Global financial meltdown

My efforts to draw readers’ attention to the fact that the Third World Debt Crisis, which started 30 years ago in Mexico (and as I noted Guyana also) is alive and well today is by no means intended to diminish the magnitude of today’s sovereign debt problems, which now centre on the First World economies. In my opinion, it is entirely justifiable today that this crisis should dominate both global media attention and international institutional responses. This state of affairs is attributable to the sheer size and importance of the affected First World economies, namely, Europe, Japan and the USA. In truth, the threats posed by their current debt crises are so severe that they strike at the very heart of the solvency, liquidity, and indeed survivability of the global financial system and economy.

Readers need to constantly keep in mind therefore that, at this historic juncture, the First World debt crisis poses the threat of systemic breakdown, not only to globalisation but indeed the very structure of the global capitalist system.

A useful example of this possibility can be interpreted from the media’s rightful concerns over the unduly prolonged fiscal cliff crisis in the United States. As I write, this crisis has morphed into calls for deep government spending cuts at a time of hesitant economic recovery, and another repeat of the debt ceiling impasse. Early resolution of this complex situation has grave implications for the global economic and financial system, because of the weight and influence of the United States, as the world’s leading economy. Economic and/or financial meltdown in the United States, despite the emergence of the formidable emerging economies of Brazil, Russia, India and China (BRICs) as trading and financial centres, cannot prevent its rapid transmission to the rest of the world.

A useful example of this possibility can be interpreted from the media’s rightful concerns over the unduly prolonged fiscal cliff crisis in the United States. As I write, this crisis has morphed into calls for deep government spending cuts at a time of hesitant economic recovery, and another repeat of the debt ceiling impasse. Early resolution of this complex situation has grave implications for the global economic and financial system, because of the weight and influence of the United States, as the world’s leading economy. Economic and/or financial meltdown in the United States, despite the emergence of the formidable emerging economies of Brazil, Russia, India and China (BRICs) as trading and financial centres, cannot prevent its rapid transmission to the rest of the world.

In my view, it remains true today that, as the metaphor goes, when the “United States sneezes, the rest of the world is at serious risk of catching a cold.”

Readers may not also be fully aware that lurking behind the fiscal cliff, government spending cuts, and debt ceiling crises in the United States, is a dire banking situation. Since the global financial crisis erupted in late 2007 more than 460 United States’ private banks have failed. The total value of the assets held by these failed banks is more than $680 billion. This situation compares with the failure of only 32 banks, in the preceding 5 years!

Globally, the private banking situation is equally bleak. Financial analysts are today claiming worldwide over 200 private banks are at risk; that is, they have regulatory authorities/credit bureaus ratings in the two lower tiers. The combined value of their assets is about US$45 trillion!

On top of all this, readers should also be aware of several major global banks having been recently caught and punished by regulators for fraudulent, corrupt, and other illegal activities. Indeed, there is a significant risk that others will soon to be similarly caught.

As examples, the huge transnational Swiss bank, UBS, has been hit with a fine of US$1.5 billion, by regulatory authorities for rigging the “fixings” of the London Interbank Overnight Rate (LIBOR).

The British bank, Barclays, was also fined US$0.5 billion. The German bank, Deutsche, is presently being investigated for tax evasion, accounting manipulation tied to derivatives, obstruction of justice, and other irregularities and illegalities. Further, several US banks have only this week been fined for the issuance of improper domestic mortgages.

It is my proposition here that, if one takes into account the severity of the banking crisis which undergirds the sovereign debt crises of the First World economies, it is difficult to exaggerate the contradictions presently facing the international financial system, globalisation, and indeed the global capitalist framework itself. In this alarming context, the ongoing Third World Debt Crisis adds to the global difficulties, and does not subtract from the First World Debt Crisis.

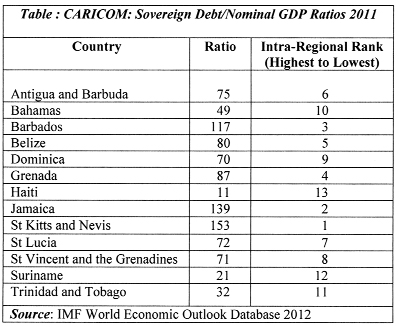

Caricom’s public indebtedness

With the proviso discussed above, let me conclude by directing readers’ attention once again to the TWDC. The table below shows the state of public indebtedness for Caricom countries, except Guyana, (which I shall examine separately). Placed in a wider global context, the information in the table informs us that at the end of 2011 Caricom was the most highly indebted region in the world, when measured on the basis of the public debt-to- GDP ratio!

Next week’s column will begin with further observations of the state of Caricom’s public indebtedness at December 31, 2011.

Next week’s column will begin with further observations of the state of Caricom’s public indebtedness at December 31, 2011.