The problem is not simply fossil fuel emissions. It’s fossil fuels – period. The solution is clear: The world must phase out fossil fuels in a just and equitable way – moving to leave oil, coal and gas in the ground…Fossil fuel companies must also cease and desist influence peddling and legal threats designed to knee-cap progress.

The problem is not simply fossil fuel emissions. It’s fossil fuels – period. The solution is clear: The world must phase out fossil fuels in a just and equitable way – moving to leave oil, coal and gas in the ground…Fossil fuel companies must also cease and desist influence peddling and legal threats designed to knee-cap progress.

Fossil fuel industry transition plans must be transformation plans, that chart a company’s move to clean energy – and away from a product incompatible with human survival. Otherwise, they are just proposals to become more efficient planet-wreckers. – UN Secretary-General Antonio Guterres

Local democracy is an integral and indispensable aspect of any democratic system. Perhaps the most important aspect relates to the holding of periodic elections in accordance with the law, where citizens choose among themselves who should manage the affairs of their communities on their behalf. Last Monday, Guyana held its fourth local government elections since it gained Independence some 57 years ago, although the law requires such elections to take place every three years. The first elections were held in 1970, and it took 24 years for the next elections to be conducted. This was in 1994. One would have thought that with central democracy restored in 1992, there would have been strict adherence to the law as regards local government elections. However, this was not to be, as the next elections took another 24 years to be held. This was in 2018 during the third year of the APNU+AFC Administration. Last Monday’s elections would have marked five years since the third elections were conducted.

As expected, given the lackluster performance so far of the political opposition following attempts to tampering with the results of the 2020 national and regional elections as well as the almost exclusive access to State resources by the ruling party during the elections campaign, the results of the 2023 local government elections did not surprise anyone.

They show overwhelming victory for the PPP/C, winning control over 56 out of the 70 Neighbourhood Democratic Councils (NDCs); while the remaining 14 went to the APNU. In respect of the ten municipalities, the results showed that the APNU won three, namely, Georgetown, New Amsterdam and Linden. In Bartica and Mahdia, there was a tie with both the PPP/C and the APNU obtaining equal number of seats through a combination of proportional representation and constituency system.

However, since the PPP/C gained the plurality of votes, the mayorship of these two municipalities will go to that party. The remaining five municipalities – Corriverton, Rose Hall, Mabaruma, Anna Regina and Lethem – all went to the PPP/C. The ruling party will therefore be in control of seven of the ten municipalities.

Media reports, however, indicate that voter turnout was low at around 30 percent, compared with the 2020 national and regional elections where the turnout was 70 percent. Caution therefore needs to be exercised in interpreting these results as an indicator of what is likely to be expected in the next general elections due in two years’ time. There were 12 NDCs for which there was no voting because only one political party fielded candidates. According to Section 54 of the Local Authorities (Elections) Act, if only one list of candidates for any local authority area has been approved, the persons whose names appear on the list shall be deemed to have been elected as Councillors due to the approved list being unopposed.

Therefore, the candidates in that list shall be declared the winner of the election. The 12 NDCs are Leguan, Canals Polder, La Jalousie/Nouvelle Flanders, Herstelling/Little Diamond, Bath/Woodley Park, Bloomfield/Whim, No. 64/No.74, Kintyre/No. 37 Borlan, Ordinance/Fort Lands No. 38, Kilcoy/Hampshire, Port Mourant/Johns and Aranaputa/Upper Burro Burro. There was also only one list of candidates for municipality of Lethem.

In today’s article, we discuss the importance of local democracy as well as financial accountability of local government bodies, bearing in mind that in societies that embrace democratic norms and values, democracy (whether central or local), accountability can be considered the twin sides of the same coin. Democracy leads to accountability which in turn facilitates development, including social progress. A lack of democracy invariably leads to stagnation in development which in turn leads to a lack of accountability.

Importance of local government democracy

In our article of 17 March 2014, we had referred to a joint statement from the ABC (Unites States of America, the United Kingdom and Canada) countries calling for local government elections to be held by 1 August 2014 since they were overdue for 17 years. In that statement, the ABC countries noted that international development agencies have long recognized the tangible benefits of local democracy going beyond the act of casting a vote, and that elections would bring ‘much needed reinvigoration into local government entities’. They argued that:

Effective and efficient public administration coupled with healthy local governance can drive development efforts. Local government institutions bring government closer to the people, fostering greater inclusion, civic responsibility, empowerment and participation…It is only when people have transparent and accountable institutions at all levels of government – national, regional, and local, will they have confidence in their future.

A significant portion of the Constitution is devoted to local democracy. For example, Article 171 (1) states that local government is a vital aspect of democracy and shall be organized so as to involve as many people as possible in the task of managing and developing the communities in which they live. Other sections of the Constitution provide for local democratic organs to, among others:

Ensure in accordance with law the efficient management and development of their areas and to provide leadership by example (Article 74 (1));

Organise popular cooperation in respect of the political, economic, cultural and social life of their areas and cooperate with respect of social organisations of the working people (Article 74 (2)); and

Maintain and protect public property, improve working and living conditions, promote social and cultural life of the people, raise the level of civic consciousness, preserve law and order, consolidate the rule of law and safeguard the rights of citizens (Article 74 (3)).

Financial accountability of municipalities

Section 177 of the Municipal and District Councils Act requires all accounts of Municipal and District Councils to be prepared not later than four months after the end of each year and for those accounts to be audited as soon as practicable thereafter. The responsibility for the preparation of the annual financial statements rests with the Treasurer who shall be guilty of an offence if he/she neglects to do so. The Auditor General is the appointed external auditor of all local government bodies.

According to the 2021 Auditor General’s report, nine of the ten municipalities had a combined total of 105 years of audit outstanding; while in respect of the Corriverton Town Council, the accounts were in such a bad shape that disclaimers of opinion were issued on the eleven sets of accounts covering the period 2002 to 2012. In relation to the NDCs, the majority of them were significantly in arrears in the submission of financial statements for audit. In particular, a total of 40 NDCs did not present financial statements for the years 2018, 2019 and 2020.

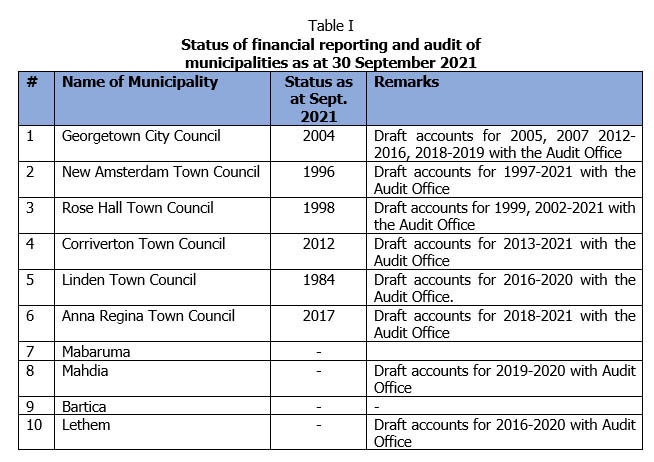

Table I provides the status of financial reporting and audit of the ten municipalities as at 30 September 2021.

As can be noted, the last set of audited accounts of the Georgetown City Council was in respect of 2004. However, draft accounts were received by the Auditor General for nine years without any indication as to how long they were with his office waiting to be audited. As at 31 December 2004, the City Council was only three years in arrears in terms of financial reporting and audit, and there were no gaps. As of September 2021, it was 17 years in arrears through a combination of apparent neglect on the part of the City Treasurer and the failure by the Auditor General to audit and certify financial statements received from the City Council. A similar situation exists as regards the other municipalities where the Auditor General was in possession of 69 sets of accounts waiting to be audited.

Bartica and Mabaruma have not had financial reporting and audit since they became municipalities.

Financial accountability of NDCs

Again, according to the 2021 Auditor General’s report, the majority of NDCs were significantly in arrears in the submission of financial statements for audit. In fact, the audits of only nine NDCs were finalized in 2021; while 40 NDCs did not submit financial statements for the years 2018, 2019 and 2020. Similar comments were made in earlier reports of the Auditor General.

However, as in the case of municipalities, numerous draft financial statements have been received by the Auditor General and were awaiting audit examination and certification.

Conclusion

Financial accountability of local government bodies is in a complete state of disarray. It has been a source of neglect for the longest while, without any evidence of action taken to sanction those responsible for this sad state of affairs. With the recently concluded local government elections and the announcement of the results, among the first tasks of those who have been elected to serve their communities, must of necessity be to take stock of the financial affairs of the entities involved and institute all the necessary measures to bring about some degree of respectability with regard to the financial management and accountability of the bodies involved.

The Auditor General is also not without blame. His office must make every effort to audit and certify the accounts submitted to him, within a reasonable time. As part of his annual report to the National Assembly, the Auditor General should compile a list of the 80 local government bodies showing the status of financial reporting and audit. In this way, the Assembly and hence the public would be in a position to determine which entities are delinquent in discharging their financial stewardship.

Finally, a significant amount of public resources is normally allocated to local government bodies via the Estimates of Revenue and Expenditure. Parliamentarians must therefore demand proper and timely financial accountability of these bodies before approving new allocations to them. Anything less is to encourage the continuation of the present undesirable practice.