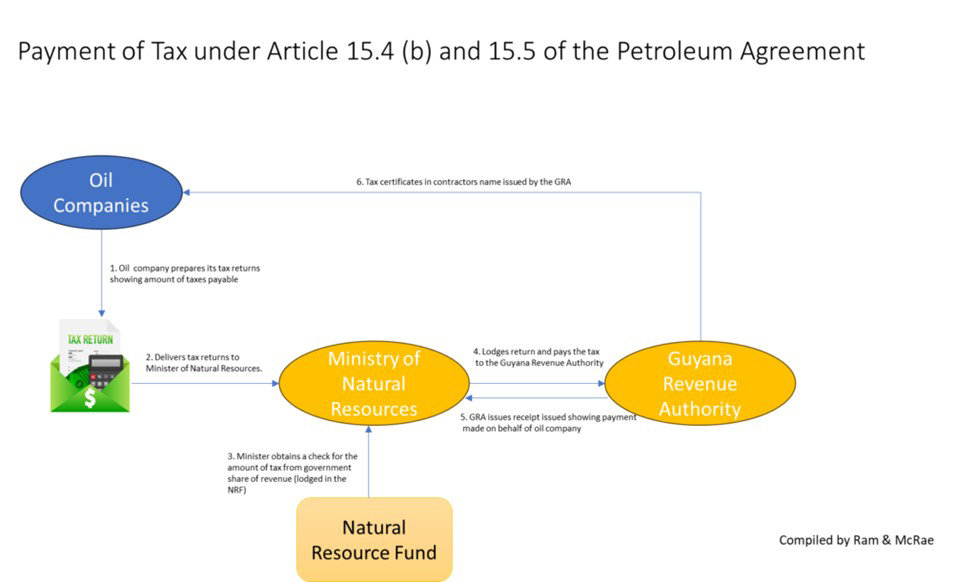

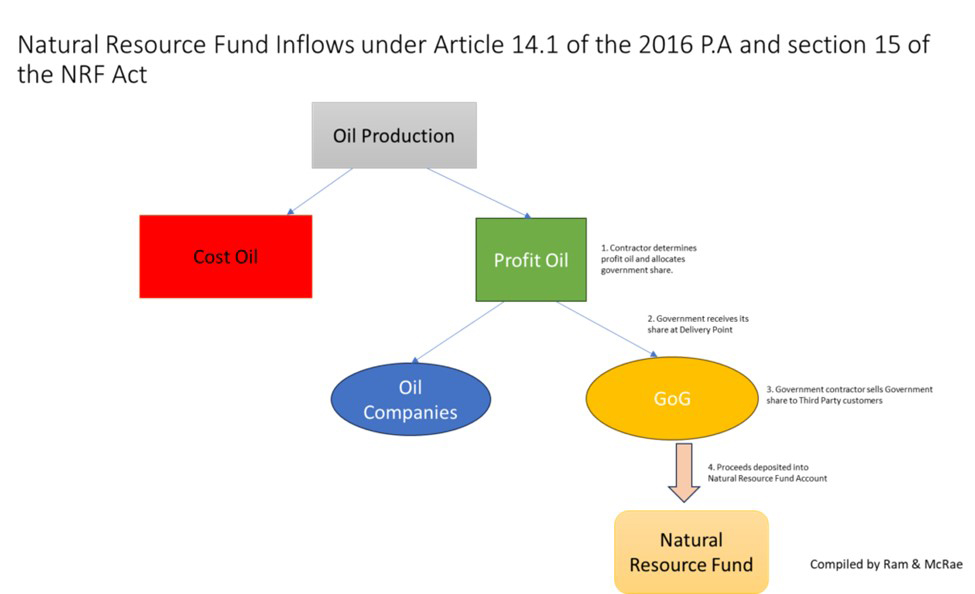

In last week’s article, we referred to the exchanges between Chartered Accountant and Attorney-at-law Christopher Ram, and the Attorney General as to whether the Natural Resource Fund (NRF) has been overstated to the extent of ExxonMobil’s subsidiaries tax liabilities that are required to be paid over to the Guyana Revenue Authority (GRA). With the kind permission of Mr. Ram, we reproduce the two flow charts he had produced to explain the movement of funds for the benefit of readers who may still be unclear on the matter.

We had stated that there is no doubt that the balance on the NRF account includes Exxon’s income and corporation tax liabilities since there is no evidence that payments were made to the GRA. The NRF Act 2021 specifically states that all withdrawals from the NRF must be paid over to the Consolidated Fund to be used only to finance: (i) national development priorities, including any initiative aimed at realizing an inclusive green economy; and (ii) essential projects that are directly related to ameliorating the effects of a major disaster. It has been argued that the net effect would have been the same had payments been made to the GRA which is required to transfer all tax collections to the Consolidated Fund. However, there are no short cuts in accounting; no netting off of transactions which is a fundamental principle in accounting; and one must be prepared to “take the long road” in the interest of transparency and proper accountability. That apart, the NRF and the Consolidated Fund are separate and distinct, and they serve different purposes.

We had stated that there is no doubt that the balance on the NRF account includes Exxon’s income and corporation tax liabilities since there is no evidence that payments were made to the GRA. The NRF Act 2021 specifically states that all withdrawals from the NRF must be paid over to the Consolidated Fund to be used only to finance: (i) national development priorities, including any initiative aimed at realizing an inclusive green economy; and (ii) essential projects that are directly related to ameliorating the effects of a major disaster. It has been argued that the net effect would have been the same had payments been made to the GRA which is required to transfer all tax collections to the Consolidated Fund. However, there are no short cuts in accounting; no netting off of transactions which is a fundamental principle in accounting; and one must be prepared to “take the long road” in the interest of transparency and proper accountability. That apart, the NRF and the Consolidated Fund are separate and distinct, and they serve different purposes.

We suggested that the solution to the problem lies perhaps in the amendment to the NRF Act to provide for a third category of payments, that is, to discharge Exxon’s liabilities to the GRA. However, apart from the absence of ring-fencing provisions, how does one seek to amend legislation to cater for one of the most egregious and dishonorable aspects of the PSA? Alternatively, if it can be argued that payment to the GRA falls within the category of “national development priorities”, then there is no need to amend the Act.

In today’s article, we review the audited accounts of Ministries/Departments/Regions which include both Appropriation Accounts and Statements of Receipts and Disbursements, for the fiscal year ended 31 December 2022.

Certification of accounts

There are over 200 Appropriation Accounts and Statements of Receipts and Disbursements of Ministries/Departments/Regions. The Auditor General’s certification was only in relation to the eleven sets of statements constituting the consolidated public accounts. However, in the body of his report, the Auditor General did state that these accounts and statements are subject to his comments under the relevant sections of his report. In principle, each set of financial statements, including the more than 200 appropriation and revenue accounts, should be certified individually to avoid a situation where a blanket opinion is issued covering accounts that are in good shape and with less queries as well as those that are not so. Perhaps, an abbreviated version of the audit opinion can be attached to each account, with words to the effect ‘in my opinion the Appropriation and Revenue Accounts of, say, the Ministry of Finance, properly present the revenue and expenditure for the fiscal year ….’

Highlights of the report

Overpayments to contractors

The Audit Office examined 466 contracts and found overpayments totalling $52.827 million on 33 contracts based on measured works against bills of quantities. This represents 7.1 percentage of the contracts awarded, an indicator that the level of monitoring and supervision of the works needs to be improved. Although some recoveries were made, $17.121 million remained outstanding at the time of reporting. The unrecovered overpayments were mainly in relation to the regions. A similar observation was made in 2021 where, of the 411 contracts were examined, overpayments totalling $52.996 million were made on 37 contracts. The incidence of overpayments to contractors has been a regular feature of the Auditor General’s reports over the years with little or no evidence of any action being taken to remedy the situation.

Contracts awarded to blacklisted contractors

The Region 9 Administration awarded two contracts valued at $20.350M to a contractor who has been blacklisted by the Public Procurement Commission. A similar observation was made in 2021 where eight contracts totalling $106.830M were awarded to a blacklisted contractor.

Termination of contracts due to poor performance

Contracts for the material stockpile and rehabilitation of Mahdia Main Access, the construction of Timber Wharf and Landing and the construction of GMC Packaging Facility at Sophia, were terminated due to poor performance by the contractors. A similar observation was made in 2021 where contracts for the re-construction Imbaimadai Police Station, construction of Primary school at Waramadong and the rehabilitation of Lola Street in Cane Grove were all terminated due to poor performance by the contractor.

These observations highlight the need for the Authorities to critically examine the basis of award of contracts to ensure that only qualified and competent contractors with proven track record of performance are awarded contracts. A convenient starting point is a review of the membership and operations of the various tender boards, especially the National Procurement and Tender Administration Board. There should also a more effective system of monitoring of the works to ensure their timely execution since there are additional cost implications arising from undue delays in the execution of the works, termination of contracts, and re-advertising of the works, among others.

Cheques on hand

At at September 2023, eight budget agencies had 277 cheques valued at $352.613M still on hand. It is unclear what these payments represented and why the cheques were held so long after the close of the fiscal year. In any event, the cheques had become stale-dated and should be cancelled. As a result, the respective appropriation accounts were overstated by the above amount. A similar observation was made in 2021 where there were 162 cheques valued at $623.404 million still on hand. Could it be a situation where cheques are drawn close to year-end in order to exhaust voted provisions, considering that all unspent balances at the end of the year have to be refunded to the Consolidated accounts?

Unpresented payment vouchers

The Auditor General reported that 426 payment vouchers valued at $1.110 billion were not presented for audit. A total of 54 vouchers for $887.330 million were in respect of Guyana Defence Force, while 372 valued at $223.108 million were in respect of the Region 5. The Auditor General concluded that in the absence of vouchers and supporting documents, he was unable to ascertain whether value was received for the sums involved, and whether the funds were used for the purposes intended. In the absence of vouchers and supporting documents, was it possible that alternative auditing procedures could have been adopted to ensure that value was received in respect of these payments?

Advance payments for the procurement of goods and services (Cheque Orders)

Several Ministries/Departments/Regions continued to clear cheque order vouchers through the submission of bills, receipts and other supporting documents, long after the stipulated time frame for doing so. As of September 2023, a total of 490 cheque orders valued at $1.739 billion remained outstanding, 278 of which for $1.466 billion were in relation to 2022, while the remaining 212 totalling $273.282 million were in relation to prior periods. The Auditor General concluded that he was unable to determine whether the value was received for the sums shown as having been expended. This is a serious matter that reflects a lack of accountability and should be thoroughly investigated. Again, we could ask the question: In the absence of vouchers and supporting documents, was it possible that alternative auditing procedures could have been adopted to ensure that value was received in respect of these payments?

Procurement of drugs and medical supplies

The Ministry of Public Health received 19 Inter-Departmental Warrants valued at $3.554 billion from the ten Administrative Regions for the procurement of drugs and medical supplies on their behalf. According to the records of the Ministry’s Material Management Unit, drugs and medical supplies valued at $4.098 billion were dispatched to the Regions. However, there was no evidence of reconciliation of the amounts received by the Ministry with the value of drugs and medical supplies supplied to the Regions. This has been an ongoing problem highlighted by the Auditor General in several of his reports without evidence of any action taken to remedy the situation.

Additionally, drugs and medical supplies valued at $725.499 million had not been received by the Ministry of Health as of September 2023. Further, a total of 92,131 vials of Sputnik vaccine valued at $410.831M had expired and had to be disposed of.

Items purchased yet to be delivered

As of September 2023, various items purchased valued $733.554 million had not yet been delivered to the following Ministries: Ministry of Public Works – $4.842 million; Ministry of Health – $628.241 million; and Ministry of Home Affairs – $100.471million.

Guyana Revenue Authority

Out of the approved staff complement of 65, the Petroleum Revenue Department had a staff complement of 33 officers as at September 2023, giving a 49 percent vacancy rate.

Rehabilitation of Leguan Stelling

After almost five years, the rehabilitation works at the Leguan Stelling remained incomplete. The contract was awarded in September 2018 in the sum of $413.259 million and was later revised to $607.259 million. As at the end of 2022, the contractor was paid amounts totalling $465.455 million. The contractual duration period had since expired, and there was no evidence that an extension was granted.

Purchase of drainage pumps for NDIA

The National Drainage and Irrigation Authority (NDIA) made payments totalling $600.886 million for the design, supply, installation, and commissioning of nine fixed and three mobile high-capacity drainage pumps and associated structures/equipment. However, ten of the twelve engines supplied were determined to be undersized and incapable of running the pumps on a long-term basis. As a result, the NDIA requested the contractor to replace the ten engines. However, as of September 2023, the engines were yet to be replaced.

Financial reporting of the Amerindian Purpose Fund

The Ministry of Amerindian Affairs did not present financial statements for the year 2022 to account for amounts totalling $302.454 million that it had received on behalf of the Amerindian Purpose Fund. This was despite several requests made to the Ministry.

Status of implementation of recommendations

Of the 220 recommendations made in 2021, 74 or 34% were fully implemented, 98 or 44% were partially implemented, while 48 or 22% were not implemented.