This final column of this mini-series examining the financial statements of the three Contractors under the 2016 Petroleum Agreement, reviews their balance sheets, sometimes referred to as statement of affairs, as at December 31, 2020. The Table below is designed in a similar fashion as the summary income statement presented in Column 91. The comments on that Table applies to the Balance Sheet summary as well and readers might therefore wish to go back to that Column for a better understanding of this column.

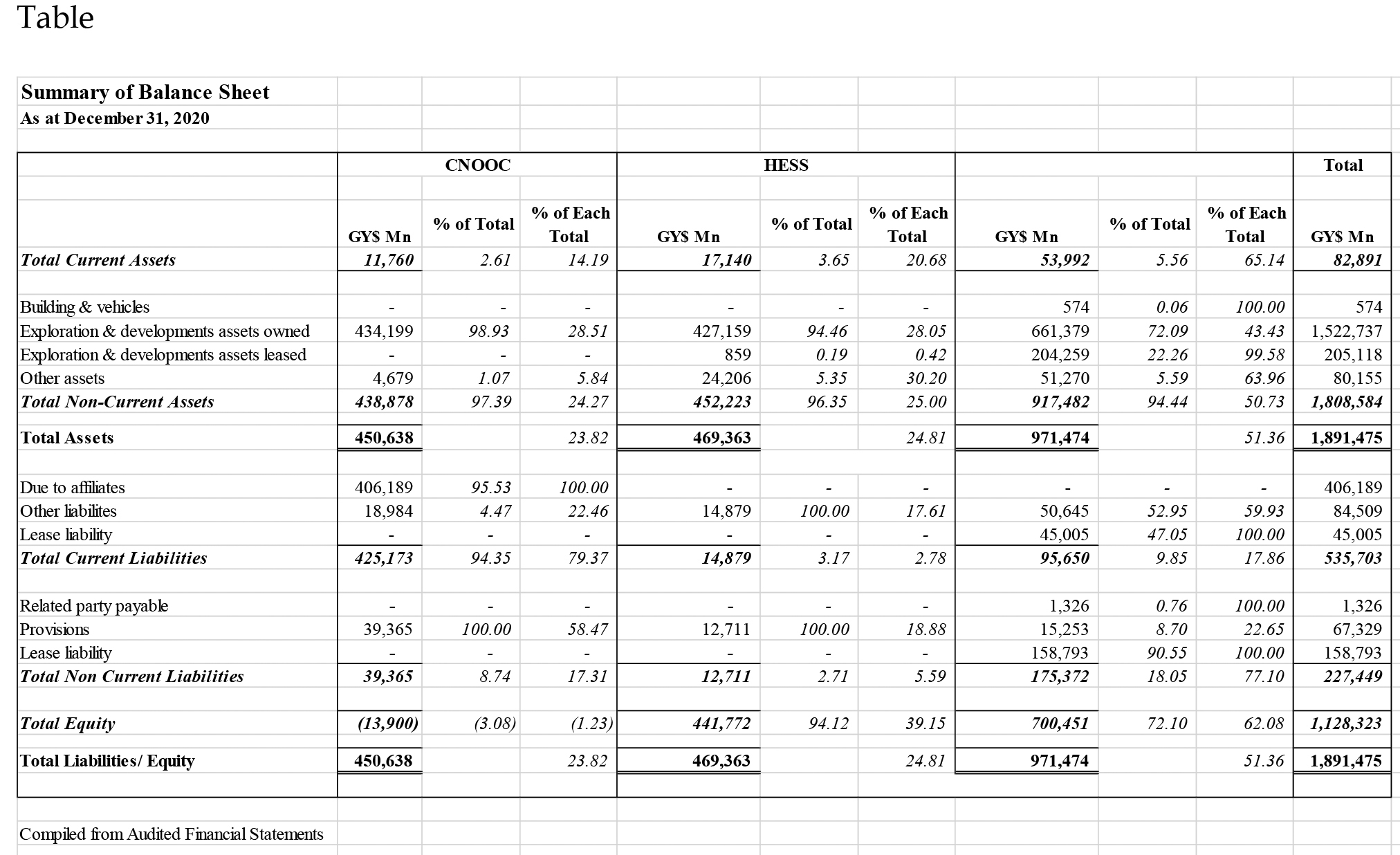

The total value of assets is $1,891 billion (approximately US$9.1 billion), of which $82.9 billion constitutes current assets, while non-current assets account for $1,808.6 billion, (approximately US$8,612 billion). The total “Equity participation” by the oil companies in the Stabroek Block is $1,128 billion (US$5.4 billion). Put simply, 60% of the assets of the three companies is financed directly by the entities. However, given the nature of branch accounts, this sum can be withdrawn at any time.

Non-current assets

Esso accounts for 51% of non-current assets while Hess and CNOOC share the balance almost equally. Exploration and development assets ($1,727 billion) make up 91% of the total assets of the three entities. Of this, assets owned by the entities account for $1,522 billion (US$724.8m) while $205 billion (US$976 million) is leased from third parties, which accounting rules require inclusion on the balance sheet, along with their corresponding liability. Of the owned assets, CNOOC contributes 29%, Hess 28% and Esso 43%, which also accounts for practically all the leased assets.

Of the three companies, only Esso has any interest in buildings, its financials disclosing net book value of $574 million in buildings and vehicles – a highly unusual combination of two very different classes of assets. More importantly, in violation of the intent of the Companies Act to restrict the ownership of land by external companies, Esso has been awarded a long-term lease of a substantial parcel of land controlled by Ogle Airport Inc. which however, is not separately identified in its financial statements.

CNOOC and Hess show as non-current assets some $450 billion and $469 billion, including, dubiously Deferred Tax Asset of $4.7 billion and $10.9 billion respectively. Since the 2016 Agreement relieves all three companies from any obligation to pay taxes on profits, the concept of deferred tax does not apply and should be disregarded for accounting purposes, as Esso does.

Current assets and liabilities

Current assets, comprising mainly of cash ($13.7 billion), receivables ($24.7 billion) and inventory of unsold crude oil ($36.2 billion) account for 4% of total assets. Of the current assets, Esso accounts for 65%, Hess 21% and CNOOC the remaining 14%. Of the $53.99 billion of current assets of Esso, 55% was held in inventory and 20% in accounts receivable. For Hess, 65% of current assets is held in accounts receivable and 35% in inventory. CNOOC holds 77% of its current assets in cash and its equivalent and 22% in receivables.

If one side of the balance sheet states the assets owned by the companies, the other side is made up of $695.8 billion in liabilities, $67 billion in provisions and $1,128 billion in what Esso describes as Equity contribution and Hess as Capital contributions, both terms being atypical of branches.

Total current liabilities of the three amounted to $535.7 billion (US$2.6 billion) with CNOOC accounting for 79%, Esso 18% and Hess 3%. The single most significant debt owed by CNOOC is an amount of $406.2 billion (US$1.9 billion) owed to an affiliate. The amount payable during 2021 on leased assets is G$45.0 billion, all by Esso. Other liabilities of the three partners amounted to $84.5 billion of which Esso is shown as owing $50.6 billion, Hess $14.9 billion and CNOOC $19.0 billion.

The joint-venture partners have a total of $67 billion in provision for decommissioning expenses at the end of the project life – possibly 25 years hence. By contrast, there is no provision for any emergency event, such as an oil spill. In this regard, the Agreement provides for the Government to fix any environmental damage if the companies do not promptly do so and to bill the companies for “reasonable costs and expenses” – not for all costs incurred. It is truly ironic that banks, insurance companies and airlines have to give bonds or lodge deposits to secure potential claims against them while oil companies, arguably engaged in the riskiest business of all, have no such obligation.

Hess shows $441 billion (US$2.1 billion) in Capital contribution or 39% of total capital contributed by the entities while Esso shows Equity contribution of $700.5 billion, representing 62% of the value of its assets. Incredibly, CNOOC had negative shareholders contribution, its assets being financed by short-term liabilities owed to an unnamed affiliate. In its 2020 Annual Report, ExxonMobil reports that “In partnership with the government of Guyana, we are efficiently developing these resources while maintaining active exploration to test multiple prospects.”

We recall from Column 91 that Esso’s direct exploration expenses of $18,286 billion (24% of its revenue), excluding the portion of General and administrative expenses of $20.8 billion (27% of revenue) which would also be allocable to its exploration activities. The claim that this is being done in the name of a partnership, not with Hess and CNOOC, but with the Government of Guyana, needs some explanation.

Conclusion

There is clearly an underlying agreement among the companies which is not available to the Guyanese public. Former Minister of Natural Resources Raphael Trotman might argue, as he initially did concerning the 2016 Agreement itself, that the confidentiality of such agreement is protected by law. There is no legal basis for such a position. And in any case, the financial statements of each of the companies should disclose, in sufficient detail, the nature of the relationship and the company’s rights, responsibilities and obligations.

Both the principles underlying their preparation and the contents of the financial statements reflect major deficiencies, including non-compliance with accounting Standards, requirements of the law and the Petroleum Agreement under which they operate. Reconciling the statements reviewed in this mini-series and the requirements of the Petroleum Agreement, or with the tax laws, would be a challenging task for those concerned.

Significantly, the Act requires financial statements of external companies, and not just of their Guyana branch which is what has been presented; the annual returns of these companies filed at the Commercial Registry are similarly non-compliant; and the Registrar of Companies was generous, if not careless, in permitting names of external companies which include the word “Guyana”.

These financial statements have vindicated the initial fears expressed about the limitations and weaknesses of the 2016 Petroleum Agreement. Those limitations and weaknesses have been compounded by the multitude of combined fatal deficiencies by the three oil companies in their financial reporting in the first year of oil production, averaging less than 100,000 barrels of oil per day. The opportunities for manipulation will increase correspondingly as production increases by eight and tenfold. It is incumbent on this Administration to separate itself as a partner in the financial shenanigans being perpetrated by the companies, introduce modern petroleum legislation, appoint independent and competent regulators and ensure that our laws are respected.

The Government should expect resolute pushback. The oil companies do not comply with a weak Agreement partly written by them, let alone a regime of regulations meeting international standards.

Finally, a word of appreciation to the several persons who shared their perspective with me on the last four columns. Next week’s column will respond to the IMF’s defence of the arrangement whereby the Government pays the tax of the oil companies.