurred by Exxon; the functioning of the National Procurement and Tender Administration Board (NPTAB); and the award of certain contracts that breached the Public Procurement Act.

In today’s article, we discuss the recent controversy over the frequency of holding meetings of the PAC as well as the decision to scrutinise several years of public accounts together, in an effort to clear the backlogged examination of the public accounts.

PAC’s role in the public accountability cycle

The public accountability cycle does not end when the Auditor General’s report on the public accounts is laid in the National Assembly. There are two more important steps to be completed: the PAC’s scrutiny of the said accounts and reporting back to the Assembly; and the Government’s response in the form of a Treasury Memorandum setting out what actions it has taken or proposes to take in relation to the Committee’s findings and recommendations. Ideally, the cycle should be completed within 12 months of the close of the fiscal year to enable citizens to consider whether the Government has fully discharged its financial stewardship. Additionally, the availability of the PAC report on the previous year’s public accounts provides legislators with an important source of reference when considering the Estimates for the next fiscal year. It is undesirable for the Assembly to approve the Estimates for the forthcoming fiscal year without first ensuring that a full and proper account has been rendered for the amounts allocated in the previous year to meet expenditure on Government programmes and activities.

All the stages in the accountability cycle from budget preparation to the issue of the Treasury Memorandum have specific deadlines, except the PAC’s scrutiny of and reporting on the public accounts. This is most unfortunate, considering that in the post-1992 period, it took on average more than four years for the Committee to complete its examination and reporting of the public accounts for a particular fiscal year. At this rate, the results of the PAC’s scrutiny of the 2020 accounts will not be known until 2024, or perhaps later, unless decisions that are devoid of political considerations are taken to expedite the Committee’s work.

This is not to suggest that there should not be a thorough and comprehensive scrutiny of the public accounts which, it is to be noted, should include not only central government activities but also those of the wider public sector – public enterprises, statutory bodies and other entities in which controlling interest vests with the State, local government bodies, and foreign-funded projects. So far, the PAC has only concerned itself with central government activities although the accounts and operations of the wider public sector are perhaps in greater need of scrutiny. Over the years, some of the entities involved have become a severe financial burden on the Treasury. Why, for example, are the audited financial statements of Guyana Sugar Corporation, Guyana Power and Light, Guyana Water Inc., and National Industrial and Commercial Investments Limited (NICIL) not scrutinized by the PAC? Do all such entities present their audited accounts to the Assembly within six months of the close of the year, as required by the law? And why are these accounts not referred to the PAC for detailed examination?

Work of the PAC in the pre-1992 period

At the time I was appointed Auditor General in late 1990, the PAC had not issued its reports on the public accounts for the fiscal years going back to the 1970s although its examination of these accounts had been substantially completed up to 1981. Concerned about the state of public accountability existing at the time as well as my own enthusiasm to assist in restoring matters to some semblance of normalcy, I offered to draft the PAC reports. The Committee, under the chairmanship of the late Reepu Daman Persaud, accepted my offer. Notwithstanding the arduous and time-consuming task of going through the verbatim records of the meetings of the PAC to piece together while at the same time attending to my day-to-day responsibilities, I was able to complete the exercise in a little of a year. When I submitted the draft reports to the Committee, they were accepted in their entirety and issued as final reports to the Assembly. Since there were no public accounts for the years 1982-1991, the work of the PAC was brought up-to-date as of 1992.

At the time I was appointed Auditor General in late 1990, the PAC had not issued its reports on the public accounts for the fiscal years going back to the 1970s although its examination of these accounts had been substantially completed up to 1981. Concerned about the state of public accountability existing at the time as well as my own enthusiasm to assist in restoring matters to some semblance of normalcy, I offered to draft the PAC reports. The Committee, under the chairmanship of the late Reepu Daman Persaud, accepted my offer. Notwithstanding the arduous and time-consuming task of going through the verbatim records of the meetings of the PAC to piece together while at the same time attending to my day-to-day responsibilities, I was able to complete the exercise in a little of a year. When I submitted the draft reports to the Committee, they were accepted in their entirety and issued as final reports to the Assembly. Since there were no public accounts for the years 1982-1991, the work of the PAC was brought up-to-date as of 1992.

Work of the PAC in the post-1992 period

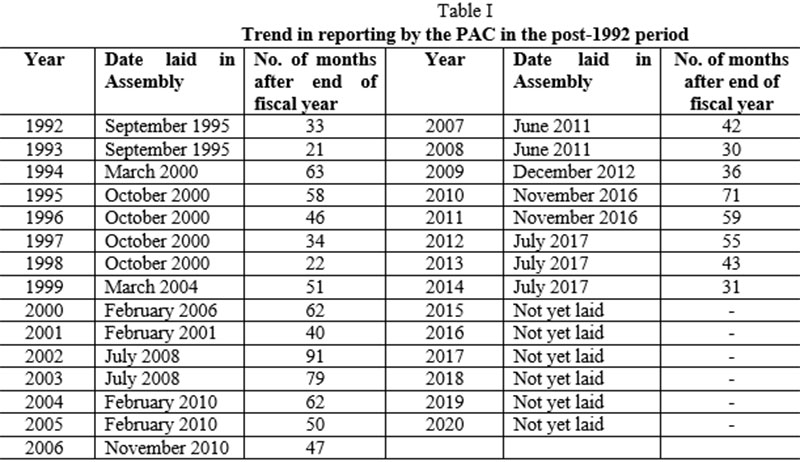

It is most disheartening that successive PACs have allowed its work to drag on, resulting in the present situation in which the current PAC has found itself. Table I shows the trend in reporting by the Committee in the post-1992 period.

As can be noted, the reports of the PAC for 1992 and 1993 were issued in September 1995. They were prepared by the Chairman himself, the late Dr. Kenneth King who declined my offer of assistance. During the Committee’s examination, both the Chairman and the other Opposition members were critical of my almost single-handed effort to restore public accountability. They took an extremely partisan approach in the scrutiny of the accounts for those years. Immediately thereafter, Dr. King resigned from the Committee and was replaced by the late Winston Murray under whose chairmanship I resumed the task of drafting the PAC reports. At the time I left for Africa to serve as the Chief Resident Auditor of the United Nations Peacekeeping Operations, the PAC was able to compete its examination and reporting of the public accounts for the years 1994 to 1998. I returned to Guyana in August 2004 and demitted office shortly thereafter.

Over the years, the PAC took the unprecedented approach of considering several years of the public accounts together: 1995-1998, 2000-2001, 2002-2003, 2004-2005, 2007-2008, 2010-2011 and 2012-2014. As it stands, there are six years of backlogged accounts to be reported on. By the time the PAC gets its act together, the findings and recommendations of the Auditor General will be overtaken by time; heads of budget agencies and other officials may also not be in place to provide the necessary answerability to the Committee; and the most recent years will be added to the backlogged accounts, thereby compounding matters. The PAC’s examination of the public accounts for the backlogged years will therefore hardly serve any use in terms of the actions that are needed to remedy the deficiencies identified by the Auditor General and to hold those responsible to account. Is it any wonder that the findings and recommendations of the Auditor General keep repeating themselves year after year? In these circumstances, the task of the Auditor General becomes an easy one: take the previous year’s report and update it with new figures. In other words, there is no incentive for the Audit Office to take a fresh approach during the audit process while the PAC’s preoccupation with the backlogged accounts offers little or no comfort in terms of providing the necessary guidance to the Audit Office in relation to current and future audits.

The last report of the PAC, issued in July 2017, was in respect of the combined fiscal years 2012-2014. The Committee has completed its examination of the 2015 accounts and is currently scrutinizing those for 2016 before it issues its report for the combined years 2015-2016. On 20 September 2021, the Auditor General presented his report on the 2020 accounts to the Speaker of the Assembly. Since the 2001 amendments to the Constitution that provide for the Auditor General’s reports to be submitted to the Speaker instead of the Minister of Finance, it has been the practice for such reports to be presented to the Assembly at its very next sitting. The report was laid yesterday.

In an attempt to expedite the scrutiny of the backlogged accounts, the PAC had agreed to meet twice per week, instead of weekly. Regrettably, this decision was reversed on the ground that the increased frequency of PAC meetings will adversely impact on the work of the two Ministers of the Government sitting on the Committee as well as that of the Committee’s advisors, namely, the Auditor General, Finance Secretary and Accountant General. However, it has been the practice elsewhere where as far as possible there is an avoidance of sitting Ministers being part of the PAC, considering their busy work schedules as well the possibility of a conflict of interest when the Committee begins its scrutiny of the accounts of budget agencies for which they have ministerial responsibility. As regards, the advisors to the Committee, there is no requirement for them to be personally present at the meetings. They can send their deputies or other senior officers to the PAC meetings, as was done in the past.

Recently, the Chairman of the PAC suggested that the accounts for the fiscal years 2017, 2018 and 2019 be examined together. However, this suggestion did not find favour with the Government members. Eventually, the PAC agreed to combine the years 2017 and 2018.

The PAC’s examination of the public accounts for the fiscal years 2012-2014 was completed in 12 sessions over a seven-month period, giving an average of four sessions per fiscal year. During this period, the Committee met on three consecutive days on one occasion. In contrast, it took 52 sessions of the PAC to complete its scrutiny of the public accounts for the fiscal years of 2010-2011 over a 27-month period, giving an average of 26 sessions per fiscal year. While we continue to applaud attempts by the PAC to expedite its work, we sincerely hope that the desired level of thoroughness/comprehensiveness so vitally necessary to ensure the proper accountability for the use of public resources, will in no way be compromised. We continue to maintain this position.