Introduction

My two immediately preceding columns have been dedicated to exploring, for reader’s benefit the thesis advanced by Envision Research, which argues that, ExxonMobil, an iconic Global 500 corporation, can successfully turnaround its fortunes away from its heavy indebtedness and ongoing zombification – if it could arrive at a financial position where it is able to generate sufficient revenues to be able to invest in its own self-driven or organic growth. As has been revealed in previous columns, that circumstance is established through determining whether ExxonMobil’s rate of return on capital employed, ROCE, and the company’s reinvestment rate, RR. Therefore:

Long-term Growth Rate = ROCE* RR

ExxonMobil’s financial data for the period Q2 2021 to Q4 2021 [the most recently available], suggest something like a turnaround might be in the making, as was indeed hinted at in last week’s column.

Unfortunately, the elapsed time so far this year, < 3 months, is much too limited for making confident forecasts. Surveys of stock research and rating analysts, however, reveal a strong consensus in favour of hold for ExxonMobil stock; in preference to any other option, for example to buy, strongly buy, sell, or strongly sell. [See Wall Street Journal and, New York Times] Indeed, CNN Business also reports that a survey of 31 investment analysts [February 16 2022] recommended “hold” for ExxonMobil stock. This rating remains unchanged since the corporation’s Q4 report, released on February 1, 2022.

CNN Business further reports that 25 analysts offering 12-month forecasts of Exxon Mobil stock have revealed the following:

Median value = US$81.00

High value = US$105.00

Low value = US$62. 00

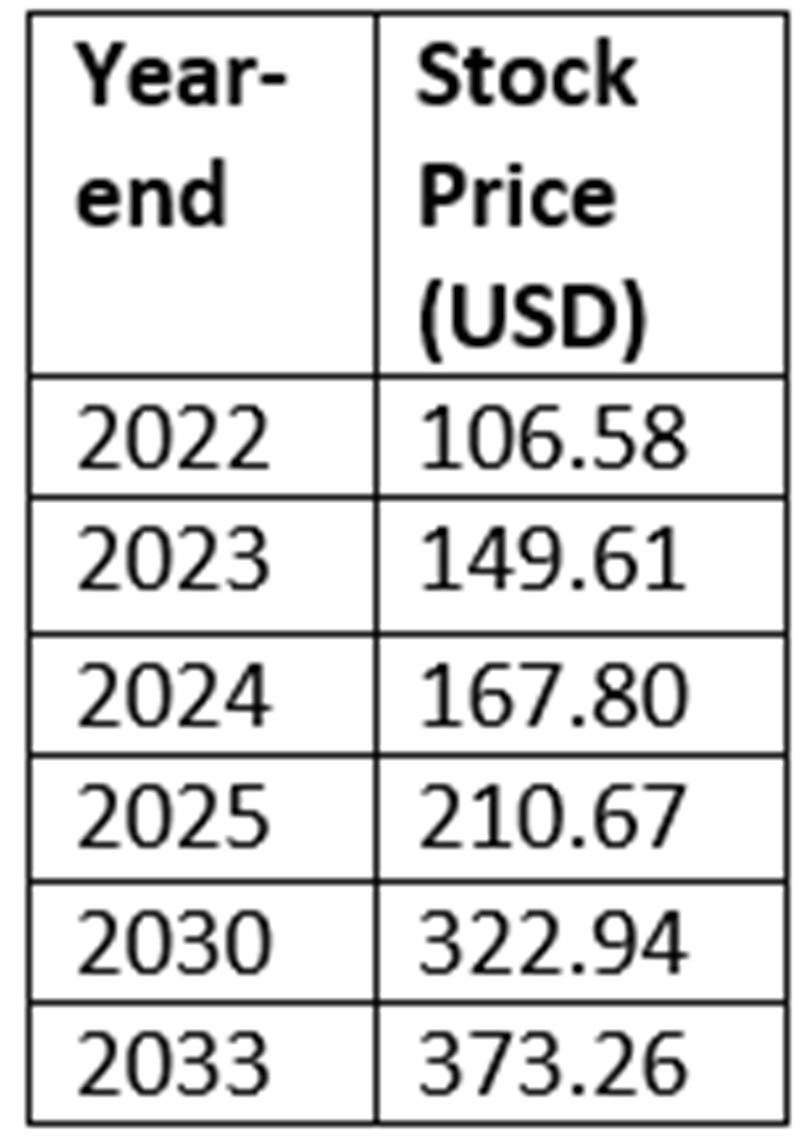

Stock price forecasting over a 12-month period is extraordinarily hazardous; due to market [demand: income, energy preference – mix as well as supply: cost, discoveries] and non-market [geopolitical, national conflicts and war] uncertainty and risks. Such uncertainty and risks grow exponentially when dealing with 1] the oil and gas sector and 2] when forecasting for long time periods. Considering this caution, I cite here a forecast by Coinbase of ExxonMobil stock price [US$] for the years 2022 to 2033. Schedule 1 reveals that: 1) the 2022 projected stock price [106.58] doubles by 2025; and 2) further grows by about 80 percent to 2033!

Coinbase: XOM Stock Price Forecast 2022- 2025 -2033

Takeaways Q4 2021 Results

For any of the gains in ExxonMobil’s stock prices, as projected above, to be realized over the near-term to the long-term, several of the key takeaways based on the corporation’s Q4 2021 results will have to be substantively realized. Among these are firstly, the headlined company achievements of attaining US$23 billion in earnings for 2021 [with the Q4 share at just under US$9 billion] together with capital and exploration spending of US$17 billion in 2021 [with the Q4 share of this at around US$6 billion; alongside, a big push objective by ExxonMobil to reduce its indebtedness [through a share repurchase of US$10 billion]. These are required in order to assure anything resembling a return of shareholders’ confidence.

Secondly, the firm hopes the above will be further reinforced through significantly increased cash flows generated from its operating activities of about US$48 billion. This is indeed the highest level in the last ten years [2012]. Alongside this ExxonMobil has signaled it needs to zero in on reducing structural costs in the immediate term through spending of around US$2 billion. These measures are designed to improve the firm’s balance sheet to the pre-Covid 19 pandemic level; and will be supplemented with paying down US$20 billion in debt.

Thirdly, ExxonMobil has been, justifiably, quite brutally chastised in the social and mainstream media, as representing possibly the worst and ugliest of ‘big oil global robber barons” when that grouping of firms constituted the dominant players in the world’s oil and gas [energy] market, whether considered separately or taken collectively as the infamous big oil grouping of oil multinationals.

While nowhere as commanding today, the decades-long legacies of that big oil ignominy continues to haunt ExxonMobil going forward and, the detrimental roles ExxonMobil has played in global struggles to constrain the exponentially rising negative impacts of man-made global warming perhaps best illustrates this negativism. I’ll discuss these issues in coming columns where I propose to treat with ExxonMobil as a zombie plus corporation. Not surprisingly, I hope at that stage to deal with ExxonMobil’s Q4 2021 Report and its declared targets for carbon emissions, carbon capture, green energy, bio-fuels and renewables more broadly.

Finally, in the same ExxonMobil Q4 2021 Report referenced above, its Chairman and Chief Executive Officer has stressed the company’s strong focus on a new streamlined business structure aimed at maintaining shareholder value and preservation of the competitive advantages of the firm. In this regard, he claimed: “our effective pandemic response, focused investments during the down cycle and structured cost savings positioned us to realize the full benefits of the market recovery in 2021.”

Conclusion

I believe the above presentation supports the view that ExxonMobil may well be on the cusp of a possible turnaround. Next week I shall delve into the contentious issue as to whether Guyana’s emerging petroleum sector is a major contributor to this outcome.